North American Ethanol’s Land, Water, Nutrient, and Waste Impact

Corn Ethanol and Fracking – Similarities Abound

Even though it is a biofuel and not a fossil fuel, in this post we discuss the ways in which the corn ethanol production industry is similar to the fracking industry. For those who may not be familiar, biofuel refers to a category of fuels derived directly from living matter. These may include:

- Direct combustion of woody biomass and crop residues, which we recently mapped and outlined,

- Ethanol1 produced directly from the fermentation of sugarcanes or indirectly by way of the intermediate step of producing sugars from corn or switchgrass cellulose,

- Biodiesel from oil crops such as soybeans, oil palm, jatropha, and canola or cooking oil waste,2 and

- Anaerobic methane digestion of natural gas from manures or human waste.

Speaking about biofuels in 2006, J. Hill et al. said:

To be a viable substitute for a fossil fuel, an alternative fuel should not only have superior environmental benefits over the fossil fuel it displaces, be economically competitive with it, and be producible in sufficient quantities to make a meaningful impact on energy demands, but it should also provide a net energy gain over the energy sources used to produce it.

Out of all available biofuels it is ethanol that accounts for a lion’s share of North American biofuel production (See US Renewables Map Below). This trend is largely because most Americans put the E-10 blends in their tanks (10% ethanol).3 Additionally, the Energy Independence and Security Act of 2007 calls for ethanol production to reach 36 billion gallons by 2022, which would essentially double the current capacity (17.9 billion gallons) and require the equivalent of an additional 260 refineries to come online by then (Table 1, bottom).

US Facilities Generating Energy from Biomass and Waste along with Ethanol Refineries and Wind Farms

View map fullscreen | How FracTracker maps work

But more to the point… the language, tax regimes, and potential costs of both ethanol production and fracking are remarkably similar. (As evidenced by the quotes scattered throughout this piece.) Interestingly, some of the similarities are due to the fact that “Big Ag” and “Big Oil” are coupled, growing more so every year:

The shale revolution has resulted in declining natural gas and oil prices, which benefit farms with the greatest diesel, gasoline, and natural gas shares of total expenses, such as rice, cotton, and wheat farms. However, domestic fertilizer prices have not substantially fallen despite the large decrease in the U.S. natural gas price (natural gas accounts for about 75-85 percent of fertilizer production costs). This is due to the relatively high cost of shipping natural gas, which has resulted in regionalized natural gas markets, as compared with the more globalized fertilizer market. (USDA, 2016)

Ethanol’s Recent History

For background, below is a timeline of important events and publications related to ethanol regulation in the U.S. in the last four decades:

- Energy Research Advisory Board (ERAB) 1980, Gasohol

- ERAB, 1981, “Biomass Energy”

- Office of Energy, 1986, Fuel Ethanol and Agriculture: An Economic Assessment

- Clean Air Act 1990 Amendments (1990 CAAA) ethanol Reid Vapor Pressure (RVP) exceptions

- Congressional Research Service, 1994, Alcohol Fuels Tax Incentives and EPA’s Renewable Oxygenate Requirement

- The Biomass Research and Development Act of 2000 (Title III of the Agricultural Risk Protection Act)

- US Department of Energy (DOE), 2002, “Roadmap for biomass technologies in the United States. Biomass Technical Advisory Committee”, Found here and here

- USDA, 2002, Ethanol Cost-of-Production Survey

- US Natural Resources Conservation Service (NRCS), 2003, Crop residue removal for biomass energy production: Effects on soils and recommendations

- US Department of Energy, 2003, Biomass program multi-year technical plan

- The Renewable Fuel Standard (RFS) program is implemented as part of the Energy Policy Act of 2005 and extended in the Energy Independence and Security Act of 2007

- US DOE, 2005, Energy Efficiency and Renewable Energy

- US Energy Independence and Security Act, 2007

- USDA, 2007, U.S. Ethanol Expansion Driving Changes Throughout the Agricultural Sector

- USDA, 2007, Growing global demands for soy for edible oil, livestock feed, and biodiesel are also contributing to high soy prices (no file found on USDA site anymore)

- Special Report of the Intergovernmental Panel on Climate Change (IPCC), 2011, Renewable Energy Sources and Climate Change Mitigation

- 2014 Farm Bill authorized the “Biomass Crop Assistance Porgram” (aka, The 2014 Agricultural Act)

Benefits of Biofuels

[Bill] Clinton justified the ethanol mandate by declaring that it would provide “thousands of new jobs for the future” and that “this policy is good for our environment, our public health, and our nation’s farmers—and that’s good for America.” EPA administrator Carol Browner claimed that “it is important to our efforts to diversify energy resources and promote energy independence.” – James Bovard citing Peter Stone’s “The Big Harvest,” National Journal, July 30, 1994.

Of the 270 ethanol refineries we had sufficient data for, we estimate these facilities employ 235,624 people or 873 per facility and payout roughly $6.18-6.80 billion in wages each year, at an average of $22.9-25.2 million per refinery. These employees spend roughly 423,000 hours at the plant or at associated operations earning between $14.63 and $16.10 per hour including benefits. Those figures amount to 74-83% of the average US income. In all fairness, these wages are 13-26% times higher than the farming, fishing, and forestry sectors in states like Minnesota, Nebraska, and Iowa, which alone account for 33% of US ethanol refining.

