By Isabelle Weber, FracTracker Alliance Spring 2019 Intern

Feature photo of oil and gas drilling in North Dakota, and is by by Nick Lund, NPCA, 2014

Although there are some federal regulations in place to protect the environment indirectly from fracking in the United States, the regulations that try to keep fracking in check are largely implemented at the state governing level. This has led to a patchwork of regulations that differ in strictness from state to state. This leads to the concern that there will be a race to the bottom where states lower the strictness of their regulations in order to draw in more fracking. While it might be tempting to welcome an industry that often creates a temporary economic spike, the costs of mitigating the environmental damage from fracking far out-weighs the profit gained. Germany, Scotland, and France are examples of countries that have taken more appropriate regulatory measures to protect their populations from the risks involved in unconventional oil and gas development.

The Shortfalls of State by State Regulations

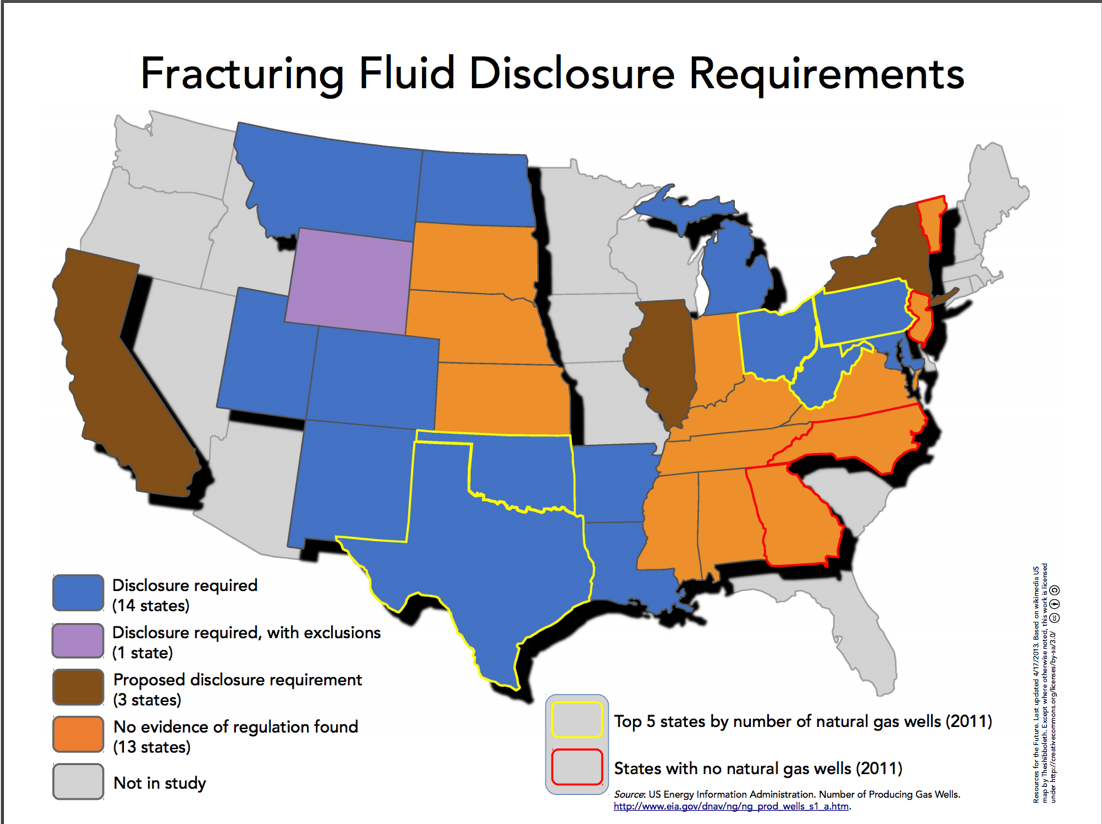

For a detailed overview of how fracking regulation differs between states, check out the Resources for the Future report, The State of State Shale Gas Regulation, which analyzes 25 regulatory elements and how they differ between states. Two of their maps that attest to this vast difference in regulation are the “Fracturing Fluid Disclosure Requirements” map as well as the “Venting Regulations” map.

The “Fracturing Fluid Disclosure Requirements” map shows regulatory differences between states regarding whether or not the chemical mixture used to break up rock formations must be made known to the public. “Disclosure” means that the chemical mixture is made known to the public and “No Regulation” means that there is nothing that obligates companies to share this information, which usually implies this information is not available.

Fig 1. Map of fracking fluid disclosure requirements by state, from Resources for the Future’s report, “The State of State Shale Gas Regulation.” Original data from US Energy Information Administration.

Note from the editor: There are several exemptions that allow states to limit the scope of reporting chemicals used in underground fluid injection for fracking. For example, all states that require chemical disclosure are entitled to exemptions for chemicals that are considered trade secrets.

