Tracking Global Oil Refineries and their Emissions

Potential Conflict Hotspots and Global Productivity Choke Points

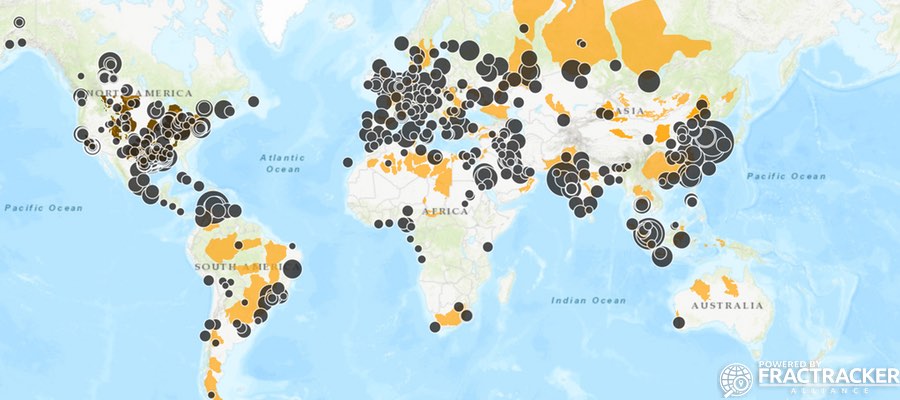

Today, FracTracker is releasing a complete inventory of all 536 global oil refineries, along with estimates of daily capacity, CO2 emissions per year, and various products. These data have also been visualized in the map below.

Total productivity from these refineries amounts to 79,372,612 barrels per day (BPD) of oil worldwide, according to the data we were able to compile. However, based on the International Energy Agency, global production is currently around 96 million BPD, which means that our capacity estimates are more indicative of conditions between 2002 and 2003 according to BP’s World Oil Production estimates. We estimate this disparity is a result of countries’ reluctance to share individual refinery values or rates of change due to national security concerns or related strategic reasons.

These refineries are emitting roughly 260-283 billion metric tons (BMT) of CO2[1], 1.2-1.3 BMT of methane and 46-51 million metric tons of nitrous oxide (N2O) into the atmosphere each year. The latter two compounds have climate change potentials equivalent to 28.2-30.7 BMT and 14.1-15.3 BMT CO2, respectively.

Assuming the planet’s 7.6 billion people emit 4.9-5.0 metric tons per capita of CO2 per year, emissions from these 536 refineries amounts to the CO2 emissions of 52-57 million people. If you include the facilities’ methane and N2O emissions, this figure rises to 61-66 million people equivalents every year, essentially the populations of the United Kingdom or France.

Map of global oil refineries

View map fullscreen | How FracTracker maps work | View static map | Download map data

