By Matt Kelso, Manager of Data & Technology

Kirk Jalbert, Manager of Community Based Research & Engagement

The Risks of Crude Oil Trains

As new oil fields boomed across North America in recent years, drillers looked for ways to get the product to refineries thousands of miles away. One solution was to use the nation’s rail infrastructure to ship hundreds of thousands of barrels of crude oil per day. The flow of oil was so great that thousands of additional tanker cars were ordered to get the oil to market. And yet, this solution of transporting crude by rail brought additional problems. Shipping large quantities of highly volatile and combustible crude oil on often antiquated rail lines has resulted in numerous accidents, at times spectacular in scale. In recent months, however, thousands of these oil tankers have been sitting idle on the tracks around the country, partially due to dropping oil prices, leading refineries to opt for cheaper imported oil and less expensive ways to get the domestic product to market such as through pipelines.

Communities Along the Tracks

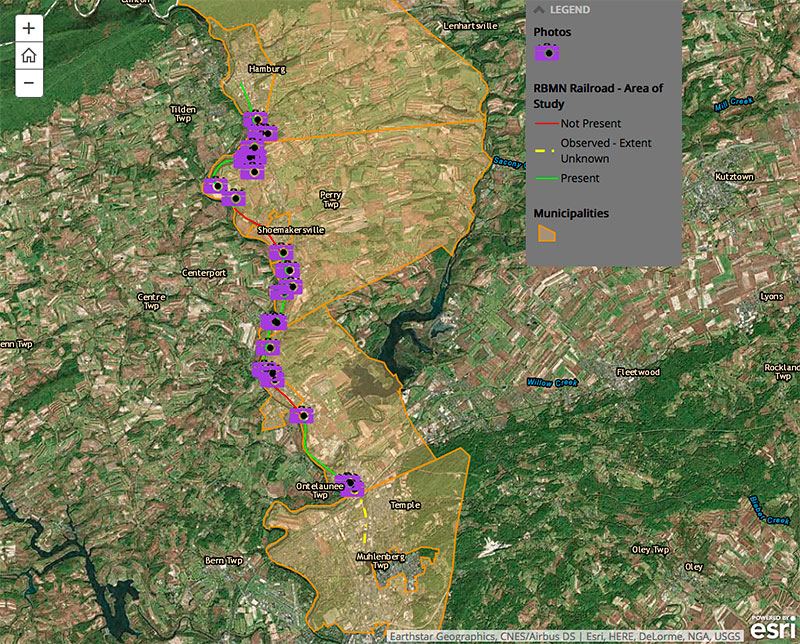

The interactive story map below investigates a stretch of oil trains that have been parked for months in close proximity to homes, schools, and busy intersections in Berks County, Pennsylvania. Altogether, 30,494 people live in the seven communities through which the tracks in question pass. We began this project in response to concerns from residents who contacted FracTracker for assistance in understanding why these trains were located in their community, what hazards they might pose, and to help people bring this story to the public to foster meaningful discussions about the risks of parked oil trains.

FracTracker has covered the risks of oil trains in a series of other articles. Click here to learn more.

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2015/10/Berks_BlogImage.jpg400900FracTracker Alliancehttps://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngFracTracker Alliance2015-10-08 11:22:372020-03-12 13:47:06Parked Oil Trains in Berks County, PA

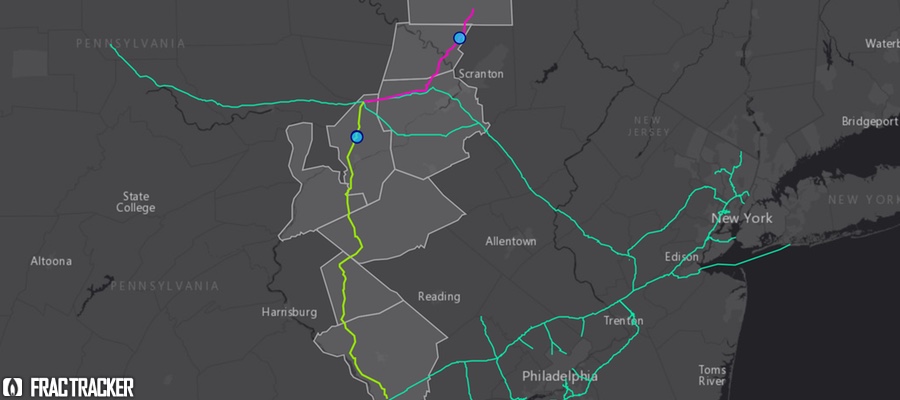

The Atlantic Sunrise Project or Central Penn Line is a natural gas pipeline Williams Companies has proposed for construction through eight counties of Central Pennsylvania. Williams intends to connect the Atlantic Sunrise to their two Transco pipelines, which extend from the northeast to the Gulf of Mexico. FracTracker discussed and mapped this controversial project as part of a blog entry in June of 2014; since then, the Atlantic Sunrise Project has been, and continues to be, a focus of unprecedented opposition. While supporters of the pipeline stress how it may enhance energy independence, economic growth, and job opportunities, opponents cite Williams’ poor safety records, their threats of eminent domain, and environmental hazards. This article provides details and maps pertaining to these threats and concerns.

Atlantic Sunrise: Project Overview

The Atlantic Sunrise Project would add 183 miles of new pipeline through the construction of the Central Penn Line North and the Central Penn Line South. The proposed Central Penn Line North (CPLN) begins in Susquehanna County, continues through Wyoming and Luzerne counties, and meets with the Transco Pipeline in Columbia County. With a 30 inch in diameter, it would allow for a maximum pressure of 1,480 psi (pounds per square inch). The proposed Central Penn Line South (CPLS) begins at the Transco Pipeline in Columbia County, and continues through Northumberland, Schuylkill, and Lebanon counties, ending in Lancaster. It would be 42 inches in diameter with a maximum pressure of 1,480 psi. The Atlantic Sunrise project also involves the construction of two new compressor stations, one in Clinton Township, Wyoming County, and the other in Orange Township, Columbia County. Finally, to accommodate the daily 1.7 million dekatherms (1 dekatherm equals 1,000 cubic feet of gas or slightly more than 1 million BTUs in energy) of additional natural gas that would flow through the system, the project proposes the expansion of 10 existing compressor stations along the Transco Pipeline in Pennsylvania, Maryland, Virginia, and North Carolina. Although the Atlantic Sunrise Pipeline would be entirely within Pennsylvania, it is permitted and regulated by the Federal Energy Regulatory Committee (FERC) because through its connection to the Transco Pipeline, it transports natural gas over state lines.

Updated Central Penn Pipeline Route

On March 31, 2015, Williams filed their formal application to FERC docket #CP15-138. Along with the formal application came changes to the pre-filing route of the pipeline that was submitted in the spring of 2014. The route of the Central Penn Line North has been modified since then by 21%, while the Central Penn Line South has been rerouted by 57%.

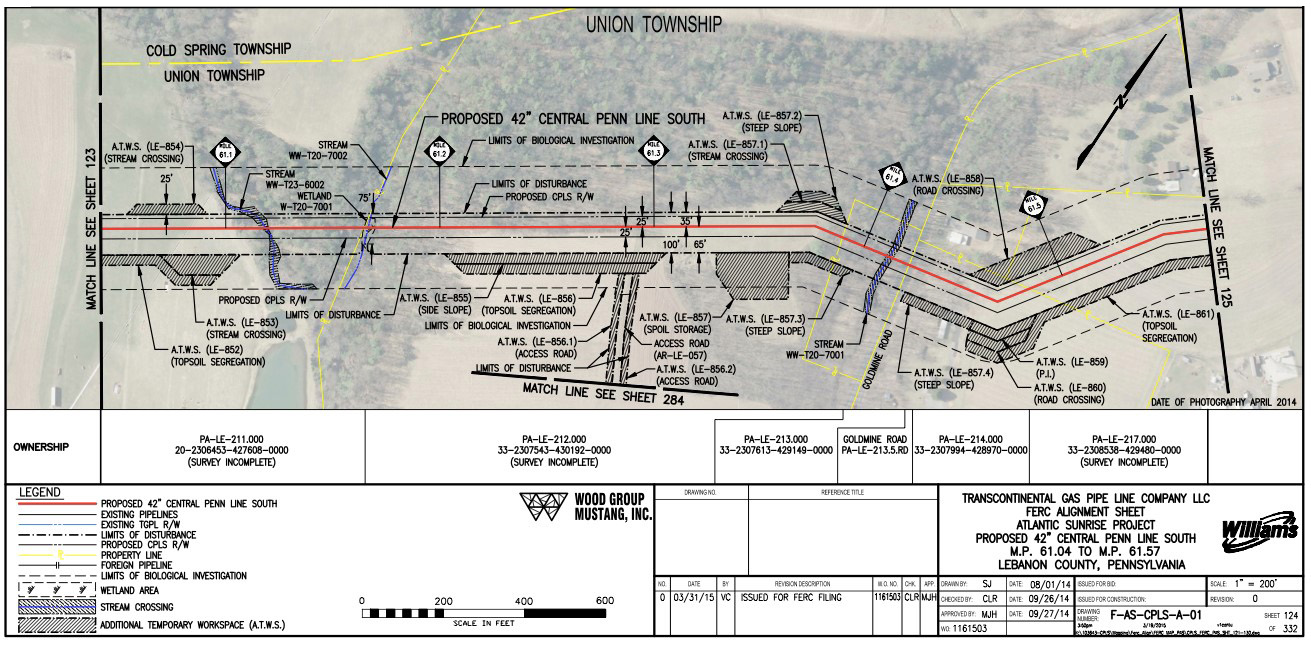

Williams’ application comprised of hundreds of attached documents, including pipeline alignment sheets for the entire route. Here is one example:

These alignment sheets show the extent of William’s biological investigation, the limits of disturbance, the occurrence of stream and wetland crossings, and any road or foreign pipeline crossings. Absent from the alignment sheets, however, is the area around the right-of-way that will be endangered by the presence of the pipeline. This is colloquially known as the “burn zone” or “hazard zone”.

What are “Hazard Zones”?

A natural gas pipeline moves flammable gas under extreme pressure, creating a risk of pipeline rupture and potential explosion. The “potential impact radius” or “hazard zone” is the approximate area within which there will be immediate damage in the case of an explosion. Should this occur, everything within the hazard zone would be incinerated and there would be virtually no chance of escape or survival. Based on pipeline diameter and pressure, the hazard zone can be calculated using the formula: potential impact radius = 0.69 * pipeline diameter * (√max pressure ).

Based on this formula, the hazard zone for the Central Penn Line North, with its diameter of 30 inches and maximum pressure of 1,480 psi, is approximately 796 feet (243 meters) on either side of the pipeline. The hazard zone for Central Penn Line South, with its diameter of 42 inches and maximum pressure of 1480 psi, is 1,115 feet (340 meters) on either side.

Many residents are unaware that their homes, workplaces, and schools are located within the hazard zone of the proposed Atlantic Sunrise Pipeline. Williams does not inform the public about this risk, primarily communicating with landowners along the right-of-way. The interactive, zoomable map (below) of the currently proposed route of the Atlantic Sunrise, Central Penn North and South pipelines depicts the pipeline right-of-way, as well as the hazard zones. The pipeline route was digitized using the alignments sheets included in Williams’ documents submitted to FERC. You can use this map to search home, work, and school addresses to see how the pipeline will affect residents’ lives and the lives of their communities.

Click in the upper right-hand corner of the map to expand to full-screen view, with a map legend.

Affected Communities

Landowners & Eminent Domain

Landowners along the right-of-way are among the most directly and most negatively impacted by the Atlantic Sunrise Pipeline, and other similar projects. Typically, people first become aware that a pipeline is intended to pass through their property when they receive a notice in the mail. Landowners faced with this news are on their own to negotiate with the company, navigate the FERC permitting and public comment process, and access unbiased and pertinent information. They face on-going stress, experiencing pressure from Williams to sign easement agreements, concern about the effects of construction on their property, and fear of living near explosive infrastructure. They must also consider costs of legal representation, decreases in property value, and limited options for mortgage and refinancing.

Sometimes, landowners in a pipeline’s right-of-way choose to not allow the company onto their property to conduct a survey. Landowners may also refuse to negotiate an agreement with the pipeline company. In response, the pipeline company can threaten to seize the property through the power of eminent domain, the federal power allowing private property to be taken if it is for the “public use.”

The law of eminent domain states that landowners whose properties are condemned must be fairly compensated for their loss. However, most landowners feel that in order to be fairly compensated by the company, they must hire their own land appraiser and attorney. This decision can be costly, however, and may not be an option for many people. The legitimacy of Williams’ intent to use eminent domain is contested by opponents of the project, who cite how “public use” of the property provides no positive local impacts. The Atlantic Sunrise Pipeline is intended to transport gas out of Pennsylvania through the Transco, so the landowners in its path will not benefit from it at all. Further, it connects to a network of pipelines leading to current export terminals in the Gulf of Mexico, as well as controversial planned export facilities like Cove Point, MD .

Throughout Pennsylvania, communities have responded to the expansion of pipelines, and to the threats of large companies like Williams. The need for landowner support has been addressed by organizations such as the Shalefield Organizing Committee, Energy Justice Network, the Clean Air Council, the Gas Drilling Awareness Coalition, and We Are Lancaster County. These organizations have worked to provide information, increase public awareness, engage with FERC, and develop resistance to the exploitation of Pennsylvania’s resources and residents. Director Scott Cannon of the Gas Drilling Awareness Coalition has documented firsthand the impacts of unconventional drilling in Pennsylvania through a short film series called the Marcellus Shale Reality Tour. The most recent in the series relates the stories of two landowners impacted by the Atlantic Sunrise Pipeline in the short film Atlantic Sunrise Surprise.