Additional benefits of ethanol refineries include the nearly 179 million tons of CO2 left in the field as stover each year, which amounts to 654,532 tons per refinery. Put another way – these amounts are equivalent to the annual emissions of 10.7 million and 39,194 Americans, respectively.

Finally, what would a discussion of ethanol refineries be without an estimate of how much gasoline is produced? It turns out that the 280 refineries (for which we have accurate estimates of capacity) produce an average of 71.93 million gallons per year and 20.1 billion gallons in total. That figure represents 14.3% of US gasoline demand.

Costs of Biofuels

Direct Costs

Biofuel expansions such as those listed in the timeline above and those eluded to by the likes of the IPCC have several issues associated with them. One of which is what Pimentel et al. considered an insufficient – and to those of us in the fracking NGO community, familiar sounding – “breadth of relevant expertise and perspectives… to pronounce fairly and roundely on this many-sided issue.”

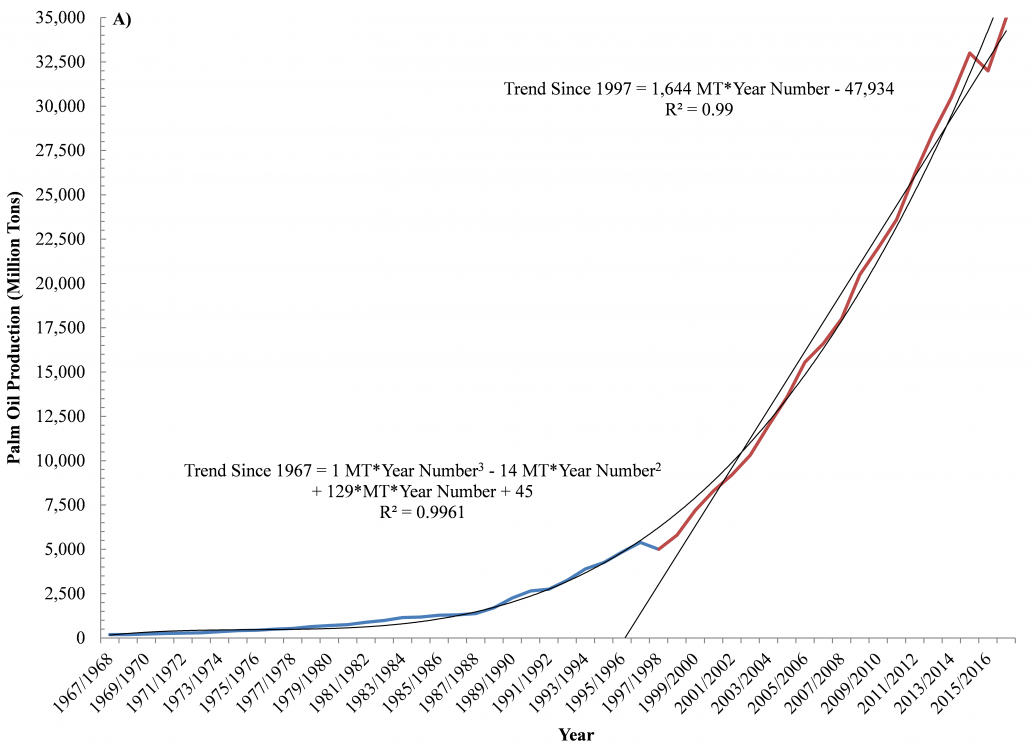

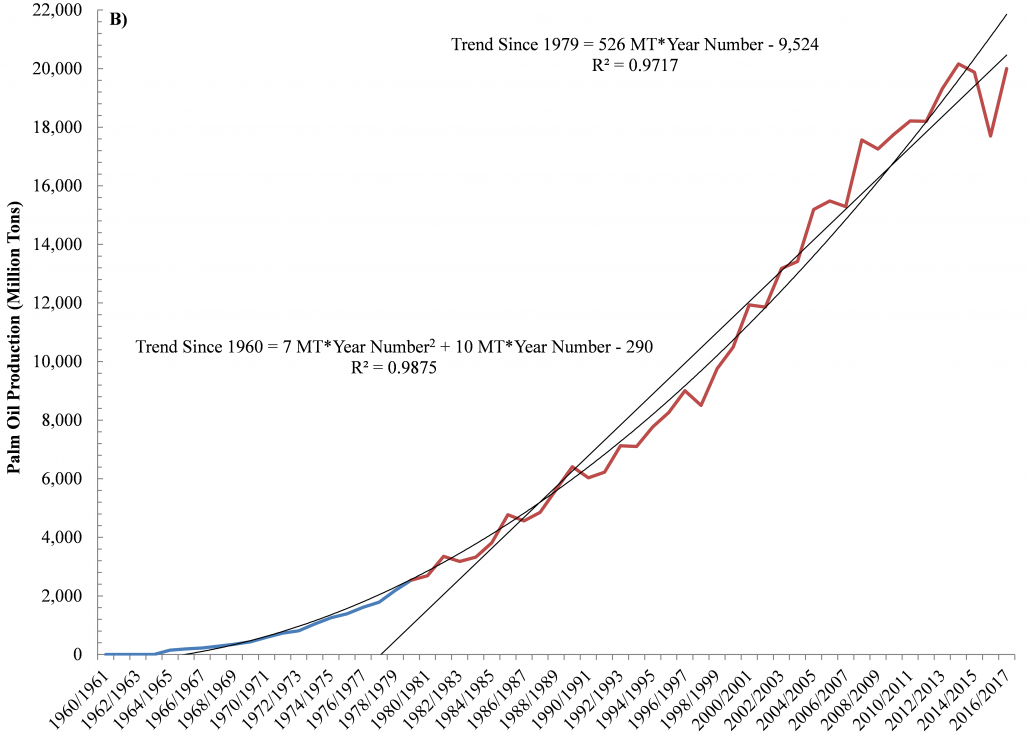

The above acts and reports in the timeline prompted many American farmers to double down on corn at the expense of soybeans, which caused Indirect Land Use Change (ILUC); the global soy market skyrocketed. This, in turn, prompted the clearing and/or burning of large swaths of the Amazonian rainforests and tropical savannas in Brazil, the world’s second-leading soy producer. More recently, large swaths of Indonesia and Malaysia’s equally biodiverse peatland forests have been replaced by palm oil plantations (Table 2 and Figure 3, bottom). In the latter countries, forest displacement is increasing by 2.7-5.3% per year, which is roughly equal to the the rate of land-use change associated with hydraulic fracturing here in the US4 (Figure 1).

Figures 1A and 1B. Palm Oil Production in A) Indonesia and B) Malaysia between 1960 and 2016.

