To Severance Tax or not to Severance Tax, that is the question!

By Ted Auch, PhD – OH Program Coordinator, FracTracker Alliance

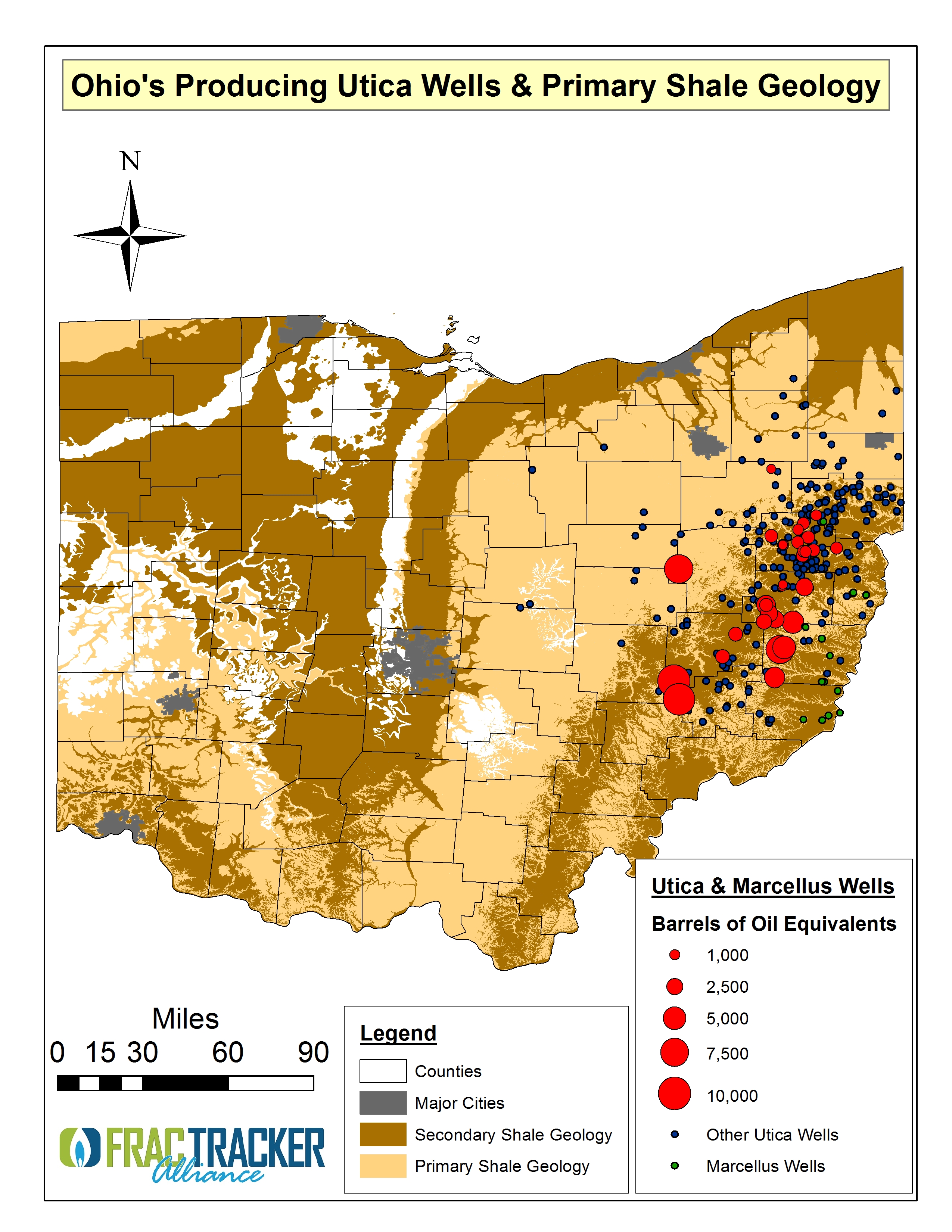

Figure 1. Ohio’s Producing Utica Wells & Primary Shale Geology – plus non-reporting, drilled, or producing Utica & Marcellus Wells.

“Million Cubic Feet” (MCF) as measured over industry standard test periods.

“Barrels of Oil Equivalents” (BOE) as measured over industry standard test periods.

The economic opportunities provided by Ohio’s Utica Shale play via hydraulic fracturing have been cited repeatedly by the Ohio Oil and Gas Association and industry think-tanks like IHS Inc [1]. Numbers published by the latter last October [2] predicted 143,000 Ohio jobs and $18 billion in state revenue by 2020. However, these projections are accompanied by substantial amounts of error. Given that the state’s Utica Shale well movement is now more than 500 wells permitted strong, we thought it was time to take a closer look at the demographics and economics of the Utica Play, given that there will be a strong geographic component being inserted into the “To Drill Or Not To Drill” and waste disposal debate here in Ohio. This is an especially important issue given that the state is wrestling with either implementing an ad valorem [3] tax or raising the state’s industry-low severance taxes, which currently stands at 0.5-0.8% but would be raised to 1% under the governor’s budget. In contrast, proposals from Policy Matters Ohio and northeast Ohio Democrats seek 5% – 7%, respectively.

In comparison to most other states producing oil and gas, even 5% may be a trivial amount, or what The Cleveland Plain Dealer called “indefensibly low.” It amounts to 97 cents per Ohioan (i.e., $275 mi2) [4]. According to an Ernst & Young analysis of eight states that produce dry gas and natural gas liquids and/or dry gas and oil…

- Ohio currently imposes the lowest combined state and local taxes of the states included in the analysis.

- …Ohio’s overall effective tax rate (measured as total taxes divided by sales) is 80% below the average rate for the other 7 states for a well producing dry natural gas and natural gas liquids.