Environmental Review

Theoretically, environmental review of this proposed pipeline would be extensive. Primary decision-making on the future of the Atlantic Sunrise rests with FERC. Due to the National Environmental Policy Act of 1969 (NEPA), all projects overseen by federal agencies are required to prepare environmental assessments (EAs) or environmental impact assessments (EIAs). Because FERC regulates interstate pipelines, EA’s or EIA’s are required in their approval process. These assessments are conducted to accurately assess the environmental impacts of projects and to ensure that the proposals comply with federal environmental laws such as the Endangered Species Act, and the Clean Air and Water Acts. On the state level, the Pennsylvania Department of Environmental Protection (PA DEP) issues permits for wetlands and waterways crossings and for compressor stations on regional basis.

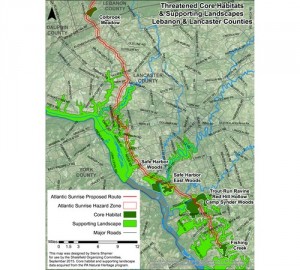

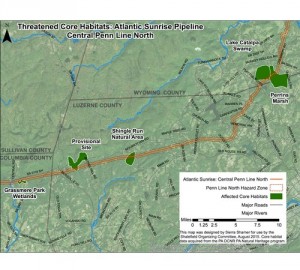

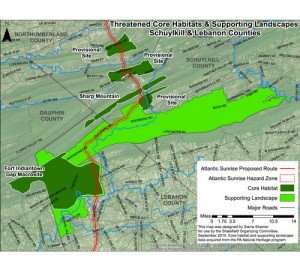

Core Habitats, Supporting Landscapes

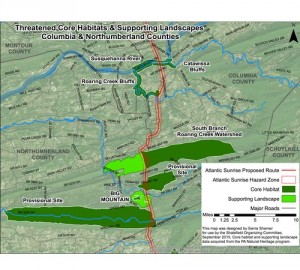

The route of the Atlantic Sunrise Pipeline will disturb numerous areas of ecological importance, including many documented in the County Natural Heritage Inventory (CNHI). The PA Department of Conservation and Natural Resources conducted the inventory to be used as a planning, economic, and infrastructural development tool, intending to avoid the destruction of habitats and species of concern. The following four maps show the CNHI landscapes affected by the current route of the Atlantic Sunrise pipeline (Figures 1-4).

Figure 1. Columbia & Northumberland counties

Figure 2. Lebanon & Lancaster counties

Figure 3. Threatened Core Habitats

Figure 4. Schuyklill & Lebanon counties

The proposed pipeline would disrupt core habitats, supporting landscapes, and provisional species-of-concern sites. According to the Natural Heritage Inventory report, core habitats “contain plant or animal species of state or federal concern, exemplary natural communities, or exceptional native diversity.” The inventory notes that the species in these habitats will be significantly impacted by disturbance activities. Supporting landscapes are defined as areas that “maintain vital ecological processes or habitat for sensitive natural features.” Finally, the provisional species of concern sites are regions where species have been identified outside of core habitat and are in the process of being evaluated. The Atlantic Sunrise intersects 16 core habitats, 12 supporting landscapes, and 6 provisional sites.

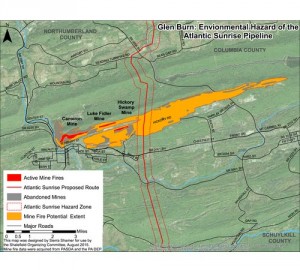

Active Mine Fires

Figure 5. Glen Burn Mine Fires

The current route of the Atlantic Sunrise intersects the Cameron/Glen Burn Colliery, considered to be the largest man-made mountain in the world and composed entirely of waste coal. This site also includes a network of abandoned mines, three of which are actively burning (Figure 5).

The pipeline right-of-way is roughly a half-mile from the closest burning mine, Hickory Swamp. These mine fire data were sourced from a 1988 report by GAI Consulting Inc. The time frame for the spread of the mine fires is unknown, and dependent on environmental factors. Mine subsidence — when voids in the earth created by mines cause the surface of the earth to collapse — is another issue of concern. Routing the pipeline through this unstable area adds to the risk of constructing the pipeline through the Glen Burn region.

Looking Ahead

The Atlantic Sunrise Project has received an unprecedented level of resistance that continues to grow as awareness and information about the threats and hazards develops. While Williams, FERC, and the PA DEP negotiate applications and permits, work is also being done by many non-profit, research, and grassroots organizations to investigate the environmental, cultural, and social costs of this pipeline. We will follow up with more information about this project as it becomes available.

This article was written by Sierra Shamer, an environmental mapper and activist. Sierra is a member of the Shalefield Organizing Committee and holds two degrees from the University of Maryland, Baltimore County: a B.A. in environmental studies and an M.S. in geography and environmental systems.

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2015/10/Atlantic-Shamer-Feature.jpg400900Guest Authorhttps://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngGuest Author2015-10-07 09:31:152020-03-12 17:39:30Maps of Updated Central Penn Pipeline Emphasize Threats to Residents and Environment

Oil, Gas, and Brine Oh My! By Ted Auch, Great Lakes Program Coordinator, FracTracker Alliance

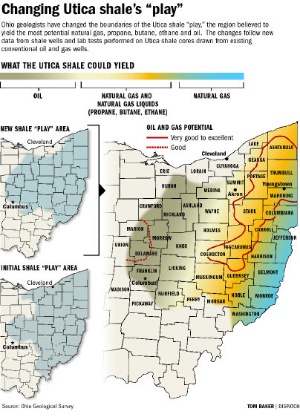

It was just three years ago that the Ohio Geological Survey (OGS) and Department of Natural Resources (DNR) were proposing – and expanding – their bullish stance on the potential Utica Shale oil and gas production “play.” Back in April 2012 both agencies continue[d] to redraw their best guess, although as the Ohio Geological Survey’s Chief Larry Wickstrom cautioned, “It doesn’t mean anywhere you go in the core area that you will have a really successful well.”

What we found is that the OGS projections have not held up to their substantial claims. And here is why…

Background

The Geological Survey eventually parsed the Utica play into pieces:

a large oil component encompassing much of the central part of the state,

natural gas liquids from Ashtabula on the Pennsylvania border southwest to Muskingum, Guernsey, and Noble Counties, and

natural gas counties, primarily, along the Ohio River from Columbiana on the Pennsylvania-West Virginia border to Washington County in the Southeast quarter of the state.

Columbus Dispatch Utica Shale “play” map

Fast forward to the first quarter of 2015 and we have a very healthy dataset to begin to model and validate/refute these projections. Back in 2009 Wickstrom & Co. only had 53 Utica Shale laterals, while today Ohio is host to 962 laterals from which to draw our conclusions. The preponderance of producing wells are operated by Chesapeake (463), Gulfport (118), Antero Resources (62), Eclipse Resources (41), American Energy Utica (36), Consol (35), and R.E. Gas Development (34), with an additional 13 LLCs and 10 publicly traded companies accounting for the remaining 173 producing laterals. A further difference between the following analysis and the OGS one is that we looked at total production and how much oil and gas was produced on a per-day basis.

Analysis

Using an interpolative geostatistical technique known as Empirical Bayesian Kriging and the 962 lateral dataset, we modeled total and per day oil, gas, and brine production for Ohio’s Utica Shale between 2011 and Q1-2015 to determine if the aforementioned map redrawing holds up, is out-of-date, and/or is overly optimistic as is generally the case with initial O&G “moving target” projections.

Days of Activity & Brine Production

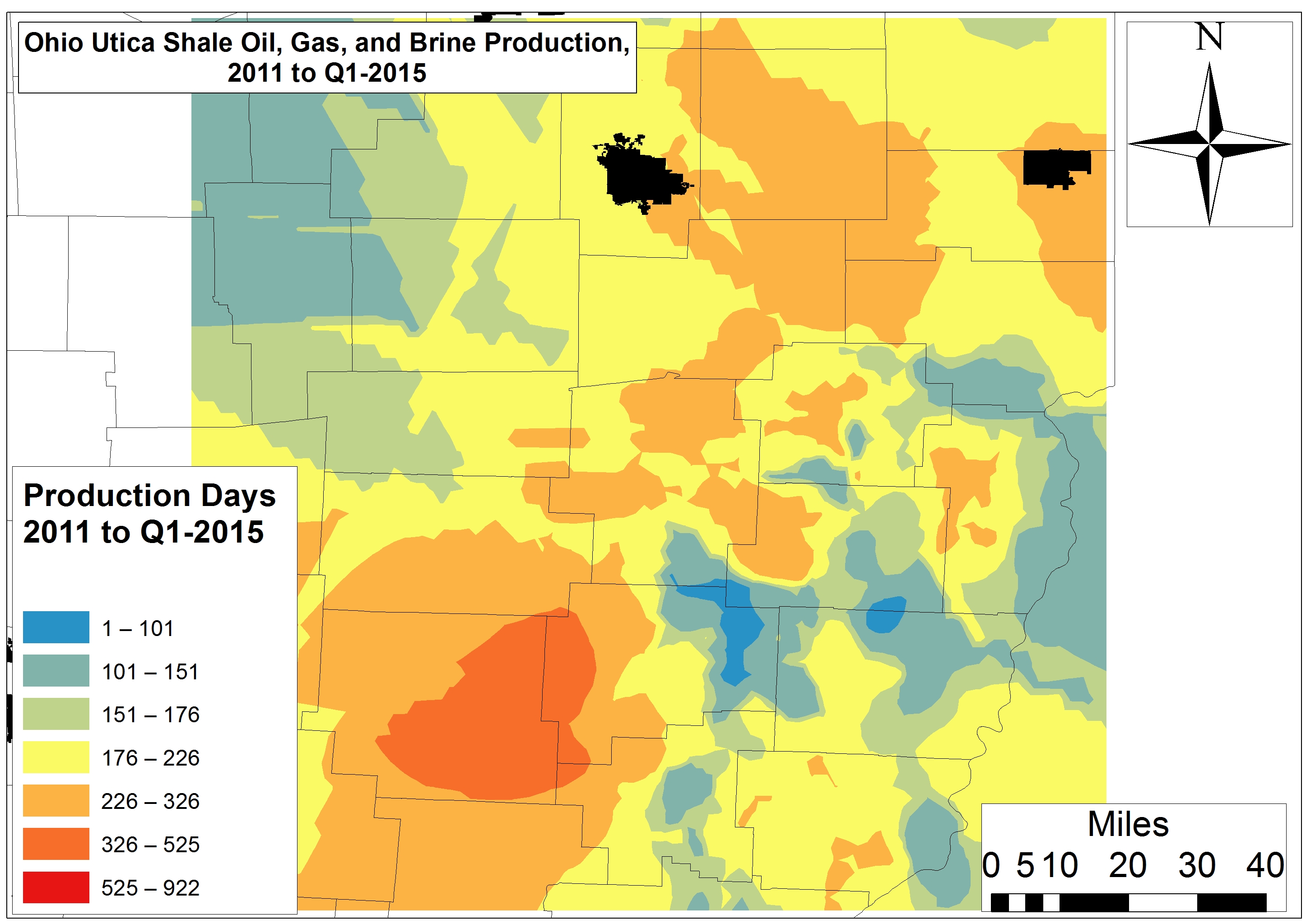

The most active regions of the Utica Shale for well pad activity has been much of Muskingum County and its border with Guernsey and Noble counties; laterals are in production every 1 in 2.1-3.4 days. Conversely, the least active wells have been drilled along the Harrison-Belmont border and the intersection between Harrison, Tuscarawas, and Guernsey counties.