There is an increasing amount of connectivity between disparate regions of the world with respect to energy consumption, extraction, and generation. These connections also affect how we define renewable or sustainable:

In a globalized world, the impacts of local decisions about crop preferences can have far reaching implications. As illustrated by an apparent “corn connection” to Amazonian deforestation, the environmental benefits of corn-based biofuel might be considerably reduced when its full and indirect costs are considered. (Science, 2007)

These authors pointed to the fact that biofuel expectations and/or mandates fail to account for costs associated with atmospheric – and leaching – emissions of carbon, nitrogen, phophorus, etc. during the conversion of lands, including diverse rainforests, peatlands, savannas, and grasslands, to monocultures. Also overlooked were:

- The ethical concerns associated with growing malnourishment from India to the United States,

- The fact that 10-60%5 more fossil fuel derived energy is required to produce a unit of corn ethanol than is actually contained within this very biofuel, and

- The tremendous “Global land and water grabbing” occuring in the name of natural resource security, commodification, and biofuel generation.

Sacrificing long-term ecological/food security in the name of short-term energy security has caused individuals and governments to focus on taking land out of food production and putting it into biofuels.

The rationale for ethanol subsidies has continually changed to meet shifting political winds. In the late 1970s ethanol was championed as a way to achieve energy independence. In the early 1980s ethanol was portrayed as salvation for struggling corn farmers. From the mid and late 1980s onward, ethanol has been justified as saving the environment. However, none of those claims can withstand serious examination. (James Bovard, 1995)