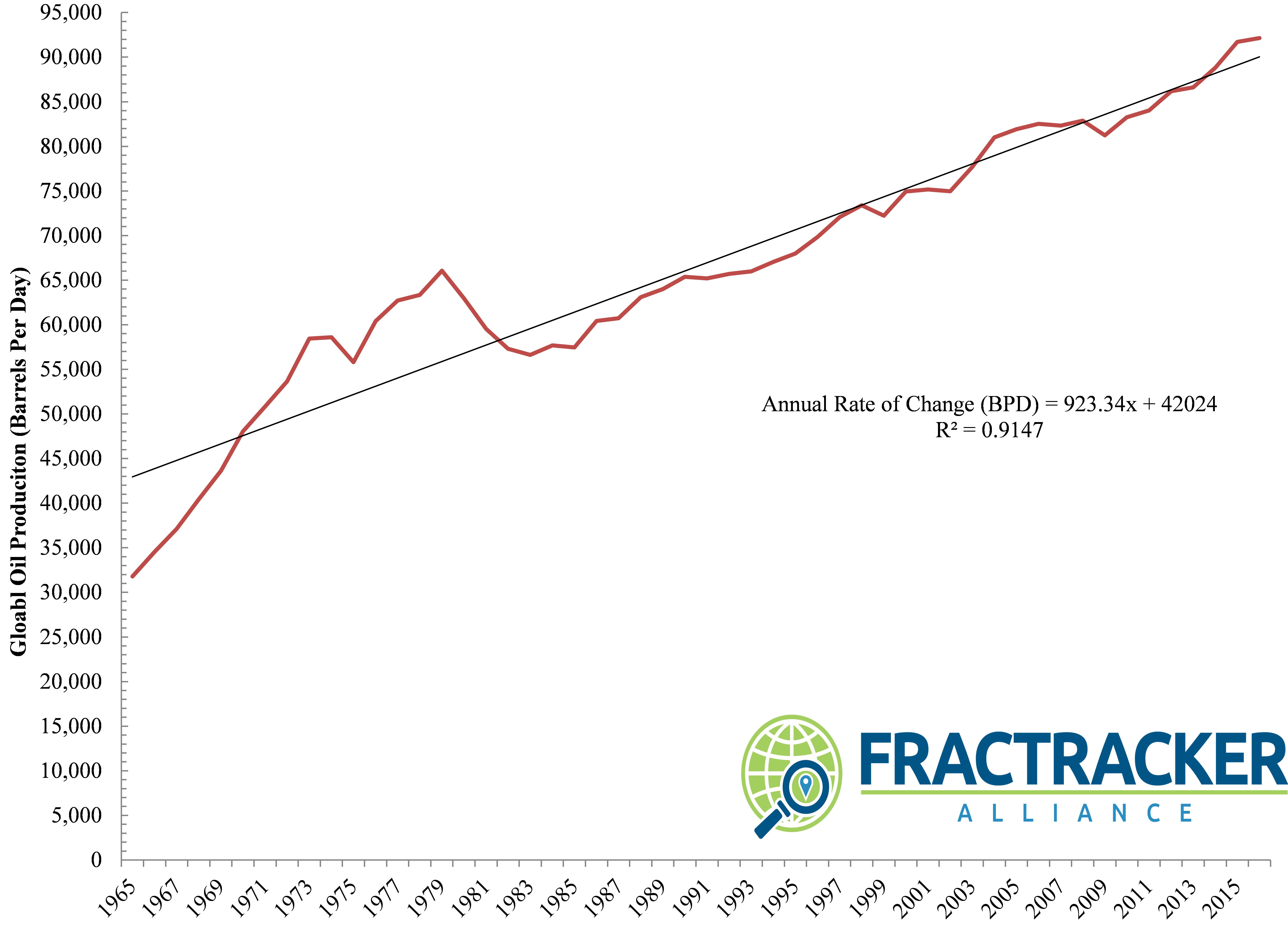

BP’s data indicate that the amount of oil being refined globally is increasing by 923,000 BPD per year (See Figure 1). This increase is primarily due to improved productivity from existing refineries. For example, BP’s own Whiting, IN refinery noted a “$4-billion revamp… to boost its intake of Canadian crude oil from 85,000 bpd to 350,000 bpd.”

Figure 1. Global Oil Production, 1965 to 2016 (barrels per day) – Data courtesy of British Petroleum (BP) World Oil Production estimates.

Potential Hotspots and Chokepoints

Across the globe, countries and companies are beginning to make bold predictions about their ability to refine oil.

Nigeria, for example, recently claimed they would be increasing oil refining capacity by 13% from 2.4 to 2.7 million BPD. Currently, however, our data indicate Nigeria is only producing a fraction of this headline number (i.e., 445,000 BPD). The country’s estimates seem to be more indicative of conditions in Nigeria in the late 1960s when oil was first discovered in the Niger Delta. Learn more.

Is investing in – and doubling down on – oil refining capacity a smart idea for Nigeria’s people and economy, however? At this point, the country’s population is 3.5 times greater than it was in the 60’s and is growing at a remarkable rate of 2.7% per year. Yet, Nigeria’s status as one of the preeminent “Petro States” has done very little for the majority of its population – The oil industry and the Niger Delta have become synonymous with increased infant mortality and rampant oil spills.

Sadly, the probability that the situation will improve in a warming – and more politically volatile – world is not very likely.