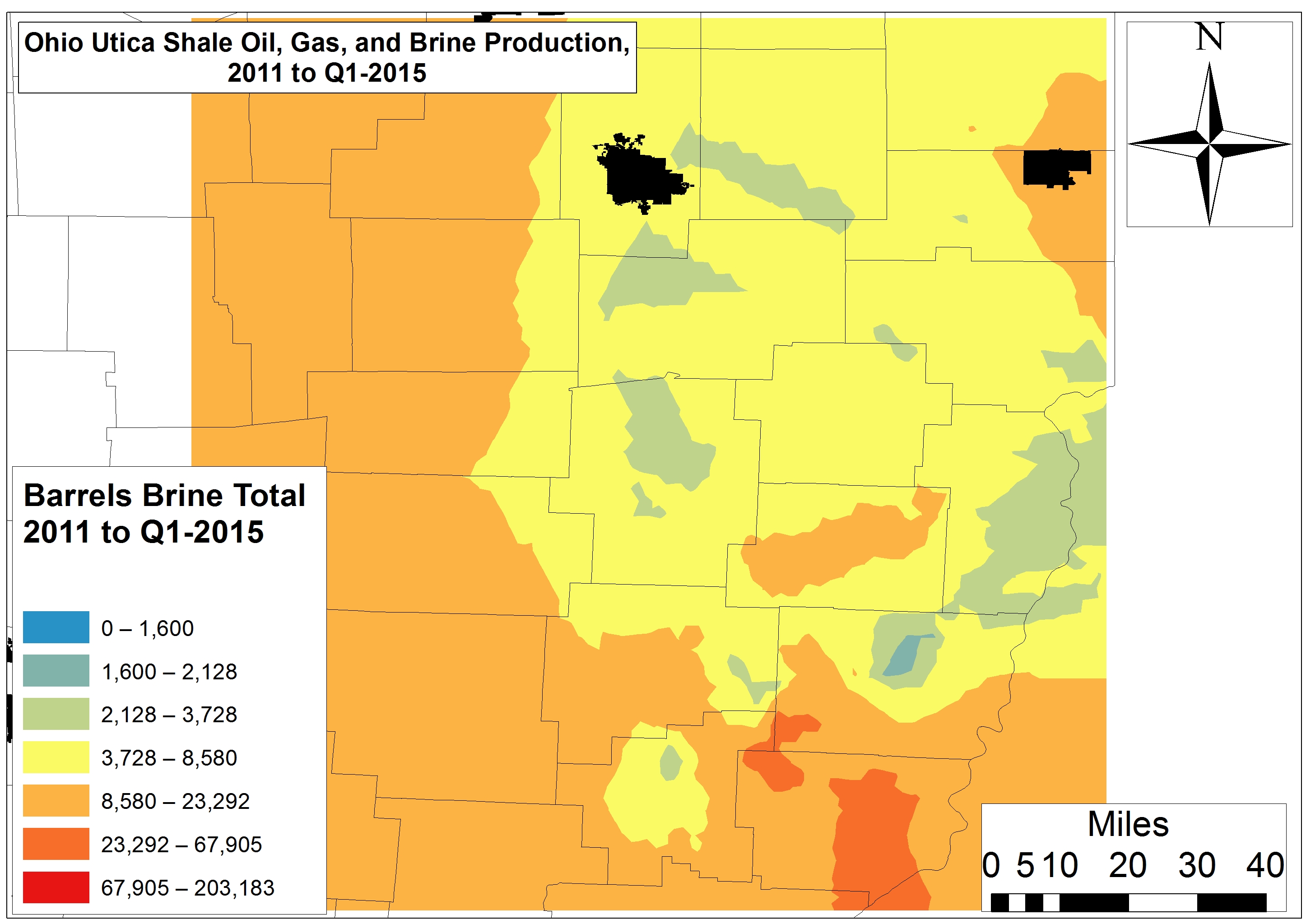

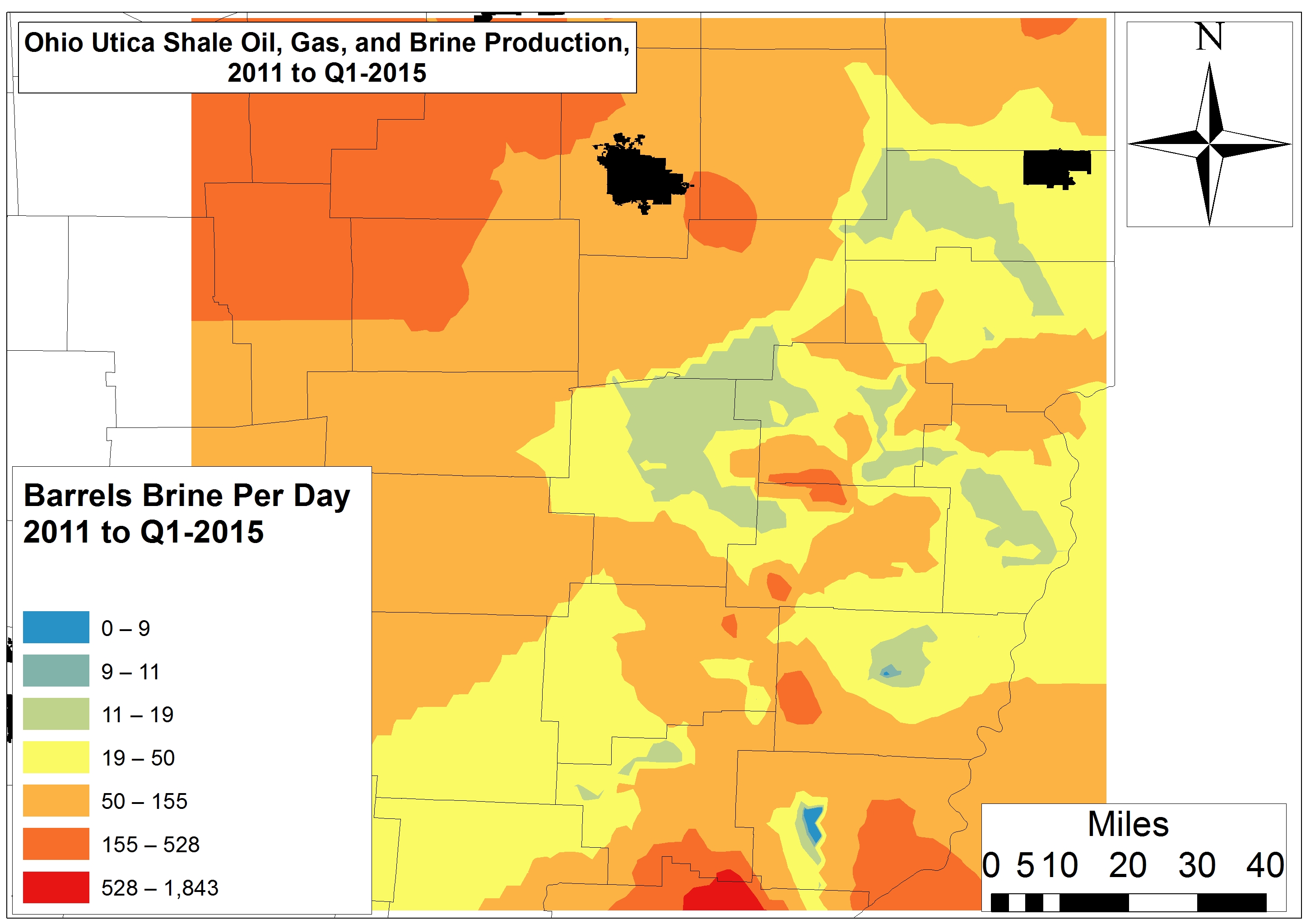

Brine is a form of liquid drilling waste characterized by high salt loads and total dissolved solids. The laterals that have produced the most brine to date are located in a large section of Monroe County and at the intersection of Belmont, Monroe, and Noble counties, with total brine production amounting to 23,292 barrels or 734,000-978,000 gallons (Fig. 1).

Figure 1. Total Ohio Utica Shale Oil, Gas, and Brine Production 2011 to Q1-2015

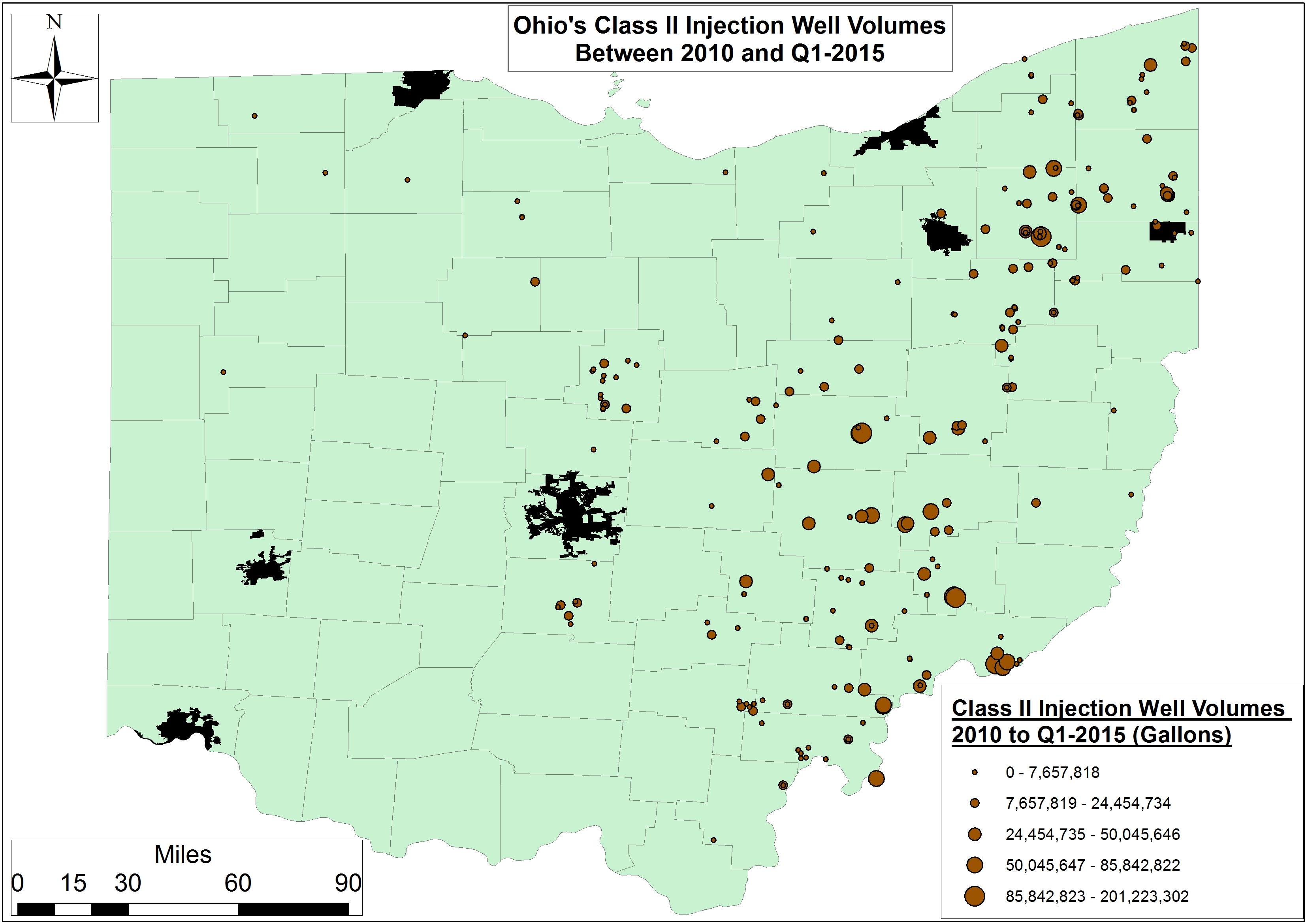

This area is also one of the top three regions of the state with respect to Class II Injection volumes; the other two high-brine production regions are Morrow and Portage counties to the west and southwest, respectively (Fig. 2).

Figure 2. Layout & Volume (2010 to Q1-2015, Gallons) of Ohio’s Active Class II Injection Wells

However, on a per-day basis we are seeing quite a few inefficient laterals across the state, including Devon Energy’s Eichelberger and Richman Farms laterals in Ashland and Medina counties. Ashland and Medina are producing 230-270 barrels (8,453-9,923 gallons) of brine per day. In Carroll County, one of Chesapeake’s Trushell laterals tops the list for brine production at 1,843 barrels (67,730 gallons) per day. One of Gulfport’s Bolton laterals in Belmont County and EdgeMarc’s Merlin 10PPH in Washington County are generating 1,100-1,200 barrels (40,425-44,100 gallons) of brine per day.

Oil & Gas Production

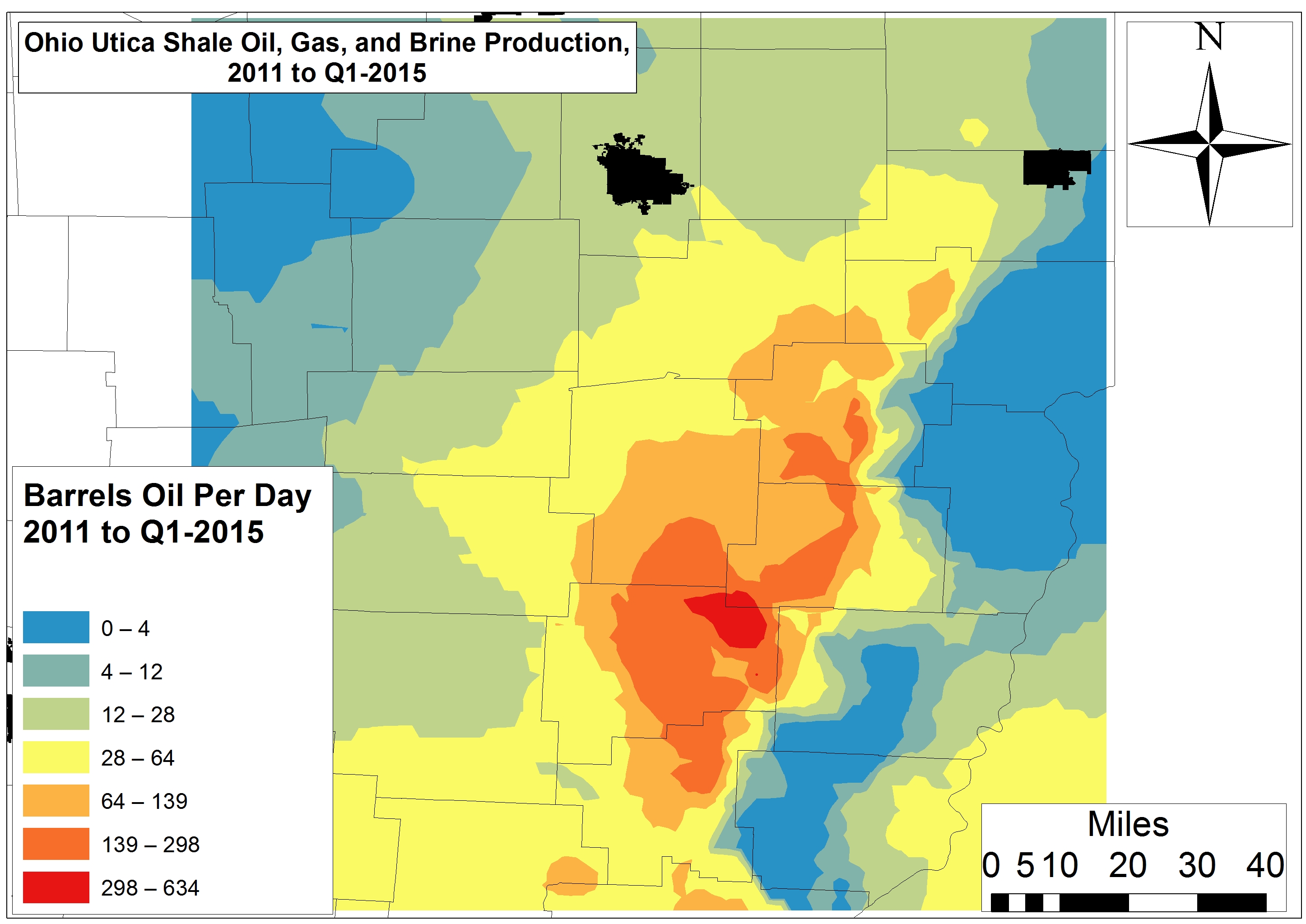

Since the last time we modeled production the oil hotspots have shrunk. They have also become more discrete and migrated southward – all of this in contrast to the model proposed by the OGS in 2012. The areas of greatest productivity (i.e., >26,000 barrels of oil) are not the central part of the state, but rather Tuscarawas, Harrison, Guernsey, and Noble counties (Fig. 1). The intersection of Harrison, Tuscarawas, and Guernsey counties is where oil productivity per-day is highest – in the range of 300-630+ barrels (Fig. 3). The areas that the OGS proposed had the highest oil potential have produced <600 barrels total or <12 barrels per day.