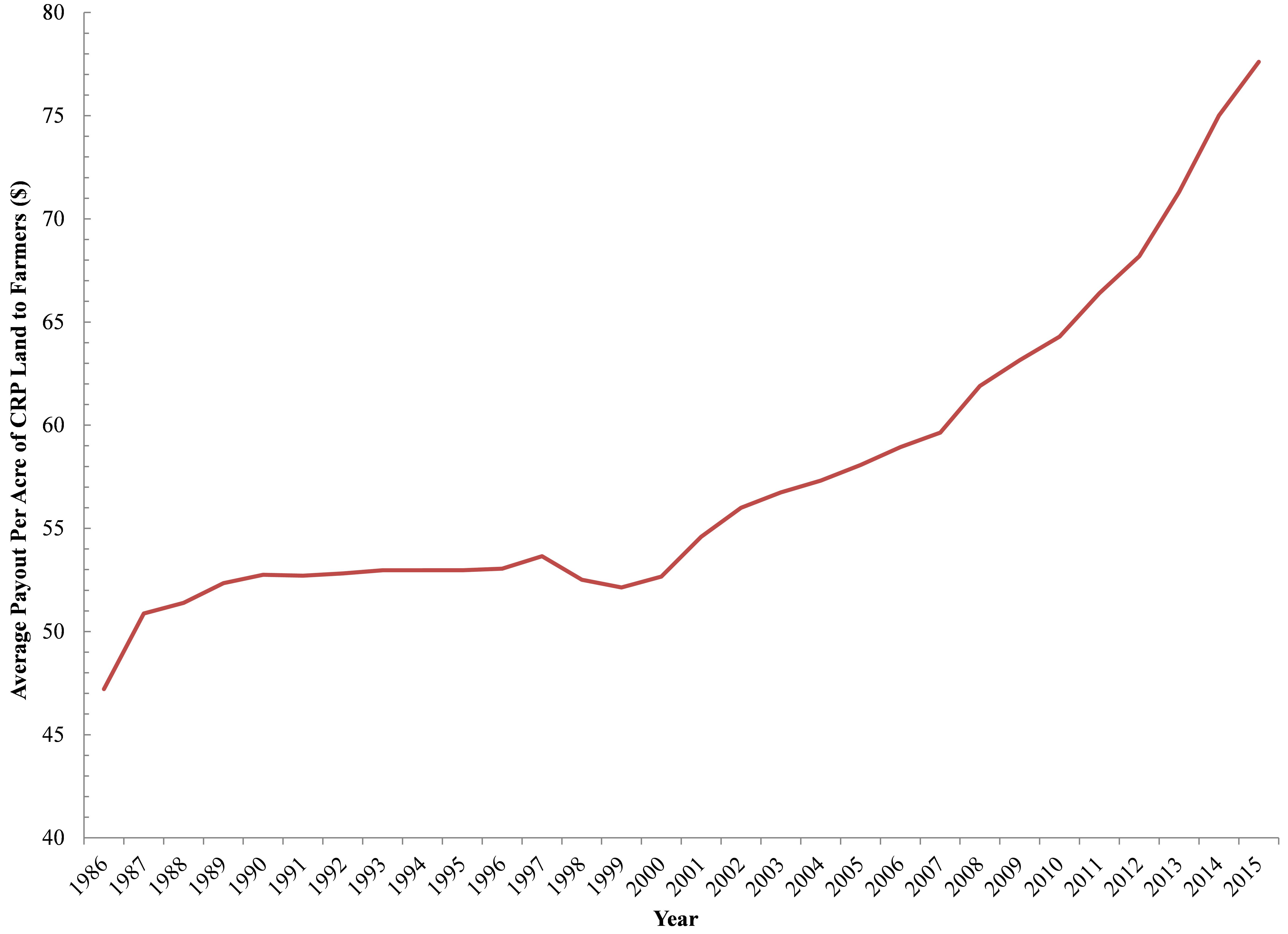

This is instead of going the more environmentally friendly route of growing biofuel feedstocks on degraded or abandoned lands. An example of such an endeavor is the voluntary US Conservation Reserve Program (CRP), which has stabilized at roughly 45-57 thousand square miles of enrolled land since 1990, even though the average payout per acre has continued to climb (Figure 2).

Figure 2. The Average Subsidy to Farmers Per Acre of Conservation Reserve Program (CRP) between 1986 and 2015.

The primary goals of the CRP program are to provide an acceptable “floor” for commodity prices, reduce soil erosion, enhance wildlife habitat, ecosystem services, biodiversity, and improve water quality on highly erodible, degraded, or flood proned croplands. Interestingly CRP acreage has declined by 27% since a high of 56 thousand square miles prior to the Energy Independence and Security Act of 2007 being passed. Researchers have pointed to the fact that corn ethanol production on CRP lands would create a carbon debt that would take 48 years to repay vs. a 93 year payback period for ethanol on Central US Grasslands.

To quote Fred Magdoff in The Political Economy and Ecology of Biofuels:

Alternative fuel sources are attractive because they can be developed and used without questioning the very workings of the economic system — just substitute a more “sustainable,” “ecologically sound,” and “renewable” energy for the more polluting, expensive, and finite amounts of oil. People are hoping for magic bullets to “solve” the problem so that capitalist societies can continue along their wasteful growth and consumption patterns with the least disruption. Although prices of fuels may come down somewhat — with dips in the business cycle, higher rates of production, or a burst in the speculative bubble in the futures market for oil — they will most likely remain at historically high levels as the reserves of easily recovered fuel relative to annual usage continues to decline.

Indirect Costs: Ethanol, Fertilizers, and the Gulf of Mexico Dead Zone

This is the Midwest vs. the Middle East. It’s corn farmers vs. the oil companies. – Dwaney Andreas in Big Stink on the Farm by David Greising

