The Ohio Utica Shale Play Turns 500… Almost!

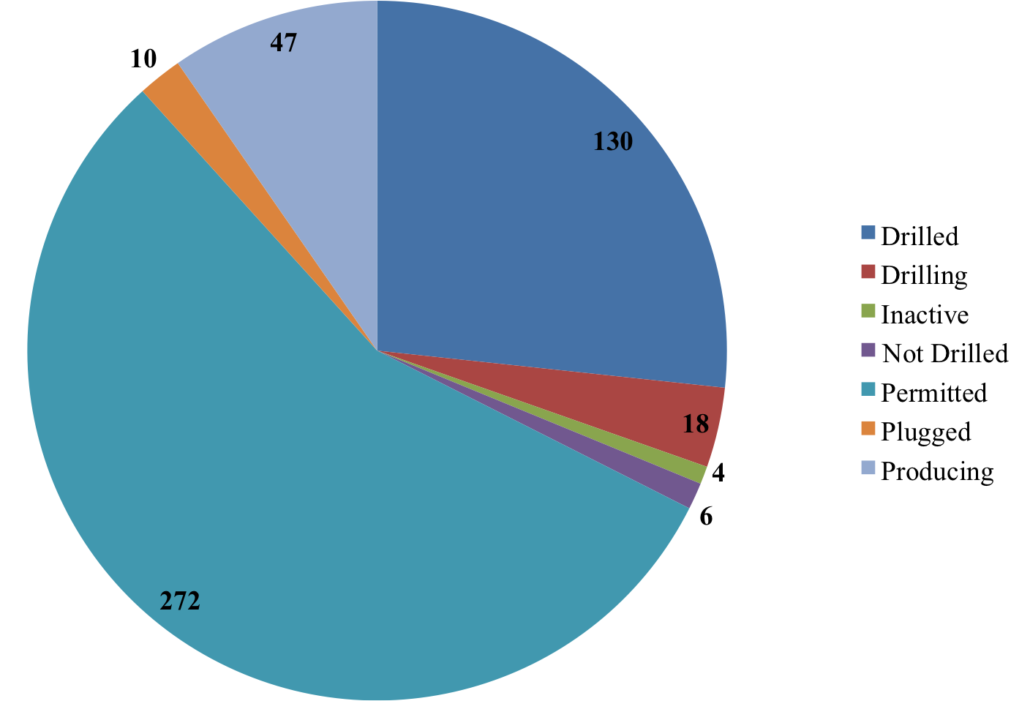

Drilling TrendsOhio’s first Utica well was permitted by ODNR on behalf of Hess Ohio Resources on 9-28-10. As shown in Figure 1 (right), the major uptick in well permitting began in the summer of 2011 with 23 wells permitted during that period, ramping up to 24 wells in November 2011. There was a brief reduction in permitting during the winter of 2011-12, followed by the boom-boom summer and fall of 2012, with an average of 37 wells per month and a total of 261 wells permitted between June and December 2012. ProductionAs of the end of 2012, only 30.4% of the 487 permitted wells had been drilled or are currently being drilled. Forty-seven are currently producing gas, with the Ohio Department of Natural Resources (ODNR) reporting production data for only 9 of the 47 producing wells. All of these wells are owned by Chesapeake, 2/3 of which are in Carroll County. On average, these wells produced 61 barrels of oil, 1,875 million cubic feet of gas, and 8,905 gallons (i.e. 37 tons) of brine per day over an average production period of 88 days. Twenty of the permitted wells are classified as inactive (not drilled) or plugged, with the remaining permitted but yet to be drilled (Figure 2). The top five Utica counties based on number of well permits are Carroll, Harrison, Columbiana [1], Jefferson, and Guernsey [2]; while on the other end, Ashland, Geauga, Medina, and Wayne are each home to one Utica well at this point (Figure 3). According to Columbus, OH-based Huntington Bank’s first Midwest Economic Index, early returns in these parts are mixed in Ohio: “58 percent of respondents agreed that the industry would bring opportunity, with 15 percent of those saying it would be a significant opportunity, while 42 percent said they did not see it bringing economic opportunity to their communities.” Bird’s Eye ViewFrom an area perspective, Carroll County has 0.45 wells per square mile – 0.39 more wells per square mile than the next ten counties with the most wells (Figure 4) – while the bottom four counties currently contain 0.0023 wells per square mile. The relationship between population and wells is generally the opposite of the previous two relationships with the bottom four counties having an average of 108,345 citizens for every well drilled. Carroll County has 163 residents per well, while the remaining top ten counties have an average resident-to-well ratio of 7,057 (Figure 4, Inset). This means that any potential ad valorem-based tax structure would benefit – on a per capita basis – less populated counties rather than those with more wells such as Carroll. Companies InvolvedChesapeake and its subsidiaries is the dominant player in the Ohio Utica play, with 320 of all wells permitted, followed by Gulfport Energy with 25, Enervest and HG Energy with 16, and Hess Ohio with 14 permitted wells. These five firms account for 80.3% of all permitted wells in Ohio, with an additional eighteen firms splitting the remaining 19.7% (Table 1, below). However, the firms that are publicly traded have been experiencing an average decline in share price of 3.41% since the time their first wells were permitted to the close of business on January 22nd, 2013. The biggest financial losers have been some of the Ohio Utica play’s biggest participants – including Chesapeake (CHK, -27%), Consol Energy (CNX, -29%), and Devon (DVN, -17%) [3]. Meanwhile, Anadarko (APC, +14%), Gulfport (GPOR, +19%)), and the upstart PDC Energy (PDCE, +55%) are the biggest beneficiaries of wading into Ohio’s Utica Shale play. However, the industry is displaying quite a few characteristics of an unsustainable boom; Wall Street analysts have been skeptical of big Utica Shale energy operations from soup to nuts as reported by Reuters last fall. but Wall Street voted in favor of the removal – either voluntary or forced – of CHK’s founder Aubrey McLendon to the tune of a 10% share spike the day of the announcement. Even the aforementioned winners have been outperformed by the S&P 500 and Dow Jones Industrial by 12.6% since permitting began in September 2010. Will the boom continue to boom? It may be too soon to tell, but one thing is for sure, shale gas extraction to-date has made an indelible mark on many communities in eastern Ohio. |