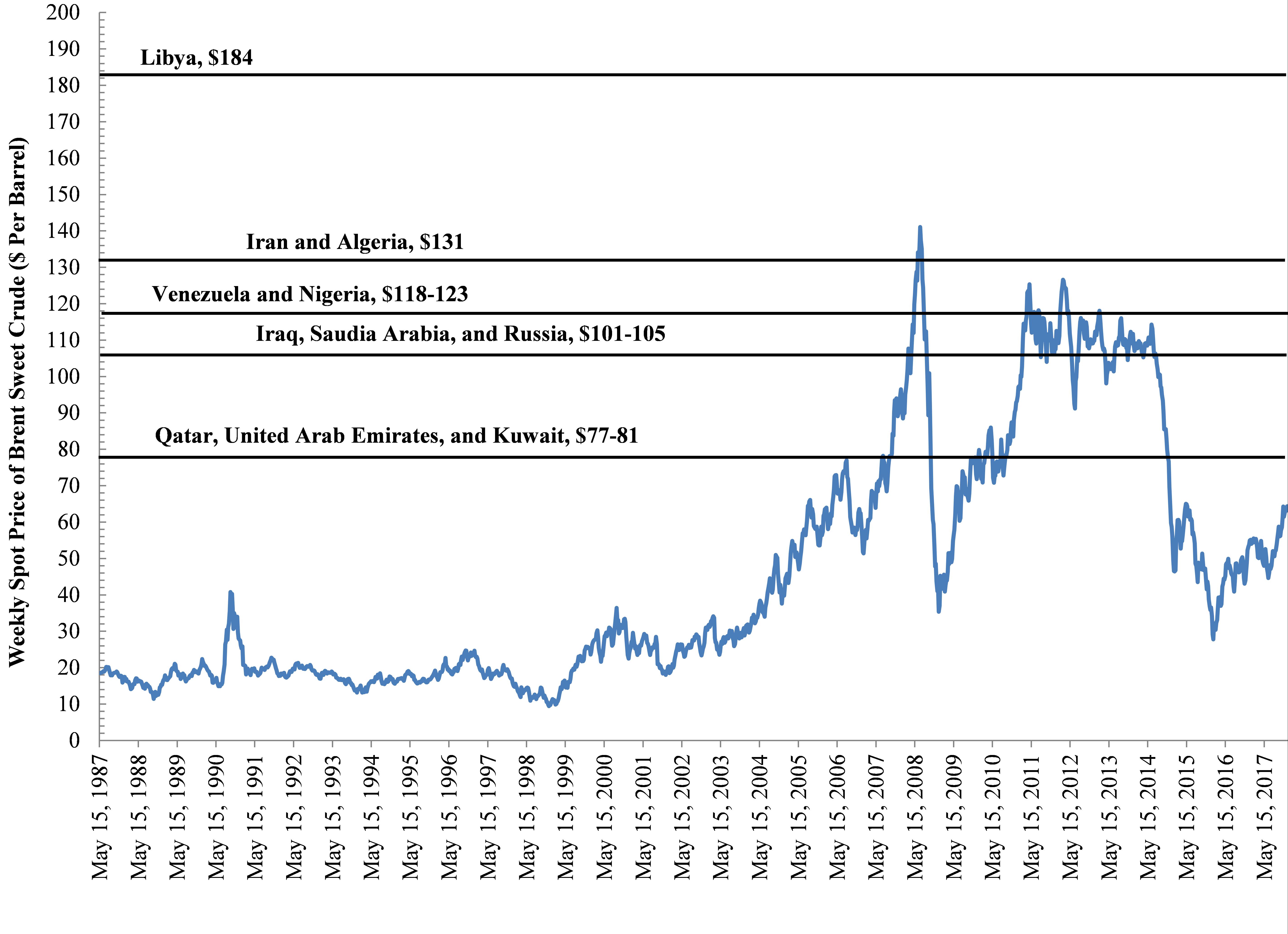

Such a dependency on oil price has been coupled to political instability in Nigeria, prompting some to question whether the discovery of oil was a cure or a curse given that the country depends on oil prices – and associated volatility – to balance its budget: Of all the Organization of Petroleum Exporting Countries (OPEC) countries, Nigeria is near the top of the list when it comes to the price of oil the country needs to balance its budget – Deutsche Bank and IMF estimate $123 per barrel as their breaking point. This is a valuation that oil has only exceeded or approached 4.4% of the time since 1987 (See Figure 2).