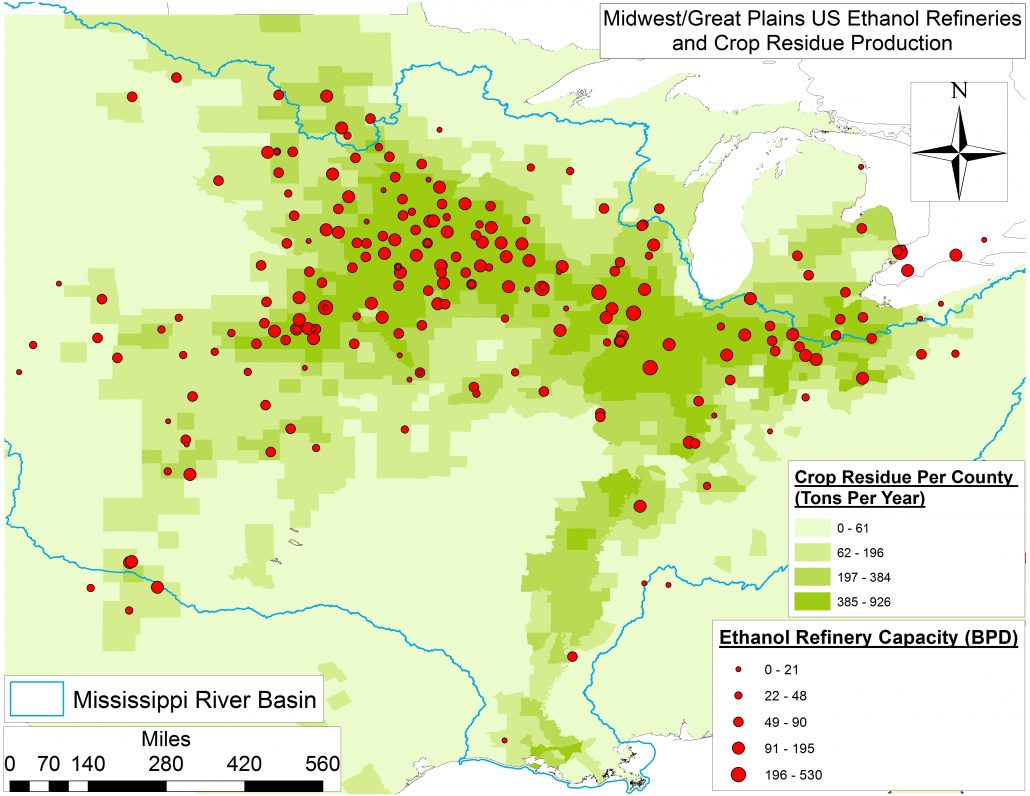

Sixty-nine percent6 of North America’s ethanol refineries are within the Mississippi River Basin (MRB). These refineries collectively rely on corn that receives 1.9-5.1 million tons of nitrogen each year, with a current value of $1.06-2.91 billion dollars or 9,570-26,161 tons of nitrogen per refinery per year (i.e. $5.42-14.81 million per refinery per year). These figures account for 27-73% of all nitrogen fertilizer used in the MRB each year. More importantly, the corn acreage receiving this nitrogen leaches roughly 0.81-657 thousand tons of it directly into the MRB. Such a process amounts to 5-44% of all nitrogen discharged into the Gulf of Mexico each year and 1.7-13.8 million tons of algae responsible for the Gulf’s growing Dead Zone.

Leaching of this nitrogen is analogous to flushing $45.7-371.6 million dollars worth of precious capital down the drain. Put another way, these dollar figures translate into anywhere between 55% and an astonishing 4.53 times Direct Costs to the Gulf’s seafood and tourism industries of the Dead Zone itself.

These same refineries rely on corn acreage that also receives 0.53-2.61 million tons of phosphorus each year with a current value of 0.34-1.66 billion dollars. Each refinery has a phosphrous footprint in the range of 2,700 to 13,334 tons per year (i.e., $1.72-8.47 million). We estimate that 25,399-185,201 tons of this fertilizer phosphorus is leached into the the MRB, which is equivalent to 19% or as much as 1.42 times all the phosphorous dischared into the Gulf of Mexico per year. Such a process means $16.13-117.60 million is lost per year.

Together, the nitrogen and phosphorus leached from acreage allocated to corn ethanol have a current value that is between 75% and nearly 6 times the value lost every year to the Gulf’s seafood and tourism industries.

Indirect Costs: Fertilizer and Herbicide Costs and Leaching

The 270 ethanol refineries we have quality production data for are relying on corn that receives 367,772 tons of herbicide and insecticide each year, with a current value of $6.67 billion dollars or 1,362 tons of chemical preventitive per refinery per year (i.e. $24.7 million per refinery per year). More importantly the corn acreage receiving these inputs leaches roughly 15.8-128.7 thousand tons of it directly into surrounding watersheds and underlying aquifers. Leaching of these inputs is analogous to flushing $287 million to $2.3 billion dollars down the drain.

What’s Next?

During the recent Trump administration EPA, USDA, DOE administrator hearings, the Renewable Fuel Standard (RFS) was cited as critical to American energy independence by a bipartisan group of 23 senators. Among these were Democratic senator Amy Klobuchar and Republican Chuck Grassley, who co-wrote a letter to new EPA administrator Scott Pruitt demanding that the RFS remains robust and expands when possible. In the words of Democratic Senator Heidi Heitkamp – and long-time ethanol supporter – straight from the heart of the Bakken Shale Revolution in North Dakota:

The RFS has worked well for North Dakota farmers, and I’m fighting to defend it. As we’re doing today in this letter, I’ll keep pushing in the U.S. Senate for the robust RFS [and Renewable Volume Obligations (RVOs)] we need to support a thriving biofuels industry and stand up for biofuels workers. Biofuels create good-paying jobs in North Dakota and help support our state’s farmers, who rely on this important market – particularly when commodity prices are challenging.

Furthermore, the entire Iowa congressional delegation including the aforementioned Sen. Grassley joined newly minted USDA Secretary Sonny Perdue when he told the Iowa Renewable Fuels Association:

You have nothing to worry about. Did you hear what he said during the campaign? Renewable energy, ethanol, is here to stay, and we’re going to work for new technologies to be more efficient.

How this advocacy will play out and how the ethanol industry will respond (i.e., increase productivity per refinery or expand the number of refineries) is anybody’s guess. However, it sounds like the same language, lobbying, and advertising will continue to be used by the Ethanol and Unconventional Oil and Gas industries. Additional parallels are sure to follow with specific respect to water, waste, and land-use.

Furthermore, as both industries continue their ramp up in research and development, we can expect to see productivity per laborer to continue on an exponential path. The response in DC – and statehouses across the upper Midwest and Great Plains – will likely be further deregulation, as well.