Figure 3. Per-Day Ohio Utica Shale Oil, Gas, and Brine Production 2011 to Q1-2015

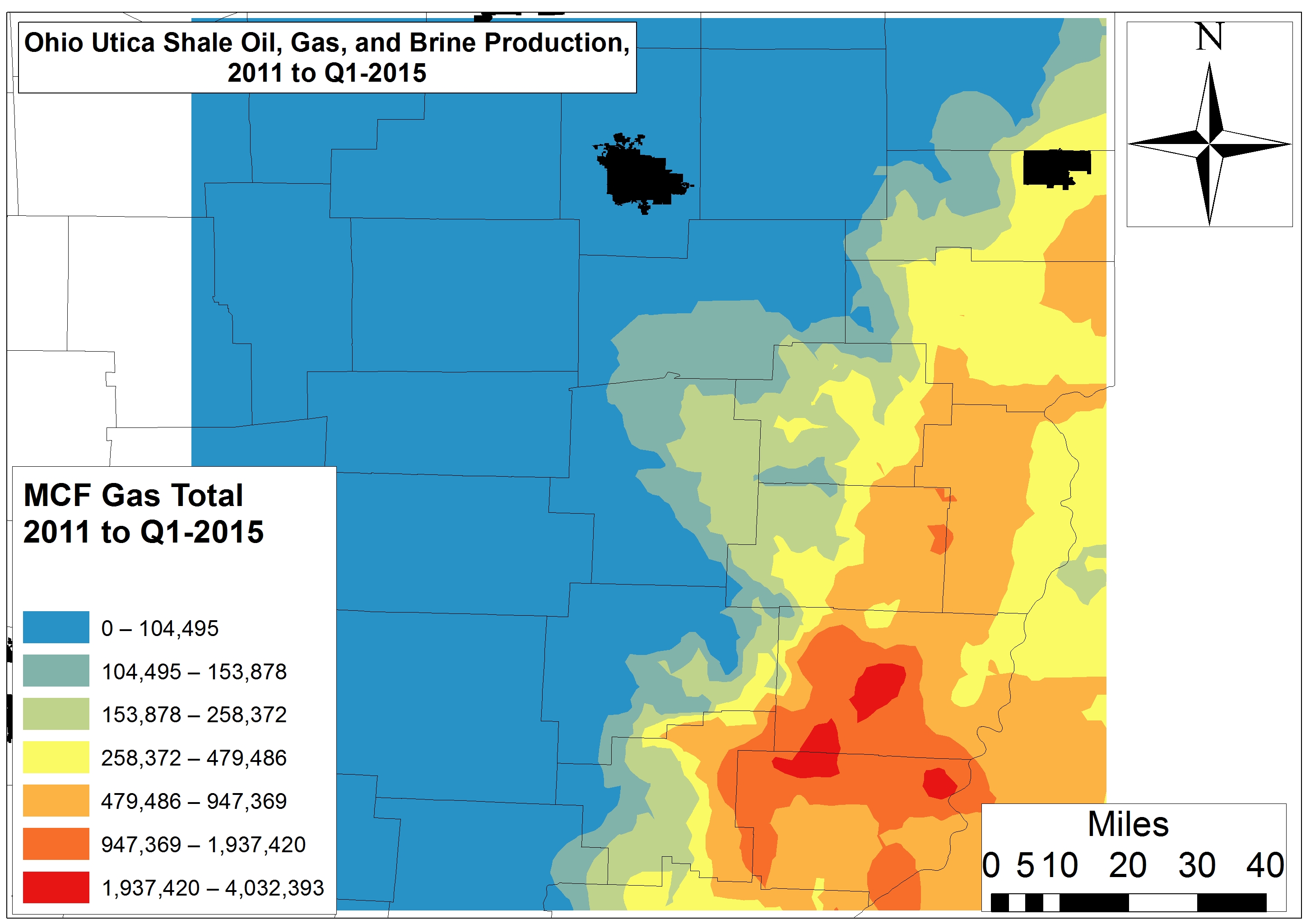

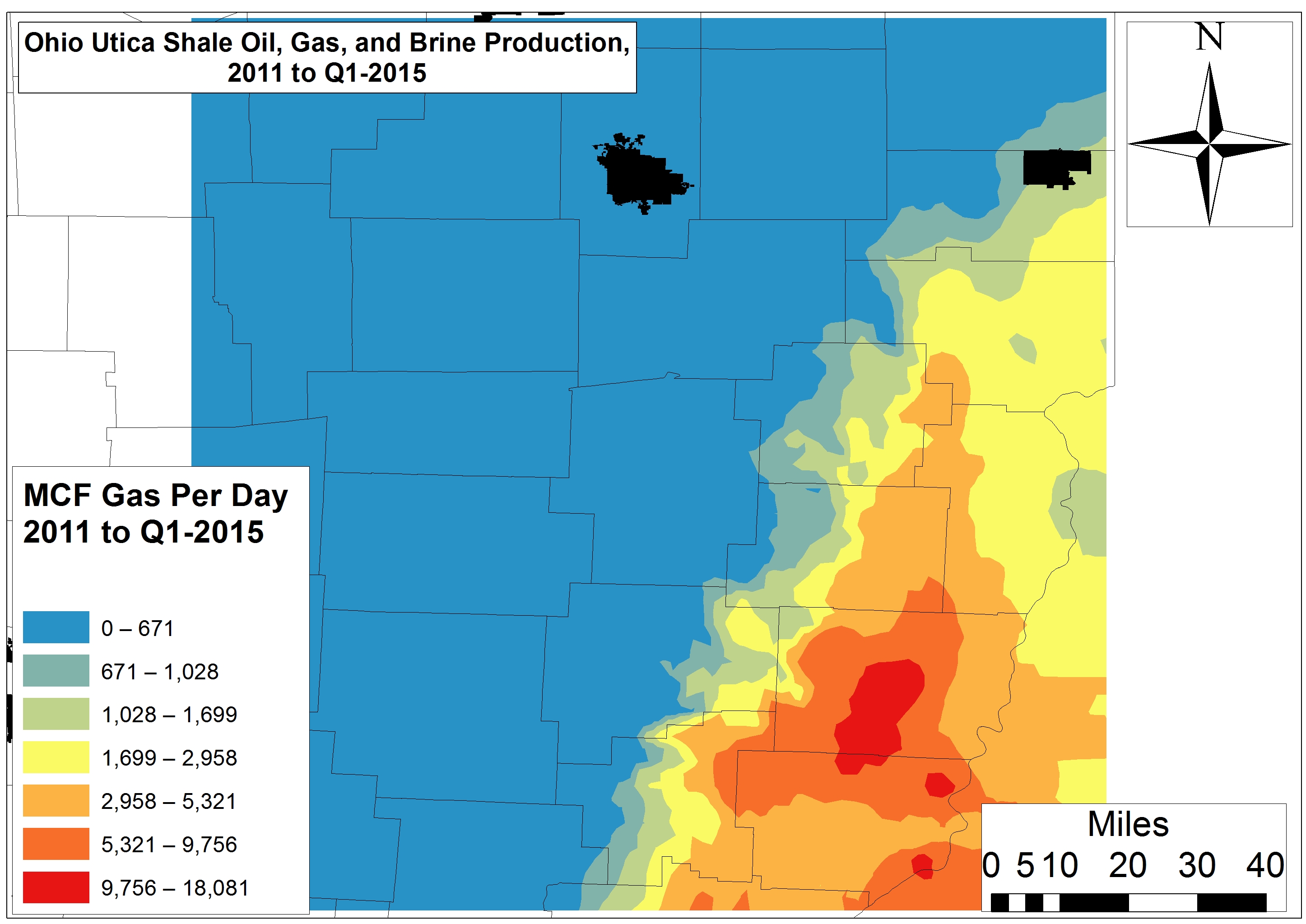

The OGS natural gas region has proven to be another area of extremely low oil productivity.

Natural gas productivity in the Utica Shale is far less extensive than the OGS projected back in 2012. High gas production is restricted to discreet areas of Belmont and Monroe counties to the tune of 947,000-4.1 million Mcf to date – or 5,300-18,100 Mcf per day. While the OGS projected natural gas and natural gas liquid potential all the way from Medina to Fairfield and Perry counties, we found a precipitous drop-off in productivity in these counties to <1,028 Mcf per day (<155,000 Mcf total from 2011 to Q1-2015) or a mere 6-11% of the Belmont-Monroe sweet spot.

Conclusion: A Shrinking Utica Shale Play

Simply put, the OGS 2012 estimates:

Have not held up,

Are behind the times and unreliable with respect to citizens looking to guestimate potential royalties,

Were far too simplistic,

Mapped high-yield sections of the “play” as continuous when in fact productive zones are small and discrete,

Did not differentiate between per day and total productivity, and

Did not address brine waste.

These issues should be addressed by the OGS and ODNR on a more transparent and frequent basis. Combine this analysis with the disappointing returns Ohio’s 17 publicly traded drilling firms are delivering and one might conclude that the structural Utica Shale bubble is about to burst. However, we know that when all else fails these same firms can just “lever up,” like their Rocky Mountain brethren, to maintain or marginally increase production and shareholder happiness. Will these Red Queens of the O&G industry stay ahead of the Big Bank and Private Equity hounds on their trail?

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2015/09/OH-Shrinking2-Feature.jpg400900Ted Auch, PhDhttps://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngTed Auch, PhD2015-09-29 15:29:212020-03-12 17:39:58The Curious Case of the Shrinking Utica Shale Play

FracTracker Alliance worked with Public Herald this spring to update and map oil and gas complaints filed by citizens to the Pennsylvania Department of Environmental Protection (PA DEP) as of March 2015. The result is the largest release of oil and gas records on water contamination due to fracking in PA. Additionally, Public Herald’s investigation revealed evidence of Pennsylvania state officials keeping water contamination related to fracking “off the books.”

The mission of Public Herald, an investigative news non-profit formed in 2011, is two-fold: truth + creativity. Their work uses investigative journalism and art to empower readers and hold accountable those who put the public at risk. For this project, Public Herald aims to improve the public’s access to oil and gas information in PA by way of file reviews and data digitization. Public Herald maintains an open source website called #fileroom, where people can access a variety of digital information originally housed on paper within the PA DEP. This information is collected and synthesized with the help of donors, journalists and researchers in a collective effort with the community. To date, these generous volunteers have already donated more than 2,000 hours of their time collecting records.

The site includes complaints, permits, waste, legal cases, and gas migration investigations (GMI) conducted by the PA DEP. Additionally, there is a guide on how to conduct file reviews and how to access information through the “Right-to-Know” law at the PA DEP. They have broken down complaints and permits by county; wastes and GMI categories by cases, all of which include test results from inspections; and correspondence and weekly reports.

Some partners and contributors to the file team include Joshua Pribanic as the co-founder and Editor-in Chief, Melissa Troutman as co-founder and Executive Director, John Nicholson, who collects and researches for several databases, Nadia Steinzor as a contributor through Earthworks, and many more. Members of FracTracker working on this project include Matt Kelso, Samantha Rubright, and Kirk Jalbert.

#fileroom’s update expands the number of complaint data records collected to 18 counties – and counting!

Over the past few years, oil train traffic across the continent has increased rapidly with more than 500,000 rail cars moving oil in 2014 alone, according to the Association of American Railroads. The recent Lac-Mégantic, Quebec disaster and subsequent accidents illustrate the severity of this issue. There is a pressing need to determine true hazards facing our communities and to develop solutions to prevent further disasters. Across the United States and Canada, the issue of oil trains has quickly risen onto the agenda of community leaders, safety experts, researchers, and concerned citizens. There is much to discover and share about protecting people and vulnerable places from the various risks these trains pose. Oil Train Response 2015 provides two invaluable forums on this most pressing problem and provides information and insights for every audience.

November 13, 2015

Community Risks & Solutions Conference Presented by The Heinz Endowments

November 14 & 15, 2015

Activist Training Weekend Presented by ForestEthics

The one-day conference presented by The Heinz Endowments invites all interest groups to hear from experts about the scale and scope of this challenge, as well as updates on the current regulatory and legal frameworks; consider case studies about the actions/measures taken by various communities in response; and, participate in discussion sessions to explore solutions to better safeguard communities. Elected officials, regulators, and emergency response professionals from Pennsylvania and beyond are especially encouraged to attend to take advantage of this important learning and networking opportunity.