Figure 1. Ohio Utica Well Development per Month & Cumulatively as of January 1, 2013. Click on the image to view full-screen.  Figure 2. Ohio Utica Well Status as of January 1, 2013. Click on the image to view full-screen.  Figure 3. Ohio Utica Wells by County as of January 1, 2013. Click on the image to view full-screen.  Figure 4. Ohio Utica Wells Per Square Mile by County and People Per Well by County as of January 1, 2013. Click on the image to view full-screen. |

[1] Thanks to the surge in Columbiana County wells, the Texas-based Santrol will be opening a frac sand terminal with direct access to Ohio State Route 11 open 365 days a year and equipped to handle 500,000 tons annually.

[2] Guernsey and Noble are home to the Muskingum Watershed Conservancy District that is currently in negotiations with Antero to drill beneath Seneca Lake – even though there is a substantial and vocal opposition in the region in the form of the Southeast Ohio Alliance to Save Our Water.

Table 1. Distribution of Ohio Utica Shale wells across companies (#, %), Date of First Permit (DFP), and the valuation of the publicly funded companies at their DFP at the close of business 1/22/2013.

|

Company Valuation |

||||||

|

Company |

# |

% |

DFP† |

Share Price DFP |

Share Price 1/22/2013 |

% Change |

|

Anadarko |

12 |

0.025 |

09/07/2011 |

69.88 |

79.49 |

1.138 |

|

Antero |

11 |

0.023 |

03/23/2012 |

|||

|

Atlas Noble |

5 |

0.010 |

09/24/2012 |

31.14 |

30.315 |

0.974 |

|

Carrizo |

2 |

0.004 |

07/26/2012 |

24.02 |

22.43 |

0.934 |

|

Chesapeake Energy |

320 |

0.657 |

12/23/2010 |

25.61 |

18.73 |

0.731 |

|

Chevron Appalachia |

2 |

0.004 |

07/31/2012 |

109.58 |

115.91 |

1.058 |

|

Consol Energy |

19 |

0.039 |

06/17/2011 |

45.86 |

32.74 |

0.714 |

|

Devon Energy |

13 |

0.027 |

11/02/2011 |

65.46 |

54.28 |

0.829 |

|

Eclipse Resources |

1 |

0.002 |

12/21/2012 |

— |

— |

— |

|

Enervest |

16 |

0.033 |

06/30/2011 |

9.37 |

9.37 |

1.000 |

|

EQT |

1 |

0.002 |

09/13/2012 |

57.76 |

60.43 |

1.046 |

|

Gulfport Energy |

25 |

0.051 |

02/28/2012 |

35.49 |

42.3 |

1.192 |

|

Halcon |

1 |

0.002 |

11/02/2012 |

5.003 |

5.815 |

1.162 |

|

Hall Drilling |

1 |

0.002 |

09/17/2012 |

|||

|

Hess Ohio |

14 |

0.029 |

09/28/2010 |

53.63 |

58.87 |

1.098 |

|

HG Energy |

16 |

0.033 |

09/14/2011 |

— |

— |

— |

|

Hilcorp Energy |

1 |

0.002 |

12/14/2012 |

— |

— |

— |

|

Mountaineer Keystone |

7 |

0.014 |

07/13/2012 |

— |

— |

— |

|

PDC Energy |

4 |

0.008 |

05/25/2012 |

25.67 |

39.8 |

1.550 |

|

R E Gas Development |

8 |

0.016 |

03/19/2012 |

— |

— |

— |

|

Sierra Resources |

3 |

0.006 |

07/02/2012 |

— |

— |

— |

|

SWEPI |

1 |

0.002 |

06/20/2012 |

— |

— |

— |

|

XTO Energy |

4 |

0.008 |

04/09/2012 |

0.28 |

0.027 |

0.096 |

| Sum |

487 |

Average |

0.966 |

|||

† DFP = Date of First Permit; “—“ not a publicly funded company.