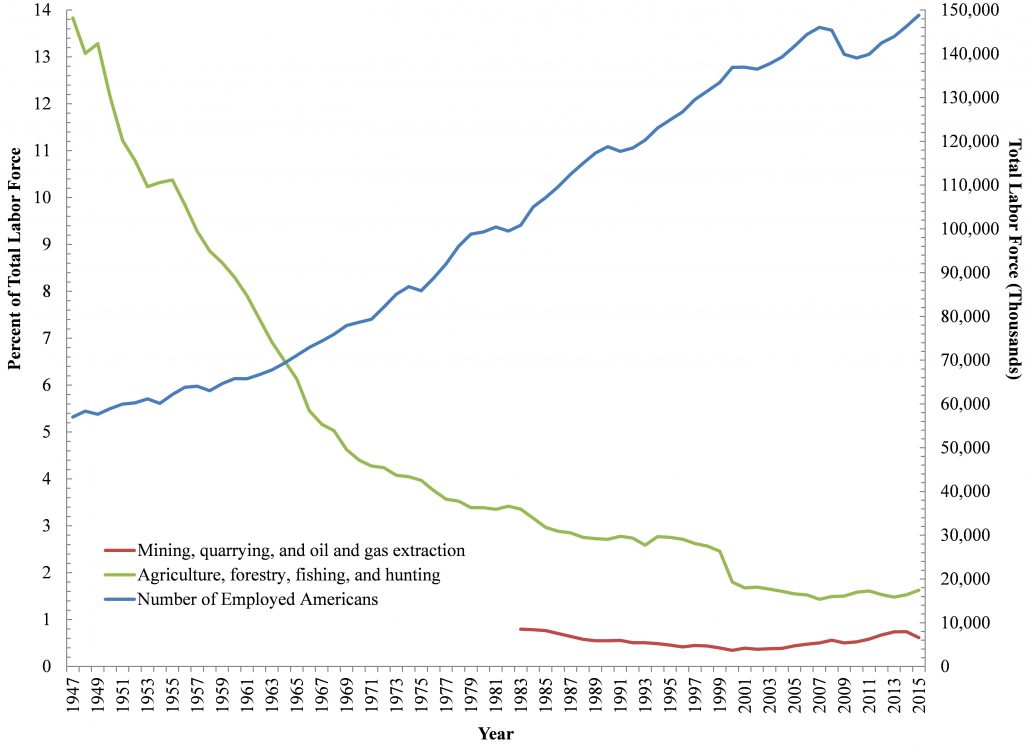

From a societal perspective, an increase in ethanol production/grain diversion away from people’s plates has lead to a chicken-and-egg positive feedback loop, whereby our farmers continue to increase total and per-acre corn production with less and less people. In rural areas, mining and agriculture have been the primary employment sectors. A further mechanization of both will likely amplify issues related to education, drug dependence, and flight to urban centers (Figures 4A and B).

We still don’t know exactly how efficient ethanol refineries are relative to Greenhouse Gas Emissions per barrel of oil. By merging the above data with facility-level CO2 emissions from the EPA Facility Level Information on Greenhouse gases Tool (FLIGHT) database we were able to match nearly 200 of the US ethanol refineries with their respective GHG emissions levels back to 2010. These facilities emit roughly:

- 195,116 tons of CO2 per year, per facility,

- A total of 36.97 million tons per year (i.e., 2.11 million Americans worth of emissions), and

- 22,265 tons of CO2 per barrel of ethanol produced.

Emissions from ethanol will increase to 74.35 million tons in 2022 if the Energy Independence and Security Act of 2007’s prescriptions run their course. Such an upward trend would be equivalent to the GHG emissions of somewhere between that of Seattle and Detroit.

What was once a singles match between Frackers and Sheikhs may turn into an Australian Doubles match with the Ethanol Lobby and Farm Bureau joining the fray. This ‘game’ will only further stress the food, energy, and water (FEW) nexus from California to the Great Lakes and northern Appalachia.

We are on a thinner margin of food security, just as we are on a thinner margin of oil security… The [World] Bank implicitly questions whether it is wise to divert half of the world’s increased output of maize and wheat over the next decade into biofuels to meet government “mandates.” – Ambrose Evans-Pritchard in The Telegraph

Will long-term agricultural security be sacrificed in the name of short-term energy independence?