Training – November 14-15th

Saturday, Nov. 14th: Training 7:30 AM – 5:00 PM. Reception 6:00 – 8:00 PM

Sunday, Nov. 15th: Training 7:30 AM – 2:00 PM

A two-day training presented by ForestEthics will equip grassroots and NGO leaders from across the nation with better skills to take back to their communities, and provide critical opportunities for attendees to share winning strategies with each other. In the process of sharing, the conference will help to build both the oil train movement and support the broader environmental and social justice movements. Areas of strategic focus will include: organizing, communications, spokesperson training, data management for organizers, legal strategies, and crowd-sourced train tracking. It will also provide a structured forum for advocates fighting specific oil terminal proposals in places like Philadelphia, Baltimore, and Albany to develop shared strategies and tactics and provide all participants with the skills, knowledge and contacts they will need to carry on this work once they return home.

Oil trains are a major environmental justice issue. The conference and training will speak directly to environmental justice concerns and be inclusive of communities of color, economically disadvantaged urban and rural regions, and communities already experiencing environmental inequities. To this end, need-based travel scholarships will be provided. We are committed to developing the agenda in close consultation with our allies and attendees so that it meets their needs.

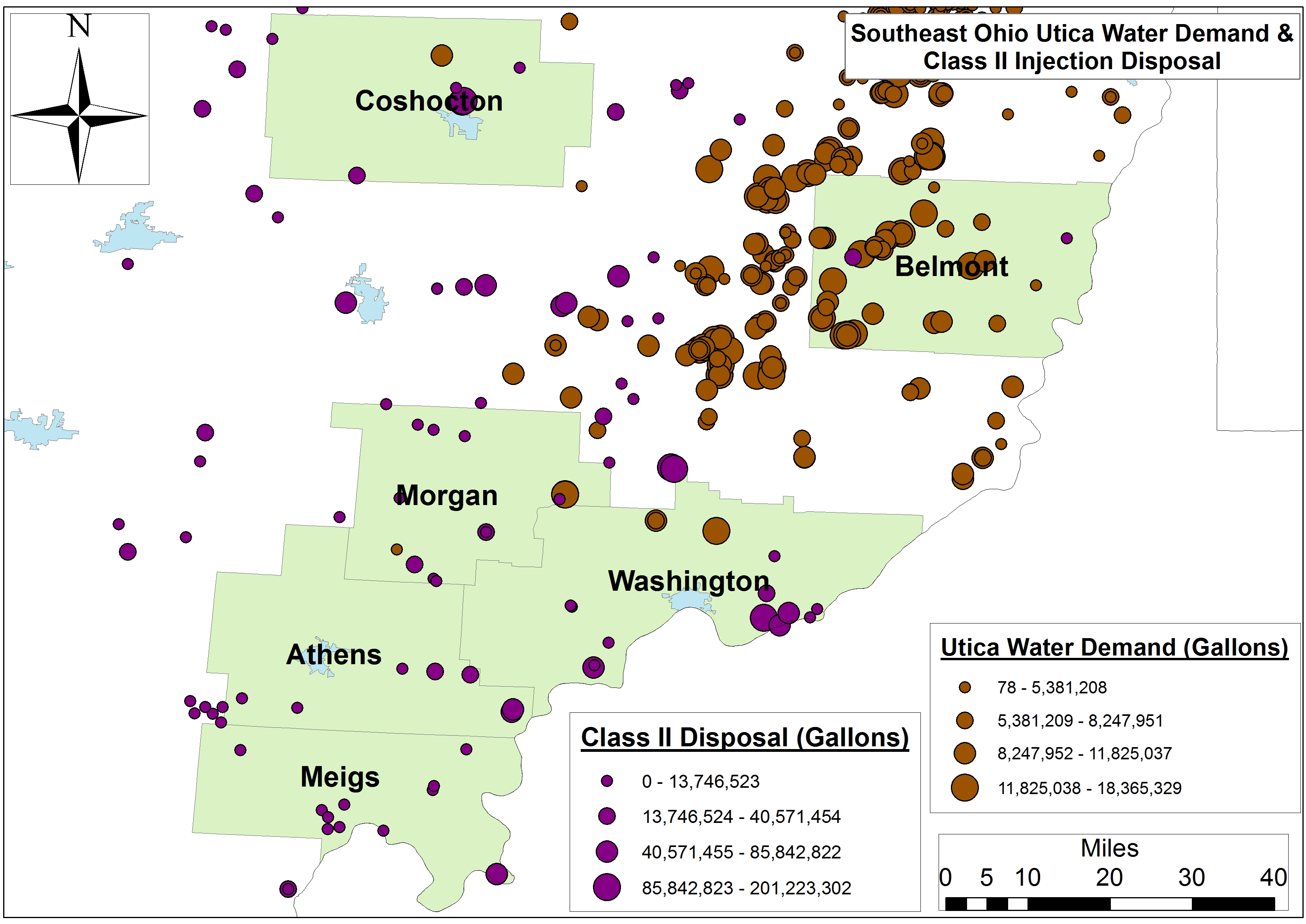

Ohio waterways face headwinds in the form of hydraulic fracturing water demand and waste disposal

By Ted Auch, PhD – Great Lakes Program Coordinator, and Elliott Kurtz, GIS Intern and University of Michigan Graduate Student

In just 44 of its 88 counties, Ohio houses 1,134 wells – including those producing oil and natural gas and Class II injection wells into which the industry’s waste is disposed. Last month we wrote about Ohio’s disturbing fracking waste disposal trend and the disproportionate influence of neighboring states. (Prior to that Ariel Conn at Virginia Tech outlined the relationship between Class II Injection Wells and induced seismicity on FracTracker.) This time around, we are digging deeper into how water demand is related to Class II disposal trends.

Ohio’s Utica oil and gas wells are using 7 million gallons of freshwater – or 2.4-2.8 million more than the average well cited by the US EPA.1 Below we explore the inter-county differences of the water used in these oil and gas wells, and how demand compares to residential water demand and wastewater production.

Please refer to Table 1 at the end of this article regarding the following findings.

Utica Shale Freshwater Demand

Data indicate that there may be serious threats to Ohio’s water security on the horizon due to the oil and gas industry.

The counties of Guernsey and Monroe are next up with water demand and waste water generation at rates of 14.6 and 10.3 million gallons per year. However, the 11.4 million gallons of freshwater demand and fracking waste produced by these two counties 114 Utica and Class II wells still accounts for roughly 81% of residential water demand.

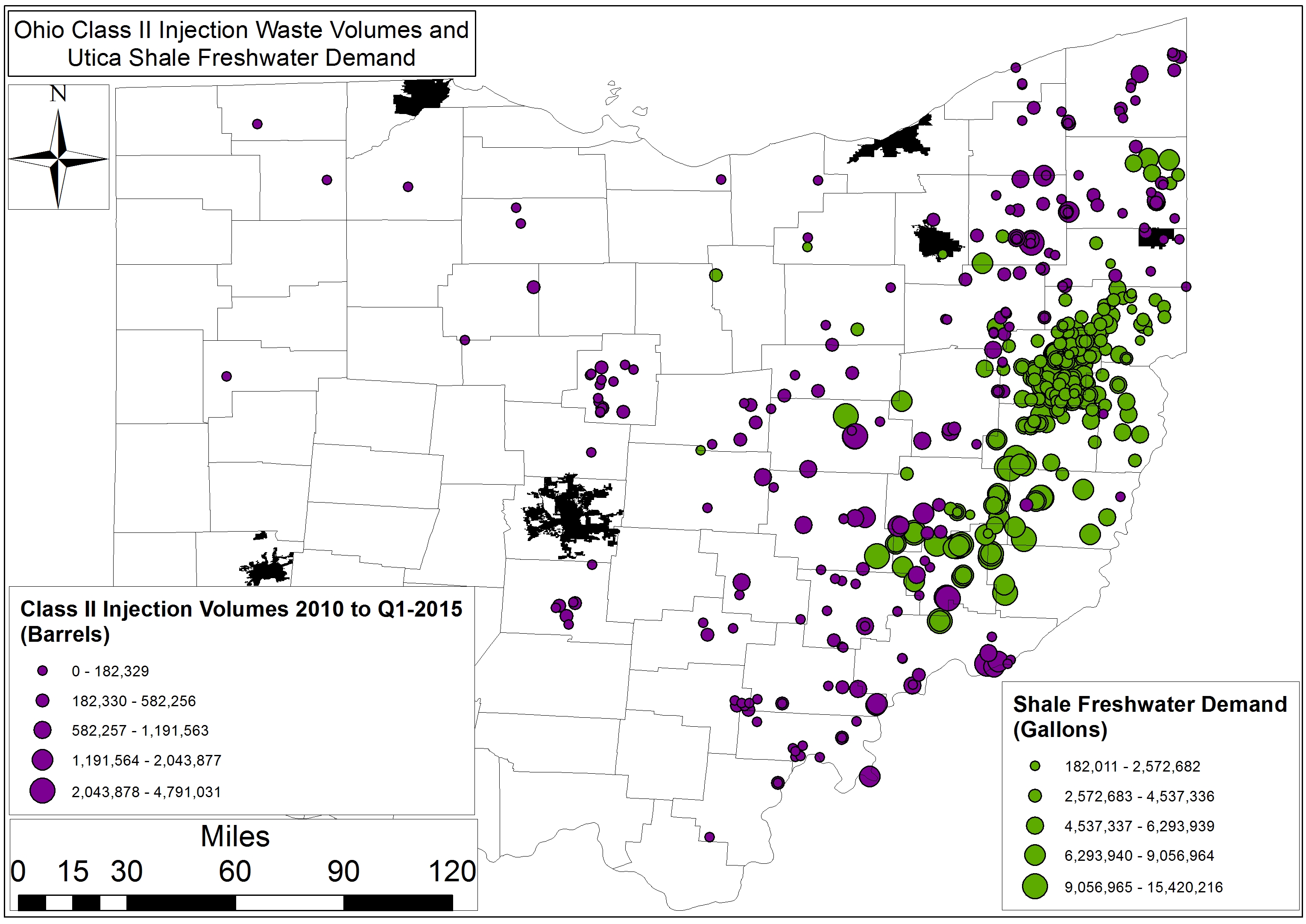

The wells within the six-county region including Meigs, Washington, Athens, and Belmont along the Ohio River use 73 million gallons of water and generate 51 million gallons of wastewater per year, while the hydraulic fracturing industry’s water-use footprint ranges between 48 and 17% of residential demand in Coshocton and Athens, respectively. Class II Injection well disposal accounts for a lion’s share of this footprint in all but Belmont County, with injection well activities equaling 77 to 100% of the industry’s water footprint (see Figure 1 for county locations and water stress).

Figure 1. Primary Southeast Ohio counties experiencing Utica Shale and Class II water stress

The next eight-county cohort is spread across the state from the border of Pennsylvania and the Ohio River to interior Appalachia and Central Ohio. Residential water demand there equals 428 million gallons, while the eight county’s 92 Utica and 90 Class II wells have accounted for 15 million gallons of water demand and disposal. Again the injection well component of the industry accounts for 5.8% of the their 7.7% footprint relative to residential demand. The range is nearly 10% in Vinton and 5.3% in Jefferson County.

The next cohort includes twelve counties that essentially surround Ohio’s Utica Shale region from Stark and Mahoning in the Northeast to Pickaway, Hocking, and Gallia along the southwestern perimeter of “the play.” These counties’ residents consume 405 million gallons of water and generate 329 million gallons of wastewater annually. Meanwhile the industry’s 69 Class II wells account for 53 million gallons – a 2.8% water footprint.

Finally, the 11 counties with the smallest Utica/Class II footprint are not suprisingly located along Lake Erie, as well as the Michigan and Indiana border, with water demand and wastewater production equalling nearly 117 billion gallons per year. Meanwhile the region’s 3 Utica and 18 Class II wells have utilized 59 million gallons. These figures equate to a water footprint of roughly 00.15%, more aligned with the 1% of total annual water use and consumption for the hydraulic fracturing industry cited by the US EPA this past June.

