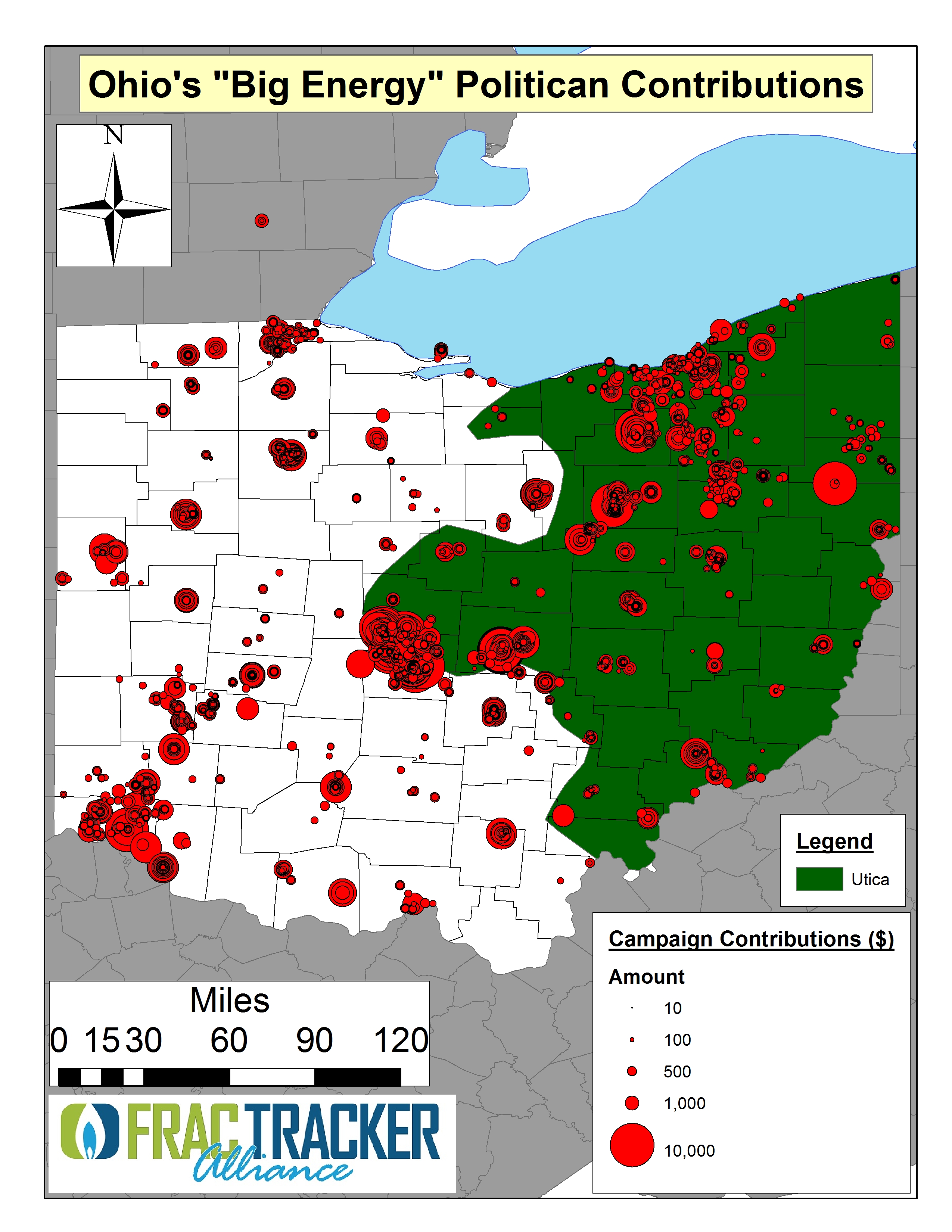

Land-Use Change, the Utica Shale, and the Loss of Ecosystem Services

By Ted Auch, PhD – Ohio Program Coordinator, FracTracker Alliance

In Ohio, Utica Well pads range in size from 5-15 acres. (Estimates for pipeline and retention ponds are unavailable.) That figure gives us the chance to estimate how hydraulic fracturing influenced changes to land-use, ecosystem services, plant productivity, and soil carbon loss.

Working with Caleb Gallemore and his Ohio State University GIS class, we created a data set that estimated the percent cover for each well pad prior to drilling using the USGS and Department of Interior’s 2006 National Land Cover Database (NLCD, 2006) [1].