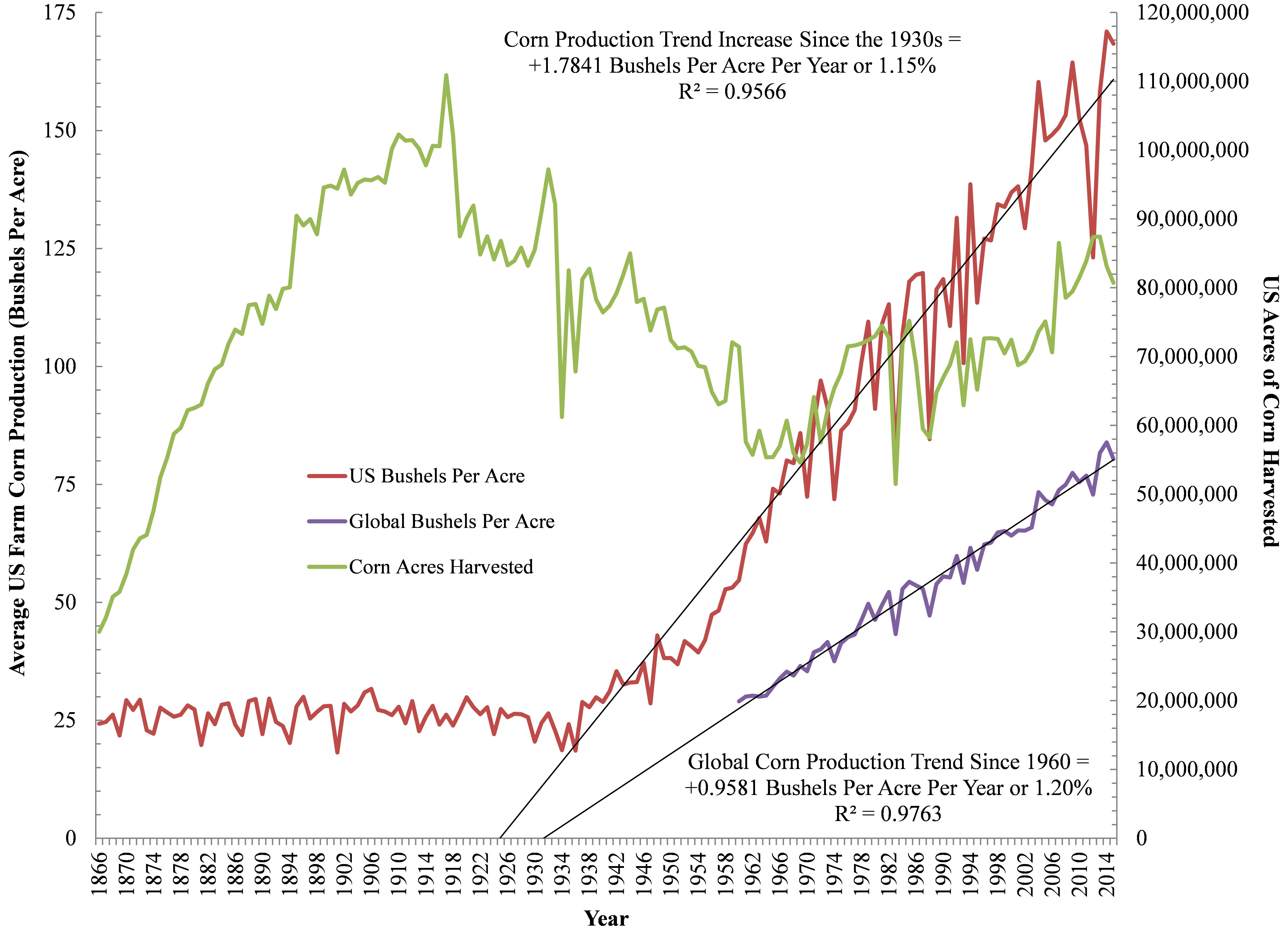

Figure 3. US and Global Corn Production and Acreage between 1866 and 2015.

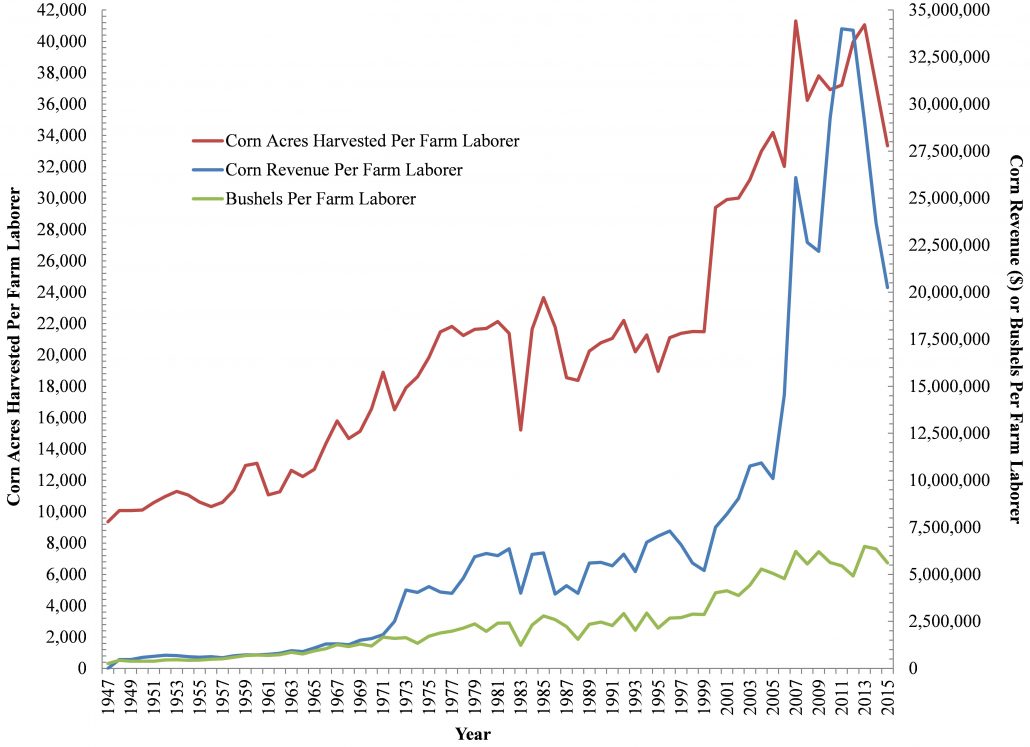

Figures 4A and 4B. A) Number of Laborers in the US Mining, Oil and Gas, Agriculture, Forestry, Fishing, and Hunting sector and B) US Corn Production Metrics Per Farm Laborer between 1947 and 2015.