Future Concerns and Projections

Industry will see their share of the region’s hydrology increase in the coming months and years given that injection well volumes and Utica Shale demand is increasing by 1.04 million gallons and 405-410 million gallons per quarter per well, respectively. The number of people living in these 42 counties is declining by 0.6% per year, however, 1.4% in the 10 counties that have seen the highest percentage of their water resources allocated to Utica and Class II operations. Additionally, hydraulic fracturing permitting is increasing by 14% each year.2

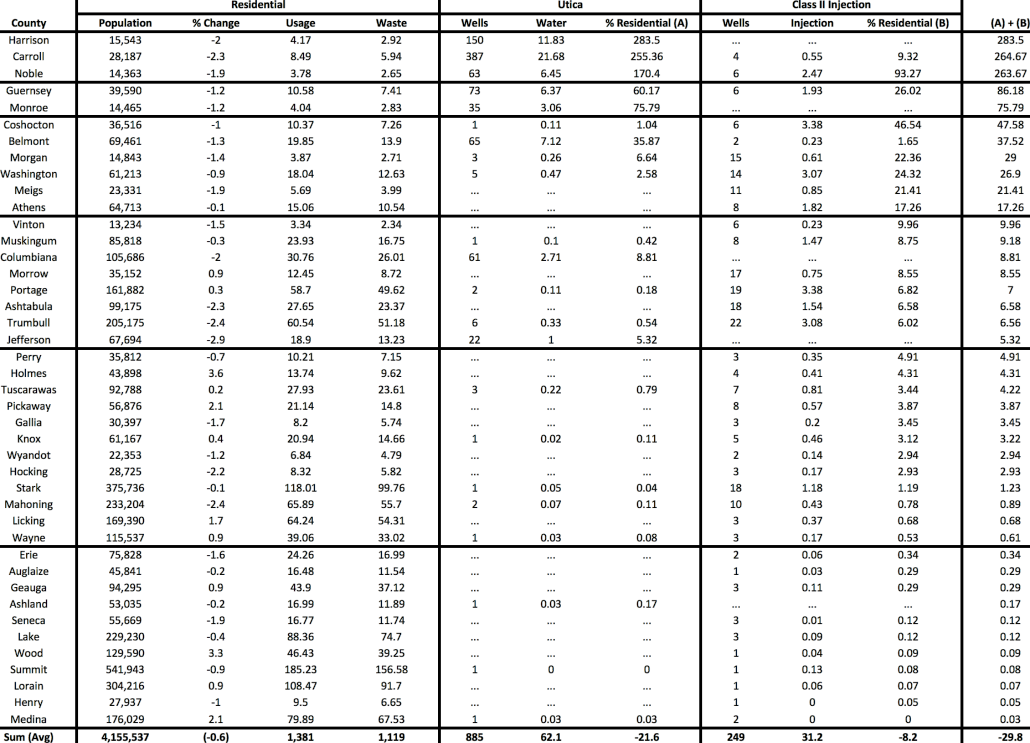

Table 1. Residential, Utica Shale, and Class II Injection well water footprint across forty-two Ohio Counties (Note: All volumes are in millions of gallons)

2. Auch, W E, McClaugherty, C, Gallemore, C, Berghoff, D, Genshock, E, Kurtz, E, & Jurjus, R. (2015). Ramification of current and future production, resource utilization, and land-use change in the Ohio Utica Shale Basin. Paper presented at the National Environmental Monitoring Conference, Chicago, IL.

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2015/08/InjectionWells-Feature.jpg400900Ted Auch, PhDhttps://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngTed Auch, PhD2015-08-11 10:42:442020-03-12 14:04:43Threats to Ohio’s Water Security

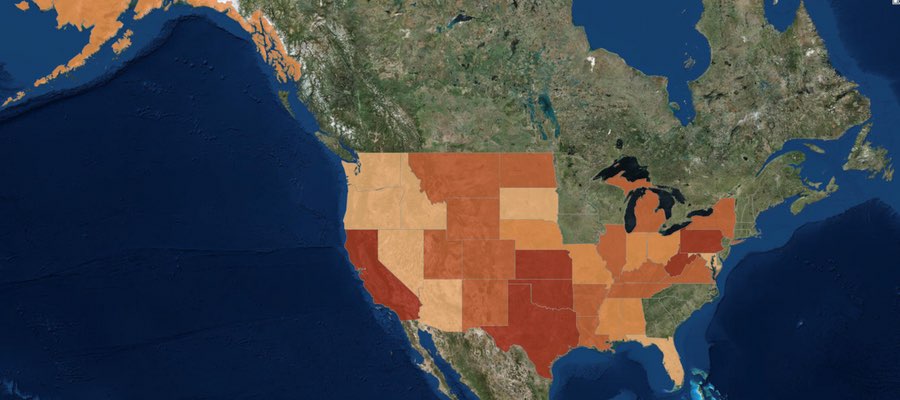

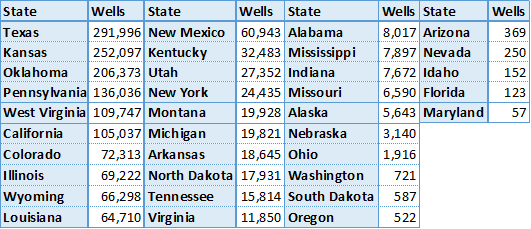

In February 2014, the FracTracker Alliance produced our first version of a national well data file and map, showing over 1.1 million active oil and gas wells in the United States. We have now updated that data, with the total of wells up to 1,666,715 active wells accounted for.

Density by state of active oil and gas wells in the United States. Click here to access the legend, details, and full map controls. Zoom in to see summaries by county, and zoom in further to see individual well data. Texas contains state and county totals only, and North Carolina is not included in this map.

While 1.7 million wells is a substantial increase over last year’s total of 1.1 million, it is mostly attributable to differences in how we counted wells this time around, and should not be interpreted as a huge increase in activity over the past 15 months or so. Last year, we attempted to capture those wells that seemed to be producing oil and gas, or about ready to produce. This year, we took a more inclusive definition. Primarily, the additional half-million wells can be accounted for by including wells listed as dry holes, and the inclusion of more types of injection wells. Basically anything with an API number that was not described as permanently plugged was included this time around.

Data for North Carolina are not included, because they did not respond to three email inquiries about their oil and gas data. However, in last year’s national map aggregation, we were told that there were only two active wells in the state. Similarly, we do not have individual well data for Texas, and we use a published list of well counts by county in its place. Last year, we assumed that because there was a charge for the dataset, we would be unable to republish well data. In discussions with the Railroad Commission, we have learned that the data can in fact be republished. However, technical difficulties with their datasets persist, and data that we have purchased lacked location values, despite metadata suggesting that it would be included. So in short, we still don’t have Texas well data, even though it is technically available.

Wells by Type and Status

Each state is responsible for what their oil and gas data looks like, so a simple analysis of something as ostensibly straightforward as what type of well has been drilled can be surprisingly complicated when looking across state lines. Additionally, some states combine the well type and well status into a single data field, making comparisons even more opaque.

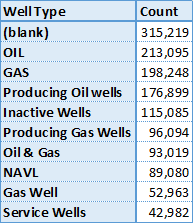

Top 10 of 371 published well types for wells in the United States.

Among all of the oil producing states, there are 371 different published well types. This data is “raw,” meaning that no effort has been made to combine similar entries, so “gas, oil” is counted separately from “GAS OIL,” and “Bad Data” has not been combined with “N/A,” either. Conforming data from different sources is an exercise that gets out of hand rather quickly, and utility over using the original published data is questionable, as well. We share this information, primarily to demonstrate the messy state of the data. Many states combine their well type and well status data into a single column, while others keep them separate. Unfortunately, the most frequent well type was blank, either because states did not publish well types, or they did not publish them for all of their wells.

There are no national standards for publishing oil and gas data – a serious barrier to data transparency and the most important takeaway from this exercise…

Wells by Location

Active oil and gas wells in 2015 by state. Except for Texas, all data were aggregated published well coordinates.

There are oil and gas wells in 35 of the 50 states (70%) in the United States, and 1,673 out of 3,144 (53%) of all county and county equivalent areas. The number of wells per state ranges from 57 in Maryland to 291,996 in Texas. There are 135 counties with a single well, while the highest count is in Kern County, California, host to 77,497 active wells.

With the exception of Texas, where the data are based on published lists of well county by county, the state and county well counts were determined by the location of the well coordinates. Because of this, any errors in the original well’s location data could lead to mistakes in the state and county summary files. Any wells that are offshore are not included, either. Altogether, there are about 6,000 wells (0.4%) are missing from the state and county files.

Wells by Operator

There are a staggering number of oil and gas operators in the United States. In a recent project with the National Resources Defense Council, we looked at violations across the few states that publish such data, and only for the 68 operators that were identified previously as having the largest lease acreage nationwide. Even for this task, we had to follow a spreadsheet of which companies were subsidiaries of others, and sometimes the inclusion of an entity like “Williams” on the list came down to a judgement call as to whether we had the correct company or not.

No such effort was undertaken for this analysis. So in Pennsylvania, wells drilled by the operator Exco Resources PA, Inc. are not included with those drilled by Exco Resources PA, Llc., even though they are presumably the same entity. It just isn’t feasible to systematically go through thousands of operators to determine which operators are owned by whom, so we left the data as is. Results, therefore, should be taken with a brine truck’s worth of salt.

Top 10 wells by operator in the US, excluding Texas. Unknown operators are highlighted in red.

Texas does publish wells by operator, but as with so much of their data, it’s just not worth the effort that it takes to process it. First, they process it into thirteen different files, then publish it in PDF format, requiring special software to convert the data to spreadsheet format. Suffice to say, there are thousands of operators of active oil and gas wells in the Lone Star State.

Not counting Texas, there are 39,693 different operators listed in the United States. However, many of those listed are some version of “we don’t know whose well this is.” Sorting the operators by the number of wells that they are listed as having, we see four of the top ten operators are in fact unknown, including the top three positions.

Summary

The state of oil and gas data in the United States is clearly in shambles. As long as there are no national standards for data transparency, we can expect this trend to continue. The data that we looked for in this file is what we consider to be bare bones: well name, well type, well status, slant (directional, vertical, or horizontal), operator, and location. In none of these categories can we say that we have a satisfactory sense of what is going on nationally.

Click on the above button to download the three sets of data we used to make the dynamic map (once you are zoomed in to a state level). The full dataset was broken into three parts due to the large file sizes.

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2015/08/2015Update-Feature.jpg400900Matt Kelso, BAhttps://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngMatt Kelso, BA2015-08-03 14:19:532020-07-21 10:30:051.7 Million Wells in the U.S. – A 2015 Update

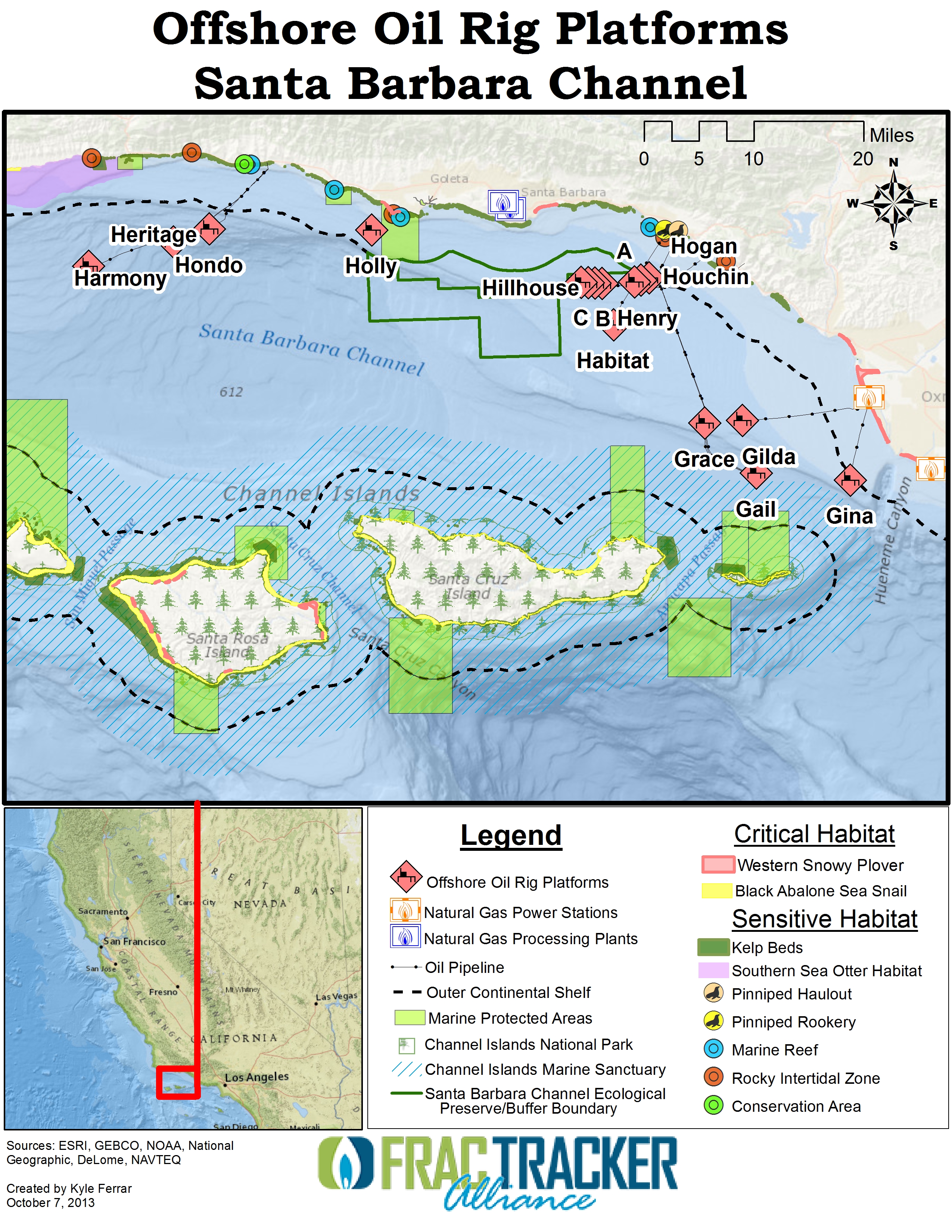

On May 19, 2015, just 20 miles north of Santa Barbara, a heavily corroded section of pipeline ruptured spilling upwards of 101,000 gallons. The pipeline was operated by Plains All American LLC, based out of Houston Texas, and was used to move crude oil from offshore rigs to inland refineries. The spill occurred on a section of pipe running parallel to the coastline at a distance of only a tenth of a mile to the ocean. As a result, the ruptured oil traveled through a drainage culvert and onto the beach where 21,000 gallons spilled into the ocean. The oil spread into a slick that covered 4 miles of coastline, and has since spread to southern California beaches more than 100 miles to the south. Santa Barbara county officials immediately closed two beaches, Refugio and El Capitan, and southern California beaches were also closed June 3rd through June 5th. Commercial fishing has been prohibited near the spill, and nearly 300 dead marine mammals and birds have been found, as well as dead cephalopods (octopi).1

Mapping the Impacts

Santa Barbara 2015 Oil Spill at Refugio Beach. To view the legend and map full screen, click here.