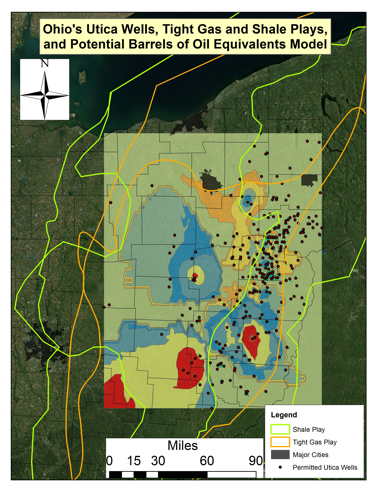

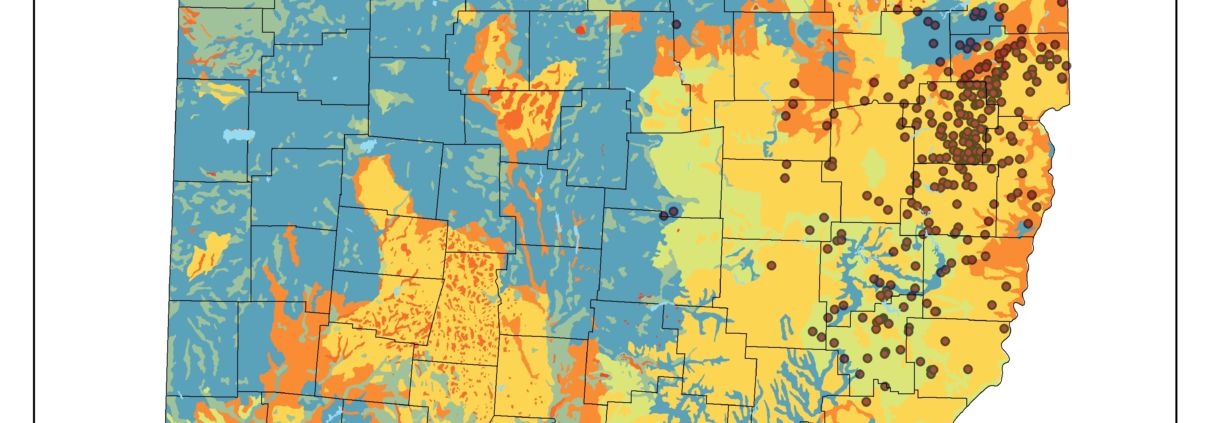

Figure 1. Ohio’s original vegetation cover and Utica Well permits as of April 30, 2013

Accordingly, the state was and is dominated by:

- mixed oak (from 12,038 mi2 pre-settlement to 7,911 mi2 today) to the east and

- maple-beech-birch (from 13,917 mi2 pre-settlement to 2,521 mi2 today) to the west stretching into the southeast and northwest corner of Ohio.

During pre-settlement times additional dominant forest types included:

- 5,181 mi2 of mixed mesophytic and hemlock-beech-chestnut-red oak forests, and

- 3,401 square miles of oak-sugar maple (Figure 1).

Since industrialization:

- The faster growing elm-ash-cottonwood has arisen as a sub-dominant forest type currently comprising 1,237 mi2.

- Additional sub-dominant forest types comprising 100-140 mi2 of Ohio’s land area include aspen-birch (134 mi2), white-red-jack pine (124 mi2), and loblolly-shortleaf pine (108 mi2).

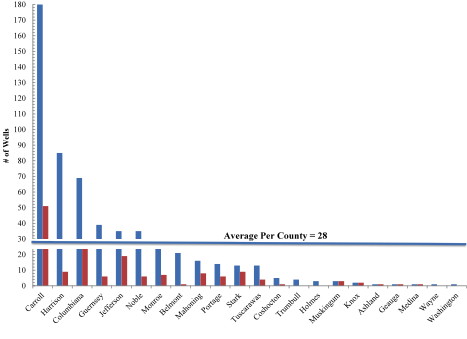

Our results suggest the average amount of deciduous forest [2] disturbed – as a percent of total well pad area – by well pad establishment is 9.8 ± 5.5% per well pad with a range of 4.7% in Stark and Holmes Counties and a high of 24% in Monroe County (Figure 2). With respect to pasture and crop displacement the average is 11.7 and 10.7% per well pad, respectively, with significantly higher between-county variability for crop cover (±5.5% Vs ±3.6%).

as a proxy for previous land-use.")