Ethanol Tables

Table 1. Summary of our Corn Ethanol Production, Land-Use, and Water Demand analysis

| Gallons of Corn Ethanol Produced Per Year | 17,847,616,000 |

| Bushels of Corn Needed | 6,374,148,571 |

| Percent of US Production | 44.73% |

| Land Needed | 104,372,023 acres |

| “” | 163,081 square miles |

| Percent of Contiguous US Land | 5.51% |

| Percent of US Agricultural Land | 11.28% |

| Gallons of Water Needed | 49.76 trillion (i.e. 3.55 million swimming pools) |

| Gallons of Water Per Gallon of Oil | 2,788 |

| Average and Total Site/Industry Capacity | |

| Average Corn Ethanol Production Per Existing or Under Construction Facility (n = 257) | 69,717,250 |

| Gallons of Corn Ethanol Produced Per Year | 17,847,616,000 |

| Difference Between 2022 Energy Independence and Security Act of 2007 36 Billion Gallon Mandate | 18,152,384,000 |

| # of New Refineries Necessary to Get to 2022 Levels | 260 |

| Percent Increase Over Current Facility Inventory | 1.7 |

| IEA 2009 World Energy Outlook 250-620% Increase Predictions for 2030 | |

| 250% | 44,619,040,000 |

| # of New Refineries Necessary | 640 |

| Percent Increase Over Current Facility Inventory | 150.00 |

| 620% | 110,655,219,200 |

| # of New Refineries Necessary | 1,587 |

| Percent Increase Over Current Facility Inventory | 520.00 |

Table 2. Global Population Growth and Corn and Soybean Productivity Trends.

| Percent Change | Metric |

| +1.13% | Global Population Growth Trend |

| Corn (Bushels Per Acre) | |

| +1.15% Per Year | United States |

| +1.20% Per Year | Global |

| Soybean (Tons Per Acre) | |

| +0.9% Per Year | United States |

| +1.5% Per Year | Brazil |

| Palm Oil (Tons) | |

| +5.1% Per Year | Indonesia |

| +2.7% Per Year | Malaysia |

References and Footnotes

- Ethanol as defined in the Ohio Revised Code (ORC) Corporation Franchise Tax 5733.46 means “fermentation ethyl alcohol derived from agricultural products, including potatoes, cereal, grains, cheese whey, and sugar beets; forest products; or other renewable resources, including residue and waste generated from the production, processing, and marketing of agricultural products, forest products, and other renewable resources that meet all of the specifications in the American society for testing and materials (ASTM) specification D 4806-88 and is denatured as specified in Parts 20 and 21 of Title 27 of the Code of Federal Regulations.”

- A) Pyrolysis is included in the biofuel category and involves the anaerobic decay of cellulose rich feedstocks such as switchgrass at high temperatures producing synthetic diesel or syngas, and

B) According to many researchers biofuels made from waste biomass or crops grown on degraded and abandoned lands with warm-season prairie grasses and legumes incur little or no carbon debt and provide “immediate and sustained Greenhouse Gas (GHG) advantages” by rehabilitating soil health and capturing, rather than emitting by way of increased fertilizer use, various forms of nitrogen including N2O, NO3–, and NO2–. - According to Fred Magdoff, the ethanol complex is lobbying for “more automobile engines capable of using E-85 (85 percent ethanol, 15 percent gasoline) for which there are currently 2,710 fueling stations across the country although 56% of them are in just nine states: 1) Wisconsin (117), 2) Missouri (107), 3) Minnesota (335), 4) Michigan (174), 5) Indiana (172), 6) Illinois (221), 7) Iowa (193), 8) Texas (99), and 9) Ohio (97). Some states are mandating a mixture greater than 10 percent. Ethanol can’t be shipped together with gasoline in pipelines because it separates from the mixture when moisture is present, so it must be trucked to where it will be mixed with gasoline.” The E-85 blend comes with its own costs including higher emissions of CO, VOC, PM10, SOx, and NOx than gasoline.

- McClaugherty, C., Auch, W. Genshock, E. and H. Buzulencia. (2017). Landscape impacts of infrastructure associated with Utica shale oil and gas extraction in eastern Ohio, Ecological Society of America, 100th Annual Meeting, Baltimore, MD, August, 2015.

- Hill et al. recently indicated “Ethanol yields 25% more energy than the energy invested in its production, whereas biodiesel yields 93% more.”

- An additional 9-10 refineries or 73% of all ethanol refineries are within 25 miles of the Mississippi River Basin.

By Ted Auch, PhD, Great Lakes Program Coordinator, FracTracker Alliance

Cover photo, left: Oil and gas well pad, Ohio. Photo by Ted Auch.

Cover photo, right: A typical ethanol plant in West Burlington, Iowa. Photo by Steven Vaughn.

Data Downloads

Click on the links below to download the datasets used to create the maps in this article.