The map above shows details of the oil spill, including the location on the coastline, the extent that the spill traveled south, and the Exxon offshore platforms forced to suspend operations due to their inability to transport crude to onshore refineries.

The dynamic map also shows the wildlife habitats that are impacted by this oil spill, putting these species at risk. This area of Central California coastline is incredibly unique. The Santa Barbara Channel Islands are formed and molded as colder northern swells meet warmer southern swells, generating many temperature gradients and microhabitats able to support an incredible amount of biodiversity. Many species are endemic to only this region of the California coastline, and therefore are very sensitive to the impacts of pollution. In addition to the many bird species, including the endangered Western Snow Plover and Golden Eagle, this area of coastline is home to a number of whale and porpoise species, and, as seen in the map, the Leatherback Sea Turtle and the Black Abolone Sea Snail, both threatened.

Figure 1. Offshore Drilling Near Santa Barbara from 2013

For California’s harbor seal populations, this kill event reinforces existing environmental pressures that have been shrinking the seal and sea lion (pinniped) communities, increasing the threat of shark attacks on humans. For the potential impact that this could have on California’s sensitive sea otter population, see FracTracker’s recent story on the West Coast Sea Otter.

In 2013, The FracTracker Alliance collaborated with the Environmental Defense Center on the report Dirty Water: Fracking Offshore California. The report showed that much of the offshore oil is extracted by hydraulic fracturing (Fig 1.), and outlined the environmental impacts that would result from a spill of this magnitude.

Clean Up Efforts

Workers are currently cleaning the spill by hand using buckets and shovels. These old fashioned techniques may be painstaking, but they are the least invasive and they are necessary to ensure that there is not additional damage to the sensitive ecosystems. Even scraping the coastline with wire brushes and putty knives cannot remove the stain of oil that has been absorbed by porous rocks. The oil will only wear away with time as it is diluted back into the ocean. Costs of the clean-up response alone have already reached $92 million, which is being paid by Texas-based Plains All American Pipeline. There have not been any reports yet on the financial impacts to the recreational and fishing industries.2

Prevention Opportunities

By comparison, the Santa Barbara oil spill in 1969 was estimated at 200 million gallons. After over 45 years, nearly a half decade, one would think that advancements in pipeline engineering and technology would prevent these types of accidents. Plains All American, the pipeline operator states that their pressure monitors can detect leaks the size of pinholes. Why, then, did the ruptured pipe continue to spill crude for three hours after the public was notified of the incident?

This section of pipeline (falsely reported by the media to be abandoned) was built in 1987. At capacity the pipeline could transport 50,400 gallons of oil per hour, but during the time of the spill the pipeline was running under capacity. Pipeline inspections had occurred in 2012 and in April of 2014, just weeks prior. The Pipeline and Hazardous Material Safety Administration said testing conducted in May had identified extensive corrosion of the pipeline that required maintenance. It is possible that this incident is an isolated case of mismanagement, but the data tell a different story as this is not an isolated event.

Plains released a statement that a spill of this magnitude was “highly unlikely,” although this section of the pipeline has experienced multiple other spills, the largest of which being 1,200 gallons. Just a year prior, May 2014, the same company, Plains, was responsible for a 19,000 gallon spill of crude in Atwater Village in Los Angeles County. According to a joint hearing of two legislative committees, the operators, Plains did not meet state guidelines for reporting the spill. According to the county, the operator should have been able to shut down the pipeline much faster.3 It is not clear how long the pipeline was actually leaking.

NASA Spill Visualizations

As a result of the spill and to assist with the clean-up and recovery, NASA’s Jet Propulsion Laboratory (JPL) in Pasadena, CA has developed new technology to track the oil slick and locate contamination of beaches along the coastline. The JPL deployed a De Havilland Twin Otter aircraft carrying a unique airborne instrument developed to study the spill and test the ability of imaging spectroscopy to map tar on area beaches. What this means is that from aircraft special cameras can take pictures of the beach. Based on the nature of the light waves reflecting off the beach in the pictures, tar balls and oil contamination can be identified. Clean-up crews can then be dispatched to these areas. On their website, NASA states “The work is advancing our nation’s ability to respond to future oil spills.”4 A picture generated using this technology, and showing oil contamination in water and on the beach, is shown below.

This article was originally posted on 10 July 2015, and then updated on 22 January 2016 and 16 February 2016.

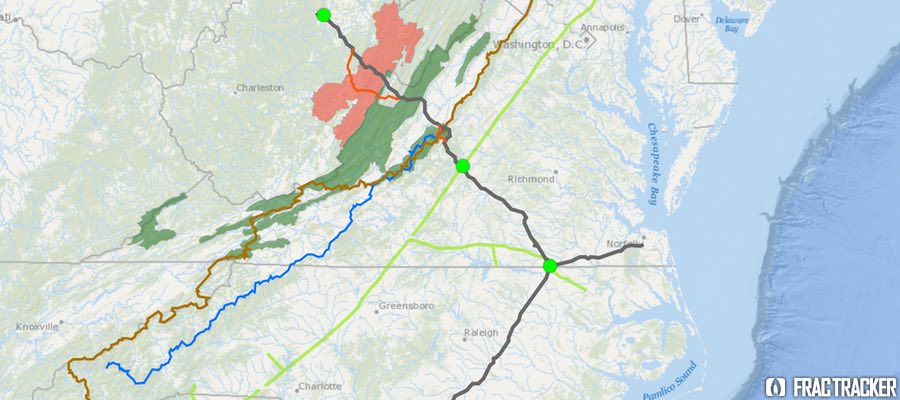

Proposed Pipeline to Funnel Marcellus Gas South

In early fall 2014, Dominion Energy proposed a $5 billion pipeline project, designed provide “clean-burning gas supplies to growing markets in Virginia and North Carolina.” Originally named the “Southeast Reliability Project,” the proposed pipeline would have a 42-inch diameter in West Virginia and Virginia. It would narrow to 36 inches in North Carolina, and narrow again to 20 inches in the portion that would extend to the coast at Hampton Roads. Moving 1.5 billion cubic feet per day of gas, with a maximum allowable operating pressure of 1440 psig (pounds per square inch gage), the pipeline would be designed for larger customers (such as manufacturers and power generators) or local gas distributors supplying homes and businesses to tap into the pipeline along the route, making the pipeline a prime mover for development along its path.

The project was renamed the Atlantic Coast Pipeline (ACP) when a coalition of four major US energy companies—Dominion (45% ownership), Duke Energy (40%), Piedmont Natural Gas (15%), and AGL Resources (5%)— proposed a joint venture in building and co-owning the pipeline. Since then, over 100 energy companies, economic developers, labor unions, manufacturers, and civic groups have joined the new Energy Sure Coalition, supporting the ACP. The coalition asserts that the pipeline is essential because the demand for fuel for power generation is predicted more than triple over the next 20 years. Their website touts the pipeline as a “Path to Cleaner Energy,” and suggests that the project will generate significant tax revenue for Virginia, North Carolina, and West Virginia.

Lew Ebert, president of the North Carolina Chamber of Commerce, optimistically commented:

Having the ability to bring low-cost, affordable, predictable energy to a part of the state that’s desperately in need of it is a big deal. The opportunity to bring a new kind of energy to a part of the state that has really struggled over decades is a real economic plus.

Unlike older pipelines, which were designed to move oil and gas from the Gulf Coast refineries northward to meet energy demands there, the Atlantic Coast Pipeline would tap the Marcellus Shale Formation in Ohio, West Virginia and Pennsylvania and send it south to fuel power generation stations and residential customers. Dominion characterizes the need for natural gas in these parts of the country as “urgent,” and that there is no better supplier than these “four homegrown companies” that have been economic forces in the state for many years.

In addition to the 550 miles of proposed pipeline for this project, three compressor stations are also planned. One would be at the beginning of the pipeline in West Virginia, a second midway in County Virginia, and the third near the Virginia-North Carolina state line. The compressor stations are located along the proposed pipeline, adjacent to the Transcontinental Pipeline, which stretches more than 1,800 miles from Pennsylvania and the New York City Area to locations along the Gulf of Mexico, as far south as Brownsville, TX.

In mid-May 2015, in order to avoid requesting Congressional approval to locate the pipeline over National Park Service lands, Dominion proposed rerouting two sections of the pipeline, combining the impact zones on both the Blue Ridge Parkway and the Appalachian Trail into a single location along the border of Nelson and Augusta Counties, VA. National Forest Service land does not require as strict of approvals as would construction on National Park Service lands. Dominion noted that over 80% of the pipeline route has already been surveyed.

Opposition to the Pipeline on Many Fronts

The path of the proposed pipeline crosses topography that is well known for its karst geology feature—underground caverns that are continuous with groundwater supplies. Environmentalists have been vocal in their concern that were part of the pipeline to rupture, groundwater contamination, along with impacts to wildlife could be extensive. In Nelson County, VA, alone, 70% of the property owners in the path of the proposed pipeline have refused Dominion access for survey, asserting that Dominion has been unresponsive to their concerns about environmental and cultural impacts of the project.

On the grassroots front, 38 conservation and environmental groups in Virginia and West Virginia have combined efforts to oppose the ACP. The group, called the Allegany-Blue Ridge Alliance (ABRA), cites among its primary concerns the ecologically-sensitive habitats the proposed pipeline would cross, including over 49.5 miles of the George Washington and Monongahela State Forests in Virginia and West Virginia. The “alternative” version of the pipeline route would traverse 62.7 miles of the same State Forests. Scenic routes, including the Blue Ridge Parkway and the Appalachian Scenic Trail would also be impacted. In addition, it would pose negative impacts on many rural communities but not offset these impacts with any longer-term economic benefits. ABRA is urging for a programmatic environmental impact statement (PEIS) to assess the full impact of the pipeline, and also evaluate “all reasonable, less damaging” alternatives. Importantly, ABRA is urging for a review that explores the cumulative impacts off all pipeline infrastructure projects in the area, especially in light of the increasing availability of clean energy alternatives.

Environmental and political opposition to the pipeline has been strong, especially in western Virginia. Friends of Nelson, based in Nelson County, VA, has taken issue with the impacts posed by the 150-foot-wide easement necessary for the pipeline, as well as the shortage of Department of Environmental Quality staff that would be necessary to oversee a project of this magnitude.

Do gas reserves justify this project?

Dominion, an informational flyer, put forward an interesting argument about why gas pipelines are a more environmentally desirable alternative to green energy:

If all of the natural gas that would flow through the Atlantic Coast Pipeline is used to generate electricity, the 1.5 billion cubic feet per day (bcf/d) would yield approximately 190,500 megawatt-hours per day (mwh/d) of electricity. The pipeline, once operational, would affect approximately 4,600 acres of land. To generate that much electricity with wind turbines, utilities would need approximately 46,500 wind turbines on approximately 476,000 acres of land. To generate that much electricity with solar farms, utilities would need approximately 1.7 million acres of land dedicated to solar power generation.

Nonetheless, researchers, as well as environmental groups, have questioned whether the logic is sound, given production in both the Marcellus and Utica Formations is dropping off in recent assessments.

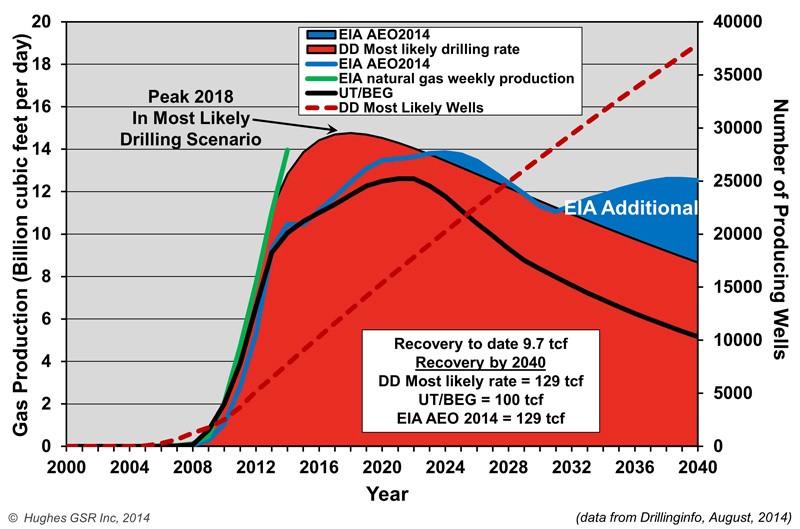

Both Nature, in their article Natural Gas: The Fracking Fallacy, and Post Carbon Institute, in their paper Drilling Deeper, took a critical look at several of the current production scenarios for the Marcellus Shale offered by EIA and University of Texas Bureau of Economic Geology (UT/BEG). All estimates show a decline in production over current levels. The University of Texas report, authored by petroleum geologists, is considerably less optimistic than what has been suggested by the Energy Information Administration (EIA), and imply that the oil and gas bubble is likely to soon burst.

Natural Gas Production Projections for Marcellus Shale

David Hughes, author of the Drilling Deeper report, summarized some of his findings on Marcellus productivity:

Field decline averages 32% per year without drilling, requiring about 1,000 wells per year in Pennsylvania and West Virginia to offset.

Core counties occupy a relatively small proportion of the total play area and are the current focus of drilling.

Average well productivity in most counties is increasing as operators apply better technology and focus drilling on sweet spots.

Production in the “most likely” drilling rate case is likely to peak by 2018 at 25% above the levels in mid-2014 and will cumulatively produce the quantity that the Energy Information Administration (EIA) projected through 2040. However, production levels will be higher in early years and lower in later years than the EIA projected, which is critical information for ongoing infrastructure development plans.