Former Central Bank of Nigeria Governor, Charles Soludo, once put this reliance in context:

… For too long, we have lived with borrowed robes, and I think for the next generation, for the 400 million Nigerians expected in this country by the year 2050, oil cannot be the way forward for the future.

Other regions are also at risk from the oil market’s power and volatility. In Libya, for example, the Ras Lanuf oil refinery (with a capacity of 220,000 BPD) and the country’s primary oil export terminal in Brega were the focal point of the Libyan civil war in 2011. Not coincidentally, Libya also happens to be the Petro State that needs the highest per-barrel price for oil to balance its budget (See Figure 2). Muammar Gaddafi and the opposition, National Transitional Council, jostled for control of this pivotal choke point in the Africa-to-Europe hydrocarbon supply chain.

The fact that refineries like these – and others in similarly volatile regions of the Middle East – produce an impressive 10% (7,166,900 BPD) of global demand speaks to the fragility of these Hydrocarbon Industrial Complex focal points, as well as the planet’s fragile dependence on fossil fuels going forward.

Figure 2. Weekly Spot Price of Brent Sweet Crude ($ Per Barrel) and estimates of the prices OPEC/Petro States need to balance their budgets.

Dividing Neighbors

These components of the fossil fuel industry, and their associated feedstocks and pipelines, will continue to divide neighbors and countries as political disenfranchisement and inequality grow, the climate continues to change, and resource limitations put increasing stress on food security and watershed resiliency worldwide.

Not surprisingly, every one of these factors places more strain on countries and weakens their ability to govern responsibly.

Thus, many observers speculate that these factors are converging to create a kind of perfect storm that forces OPEC governments and their corporate partners to lean even more heavily on their respective militaries and for-profit private military contractors (PMCs) to prevent social unrest while insuring supply chain stability and shareholder return.[2,3] The increased reliance on PMCs to provide domestic security for energy infrastructure is growing and evolving to the point where in some countries it may be hard to determine where a state’s sovereignty ends and a PMC’s dominance begins – Erik Prince’s activities in the Middle East and Africa on China’s behalf and his recent aspirations for Afghanistan are a case in point.

To paraphrase Mark Twain, whiskey is for drinking and hydrocarbons are for fighting over.

The international and regional unaccountability of PMCs has added a layer of complexity to this conversation about energy security and independence. Countries such as Saudi Arabia and Venezuela provide examples of how fragile political stability is, and more importantly how dependent this stability is on oil refinery production and what OPEC is calling ‘New Optimism.’ To be sure, PMCs are playing an increasing role in political (in)stability and energy production and transport. Since knowledge and transparency are essential for peaceful resolutions, we will continue to map and chronicle the intersections of geopolitics, energy production and transport, social justice, and climate change.

By Ted Auch, Great Lakes Program Coordinator, FracTracker Alliance; and Bryan Stinchfield, Associate Professor of Organization Studies, Department Chair of Business, Organizations & Society, Franklin & Marshall College

Relevant Data

- Inventory of all 536 Global Oil Refineries: Download zip file

- Inventory of all Global Oil and Gas Shale Plays: Download zip file

Footnotes and References

- Assuming a tons of CO2 to barrels of oil per day ratio of 8.99 to 9.78 tons of CO2 per barrel of oil based on an analysis we’ve conducted of 146 refineries in the United States.

- B. Stinchfield. 2017. “The Creeping Privatization of America’s Armed Forces”. Newsweek, May 28th, 2017, New York, NY.

- R. Gray. “Erik Prince’s Plan to Privatize the War in Afghanistan”. The Atlantic, August 18th, 2017, New York, NY.

“These refineries are emitting roughly 260-283 billion metric tons (BMT) of CO2”

How can this be true if the total emissions from all sectors are only 50 billion tons of CO2 equivalent?

Excellent presentation. One minor suggestion: correct “Assuming the planet’s 7.6 billion people emit 4.9-5.0 metric tons of CO2 per year” to “4.9-5.0 metric tons per capita of CO2 per year”.