- For a well producing dry natural gas and oil, Ohio’s effective tax rate is 65% below the other-state average…

- With the [proposed] increase, Ohio’s effective severance tax rate (ETR) would be 16% lower than the other states’ average for the well producing dry natural gas liquids and 4% lower than the other states’ average for the well producing dry natural gas and oil.

The governor’s proposed “Severance Tax Changes” will not apply to any Marcellus Shale wells, even though the state is home to five producing Marcellus wells (two in Monroe County) and eight permitted wells across Belmont and Monroe Counties. Additionally, the governor and his staff included a severance tax exemption for all “small-volume gas wells” (gas wells with average daily production of under 10 million cubic feet [MCF] would be exempt from the tax). If early industry production reports – and the Ohio Business Roundtable requested Ernst & Young report – are any indication, only 19% of wells will be subject to this tax. Our own analysis revealed that of the 32 industry reported production wells, the average production value is 7.5 MCF (Figure 1).The Kasich administration admitted the exemptions would apply to – by their estimation – 45,000 gas wells.

Another nuance of the Kasich administration’s severance tax complicated mélange is that rates will be 1% for natural gas and 4% for oil, natural gas liquids, and condensate. However, according to the administration:

… there will be a lower tax rate of 1.5 percent for the first year of production, in order to allow producers to recover the cost of preparing the well site and drilling the well.

Coincidentally, “the first year of production” is generally the time of greatest gas yields. Anonymous sources in Ohio’s Utica sweet spot have spoken of 50% declines in royalties within 6 months of production.

The Ohio Oil and Gas Association, the industry’s lobbying arm, has weighed-in against higher severance taxes, stating that:

a 4% severance tax on oil and gas would be equivalent to a 40% income tax and 16 times more than the commercial activities tax (or CAT). It would also burden economically challenged area throughout the state and landowners who want to lease their land and receive royalty streams.

Figure 2. Ohio’s Big Energy individual or Political Action Committee (PAC) political donations from 2001 to 2011. (Total: 4,037 individual donations. Data courtesy of Common Cause Ohio’s Deep Drilling, Deep Pockets spreadsheet.)

The anonymous BizzyBlog took the OOGA position one step further proclaiming that energy companies “won’t do business in a state with a newly-enacted punitive severance tax.”

Such arguments against a “hefty tax increase” don’t have much empirical support. OSU oil and gas development expert Douglas Southgate called such taxes “definitely affordable for the industry.” Even with the increases proposed by some, Ohio would still rank lowest among the eight shale gas producing states investigated by Ernst & Young in 2012.

Whereas an ad valorem tax would be redistributed directly back into the communities from which the hydrocarbons are extracted, a severance tax would be distributed throughout the state, even to communities and counties that prohibit Utica Shale drilling and/or injection activity. Theoretically, the entire state could benefit from the toils and environmental risks taken on by Ohio’s Appalachian region. According to a Quinnipiac pole, Ohioans support (52 to 38%) an increase in drilling-related severance taxes. Bipartisan voter support for a severance tax increases (60 to 32%) when the prospect of offsetting state income taxes is proposed.

Either levy – an ad valorem tax or severance tax – would be based upon the industry’s headline well production, even though USGS research recently spoke to the substantial well-to-well production variability in the Appalachian Shale Basin: 250-600% [5]. There are quite a few short- and long-term costs and benefits associated with exploitation of the Utica Shale; however, as it stands the risk burden is disproportionately being shouldered by Appalachian Ohio. Thus, the severance tax being proposed by the governor and House Democrats could add to the regional schisms evident in the state.

But maybe geography is immaterial. The likely big winner of the tax decisions will be energy companies and, according to data on recent campaign contributions, those politicians they deem worthy of their political donations – many of whom are on the fringes or completely outside the Utica Shale (Figure 2).

[1] IHS Global Insight is the brainchild of Daniel Yergin.

[2] This work was funded by the US Chamber of Commerce’s Institute for 21st Century Energy, the American Petroleum Institute, the American Chemistry Council, America’s natural Gas Alliance, and the Natural Gas Supply Association.

[3] Ad valorem taxes are assessed according to the value of the natural gas extracted.

[4] The Kasich “Ohio’s Jobs Budget 2.0: Jobs. Momentum. Transformation” highlights this aspect of their proposed severance tax, explicitly noting that it “has researched the severance tax structures of other states with significant oil and gas production, particularly those states with shale resources, and has found that even with a 4 percent tax rate, the tax burden on the revenues from these horizontal Utica wells will be lower than in other states.”

[5] According to the USGS, production from the most productive wells in the Appalachian Basin’s shale formations is commonly 50 times larger than the poorest producing wells, with the same value being 250-600 times larger for the Marcellus Basin. However, the only numbers presented to individual landowners – but less frequently to collectives given that energy firms are increasingly aware of the legal advice that land aggregators are seeking out – when the subject of royalties comes up are near-term gushers. For example:

- GPOR’s “’King’ of Utica Well” the Shugert 1-1H at 4,913 barrels of oil equivalents per day (BOEPD),

- CHK’s Buell well in Harrison County, OH producing 1,040 BOE[5],

- GPOR’s Boy Scout 1-33H in Wagner, Harrison County producing 3,456 BOE, the Ryser 1-25H producing 2,914, or the Groh 1-12H producing 1,935 BOE,

- Anadarko’s 9,5000 BOE, and

- The Wagner 1-H well producing 4,650 BOE. Yet, wells like the Frank unit in Stark County owned by Enervest producing 515 BOE or the non-producing wells across Ashland and Medina Counties are barely discussed – what a JP Morgan energy analyst called a “funding gap.”