Five out of more than 70 counties account for two-thirds of production. Eighty-five percent of production is from Pennsylvania, 15% from West Virginia and very small amounts from Ohio and New York. (The EIA has published maps of the depth, thickness and distribution of the Marcellus shale, which are helpful in understanding the variability of the play.)

The increase in well productivity over time reported in Drilling Deeper has now peaked in several of the top counties and is declining. This means that better technology is no longer increasing average well productivity in these counties, a result of either drilling in poorer locations and/or well interference resulting in one well cannibalizing another well’s recoverable gas. This declining well productivity is significant, yet expected, as top counties become saturated with wells and will degrade the economics which have allowed operators to sell into Appalachian gas hubs at a significant discount to Henry hub gas prices.

The backlog of wells awaiting completion (aka “fracklog”) was reduced from nearly a thousand wells in early 2012 to very few in mid-2013, but has increased to more than 500 in late 2014. This means there is a cushion of wells waiting on completion which can maintain or increase overall play production as they are connected, even if the rig count drops further.

Current drilling rates are sufficient to keep Marcellus production growing on track for its projected 2018 peak (“most likely” case in Drilling Deeper).

Post Carbon Institute estimates that Marcellus predictions overstate actual production by 45-142%. Regardless of the model we consider, production starts to drop off within a year or two after the proposed Atlantic Coast Pipeline would go into operation. This downward trend leads to some serious questions about whether moving ahead with the assumption of three-fold demand for gas along the Carolina coast should prompt some larger planning questions, and whether the availability of recoverable Marcellus gas over the next twenty years, as well as the environmental impacts of the Atlantic Coast Pipeline, justify its construction.

Next steps

The Federal Energy Regulatory Commission, FERC, will make a final approval on the pipeline route later in the summer of 2015, with a final decision on the pipeline construction itself expected by fall 2016.

UPDATE #1: On January 19, 2016, the Richmond Times-Dispatch reported that the United States Forest Service had rejected the pipeline, due to the impact its route would have on habitats of sensitive animal species living in the two National Forests it is proposed to traverse.

UPDATE #2: On February 12, 2016, Dominion Pipeline Company released a new map showing an alternative route to the one recently rejected by the United States Forest Service a month earlier. Stridently condemned by the Dominion Pipeline Monitoring Coalition as an “irresponsible undertaking”, the new route would not only cross terrain the Dominion had previously rejected as too hazardous for pipeline construction, it would–in avoiding a path through Cheat and Shenandoah Mountains–impact terrain known for its ecologically sensitive karst topography, and pose grave risks to water quality and soil erosion.

Waste disposal is an issue that causes quite a bit of consternation even amongst those that are pro-fracking. The disposal of fracking waste into injection wells has exposed many “hidden geologic faults” across the US as a result of induced seismicity, and it has been linked recently with increases in earthquake activity in states like Arkansas, Kansas, Texas, and Ohio. Here in OH there is growing evidence – from Ashtabula to Washington counties – that injection well volumes and quarterly rates of change are related to upticks in seismic activity.

Origins of Fracking Waste

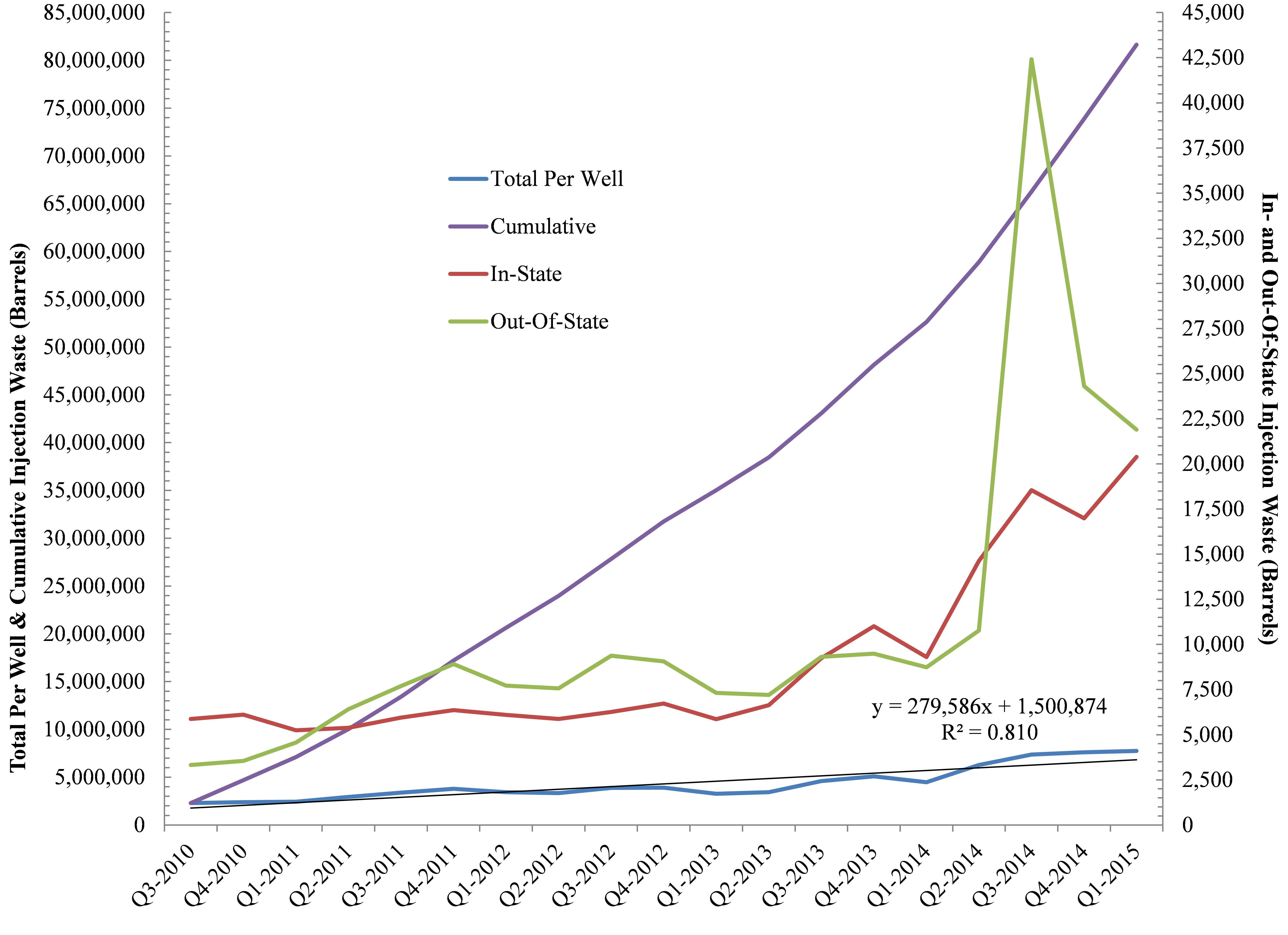

Furthermore, as part of this analysis we wanted to understand the ratio of Ohio’s Class II waste that has come from within Ohio and the proportion of waste originating from neighboring states such as West Virginia and Pennsylvania. Out of 960 Utica laterals and 245+ Class II wells, the results speak to the fact that a preponderance of the waste is coming from outside Ohio with out-of-state shale development accounting for ≈90% of the state’s hydraulic fracturing brine stream to-date. However, more recently the tables have turned with in-state waste increasing by 4,202 barrels per quarter per well (BPQPW). Out-of-state waste is only increasing by 1,112 BPQPW. Such a change stands in sharp contrast to our August 2013 analysis that spoke to 471 and 723 BPQPW rates of change for In- and Out-Of-State, respectively.

Brine Production

Figure 1. Ohio Class II Injection Well trends In- and Out-Of-State, Cumulatively, and on Per Well basis (n = 248).

For every gallon of freshwater used in the fracking process here in Ohio the industry is generating .03 gallons of brine (On average, Ohio’s 758 Utica wells use 6.88 million gallons of freshwater and produce 225,883 gallons of brine per well).

Back in August of 2013 the rate at which brine volumes were increasing was approaching 150,000 BPQPW (Learn more, Fig 5), however, that number has nearly doubled to +279,586 BPQPW (Note: 1 barrel of brine equals 32-42 gallons). Furthermore, Ohio’s Class II Injection wells are averaging 37,301 BPQPW (1.6 MGs) per quarter over the last year vs. 12,926 barrels BPQPW – all of this between the initiation of frack waste injection in 2010 and our last analysis up to and including Q2-2013. Finally, between Q3-2010 and Q1-2015 the exponential increase in injection activity has resulted in a total of 81.7 million barrels (2.6-3.4 billion gallons) of waste disposed of here in Ohio. From a dollars and cents perspective this waste has generated $2.5 million in revenue for the state or 00.01% of the average state budget (Note: 2.5% of ODNR’s annual budget).

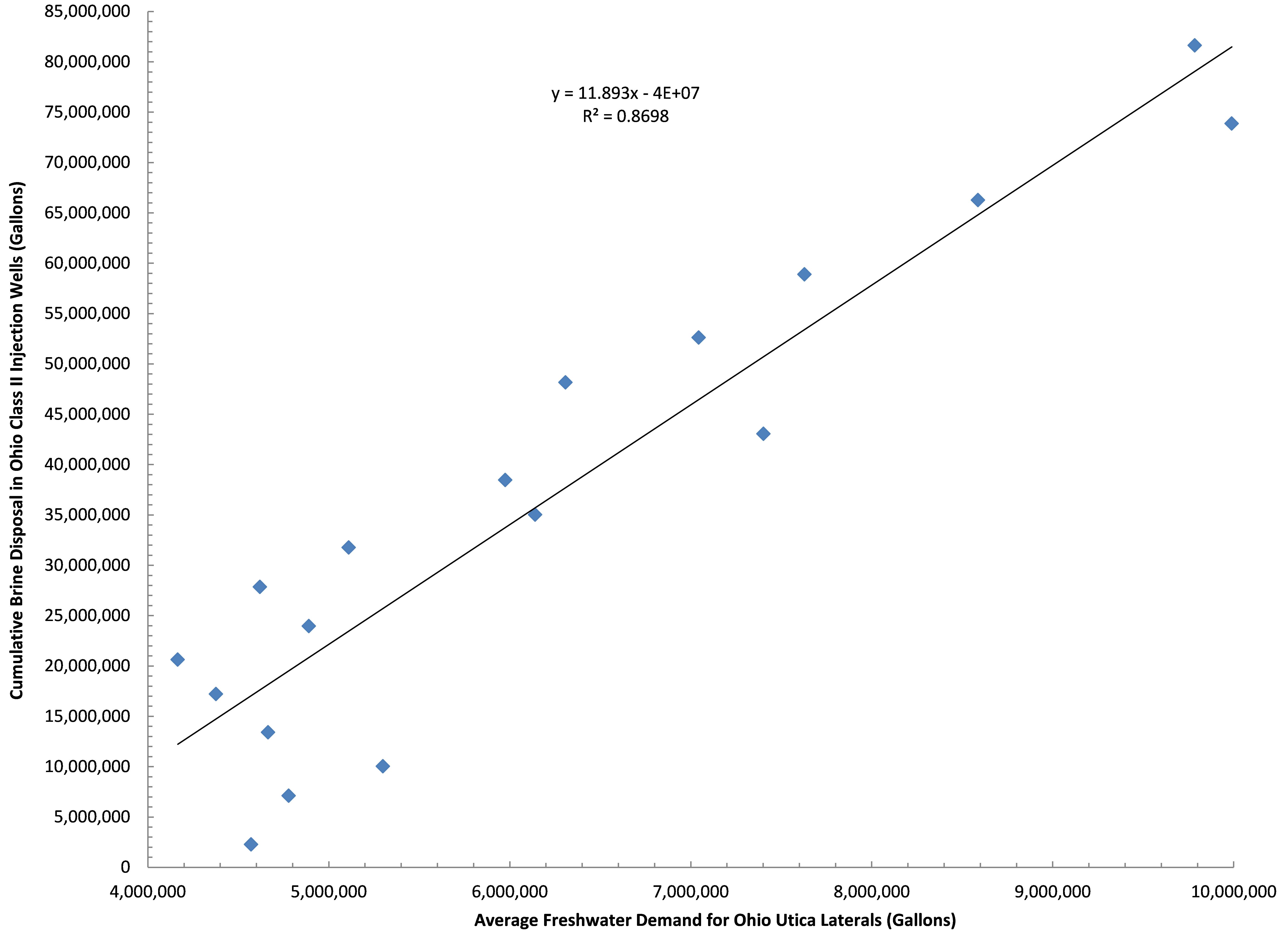

Freshwater Demand Growing

Figure 2. Ohio Class II Injection Well disposal as a function of freshwater demand by the shale industry in Ohio between Q3-2010 and Q1-2015.

The relationship between brine (waste) produced and freshwater needed by the hydraulic fracturing industry is an interesting one; average freshwater demand during the fracking process accounts for 87% of the trend in brine disposal here in Ohio (Fig. 2). The more water used, the more waste produced. Additionally, the demand for OH freshwater is growing to the tune of 405-410,000 gallons PQPW, which means brine production is growing by roughly 12,000 gallons PQPW. This says nothing for the 450,000 gallons of freshwater PQPW increase in West Virginia and their likely demand for injection sites that can accommodate their 13,500 gallons PQPW increase.

Where will all this waste go? I’ll give you two guesses, and the first one doesn’t count given that in the last month the ODNR has issued 7 new injection well permits with 9 pending according to the Center For Health and Environmental Justice’s Teresa Mills.

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2015/07/Injection-Feature.jpg400900Ted Auch, PhDhttps://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngTed Auch, PhD2015-07-09 14:54:002020-07-21 10:30:05OH Class II Injection Wells – Waste Disposal and Industry Water Demand