Figure 2. Percent Cover across Ohio’s 269 Utica Well Pads assuming an average area of 7.75 acres and the National Land Cover Database 2006 (NLCD 2006) as a proxy for previous land-use. – Click to enlarge

Converting this data into ecosystem services requires certain assumptions about plant growth, soil organic matter content, and soil compaction utilizing Natural Resource Conservation Service (NRCS) soil data to model the latter two and established peer-reviewed estimates for plant pattern and process (Follett, Kimble, & Lal, 2000; Lobell et al., 2002; Valentine et al., 2012). The basics of this analysis – assuming subsurface soils are 25% more compact and contain 45% less organic matter than the surface 12-13 inches (Needelman et al., 1999) – demonstrated that well pad establishment has displaced approximately 28,205 tons of surface and 78,348 tons of subsurface soil carbon [3] for a total of 106,554 tons of carbon equivalent to 389,986 tons of CO2.

Additionally, the displacement and/or removal of vegetation – assuming the average Ohio forest is 40-80 years old [4] – has resulted in the annual loss of 1,050, 6,516, and 9,461 tons of crop, pasture, and forest carbon production, respectively. This is equal to 17,027 tons of carbon or 62,319 tons of CO2, which when added to the aforementioned soil loss is equivalent to the CO2 footprint of 25,198 Ohioans [5].

Over the life of these three ecosystem types, well pad establishment displaces 1,021,619 tons of carbon. This equates to 3.74 million tons of CO2 or 230,034 Ohioans, which is roughly 9,000 less people than reside in Akron and Warren combined. Another way way to frame this figure is that it would be equivalent to the eightieth largest US city between Henderson, NV and Scottsdale, AZ.

| At CO2’s current valuation this Ohio Utica well pad “carbon displacement” is roughly $18.71 million. However, if we assume this is at the lower end of reasonable CO2 estimates and that a range of $10-75 dollars is more indicative of carbon’s price, then we estimate the value of well pad displaced carbon is more like $41.29-309.68 million. |

The true value of Utica well pad carbon displacement is somewhere in this range and entirely dependent on your belief in the feasibility of valuing CO2 emissions. However, these estimates do point to some of the externalities associated with Utica Shale development currently ignored by industry lobbyists and political advocates. There is far more work to be done as it relates to understanding well pads’ influence on ecosystem services, crop productivity, and local hydrology; this is simply an attempt to begin quantifying such effects.

References

Follett, R F, Kimble, J M, & Lal, R. (2000). The Potential of U.S. Grazing Lands to Sequester Carbon and Mitigate the Greenhouse Effect. Boca Raton, FL: CRC Press LLC.

Fry, J, Xian, G, Jin, S, Dewitz, J, Homer, C, Yang, L, . . . Wickham, J. (2011). Completion of the 2006 National Land Cover Database for the Conterminous United States. PE&RS, 77(9), 858-864.

Lobell, D B, Hicke, J A, Asner, G P, Field, C B, Tucker, C J, & Los, S O. (2002). Satellite estimates of productivity and light use efficiency in United States agriculture, 1982-98. Global Change Biology, 8(8), 722-735.

Needelman, B A, Wander, M M, Bollero, G A, Boast, C W, Sims, G K, & Bullock, D G. (1999). Interaction of Tillage and Soil Texture Biologically Active Soil Organic Matter in Illinois. Soil Science Society of America Journal, 63(5), 1326-1334.

Valentine, J, Clifton-Brown, J, Hastings, A, Robson, P, Allison, G, & Smith, P. (2012). Food vs. Fuel: The use of land for lignocellulosic next generation energy crops to minimize competition with primary food production. Global Change Biology Bioenergy, 4(1), 1-19.

Footnotes

[1] The NLCD estimates land cover using sixteen classes at a 98 foot spatial resolution applied to 2006 Landsat satellite data or 4-5 years prior to the first Ohio Utica permit in September, 2010 (Fry et al., 2011)

[2] Primary tree species include red and sugar maple, red and white oak, white ash, black cherry, American beech, hickory, and tulip poplar according to the most recent USFS Forest Inventory Analysis “Ohio Forests 2006”.

[3] Along with roughly 6,536 tons of soil nitrogen assuming an Ohio soil Carbon-To-Nitrogen ratio of 14.6.

[4] Utilizing the USFS’s Forest Inventory and Analysis EVALIDator Version 1.5.1.04 tool we determined that 62% of Ohio’s oak-hickory, maple-beech-birch, elm-ash-cottonwood, and oak-pine forest types, which account for 94% of the state’s forest area, are 40-80 years old.

[5] Assuming 17.3-18.6 tons of CO2 per capita based on Oak Ridge National Laboratory’s Carbon Dioxide Information Analysis Center as cited by the World Bank.