Concealing the identity of chemicals increases the risk of harm from chemical exposure for people and the environment. Emergency first responders are especially at risk, as they may have to act quickly to put out a fracking-induced fire without knowing the safety measures necessary to avoid exposure to dangerous chemicals. The population at large is at risk of exposure though several pathways such as leaks, spills, and air emissions. Partnership for Policy Integrity, along with data analysis by FracTracker, investigated the implications of keeping the identity of certain fracking chemicals secret in two states, Ohio and Pennsylvania. These reports point to evidence that exposure to concealed fracking chemicals could have serious health effects including blood toxicity, developmental toxicity, liver toxicity and neurotoxicity.

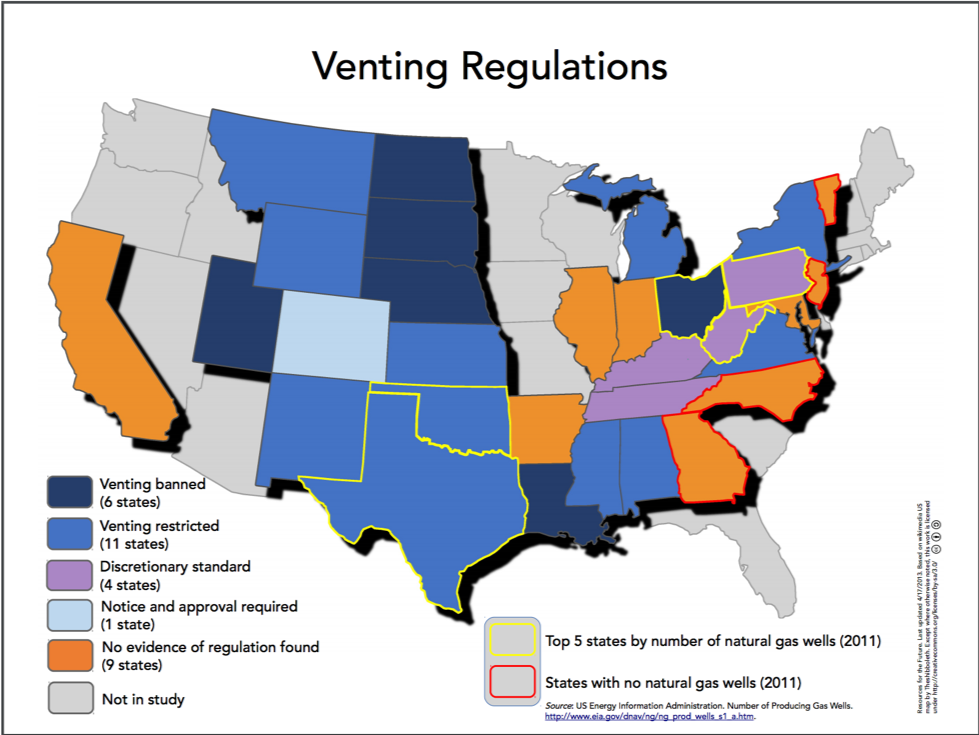

The second map, “Venting Regulations,” shows which states have regulations that limit or ban venting and which do not. Venting is the direct release of methane from the well site into the atmosphere. Methane has 30 times the green-house gas effect as carbon dioxide. Given methane’s severe impact on the environment, no venting whatsoever should be allowed at well sites.

Fig 2. Map of fracking venting regulations by state, from Resources for the Future’s report, “The State of State Shale Gas Regulation.” Original data from US Energy Information Administration.

Having overarching federal regulatory infrastructure to regulate fracking would help to avoid risks such as toxic chemical exposure and accelerated climate change. Although leaving regulation development to states allows for more specialized laws, there are certain aspects of environmental protection that apply to every area in the United States and are necessary as standard protection against the effects of fracking.

How do other countries regulate fracking?

Stronger federal regulation of fracking has worked well in the past and can be seen in several other countries.

Germany

In 2017, Germany passed new legislation that largely banned unconventional hydraulic fracking. The ban on unconventional fracking excludes four experimental wells per state that will be commissioned by the German government to an independent expert commission to identify knowledge gaps and risks with regards to fracking. Conventional fracking also received tighter regulations including a ban on fracking near drinking water sources. In 2021, the ban will be reevaluated, taking into account research results, public perception, long term damage to residents and the environment, and technological advances. This is a perfect example of how a country can use overarching federal regulation to make informed decisions about industry action.

Scotland

In 2015, Scotland placed a moratorium into effect that halted all fracking in the country. Since 2017, the government has held that the moratorium will stand indefinitely as an effective ban on fracking in the country, but the country is still working on the legislature that will officially ban fracking. Meanwhile, the Scottish government conducted one of the most far-reaching investigations into unconventional oil and gas development, which included a four-month public consultation period. This public consultation garnered 65,000 responses, 65% of which were from former coal mining communities targeted by the fracking industry. Of those responses, 99% of responses opposed fracking.

The Scottish people should be applauded for holding their federal government accountable in fulfilling its responsibility to protect its people and its environment against the effects of fracking.

France

In December 2017, France passed a law that bans exploration and production of all oil and natural gas by the year 2040. This applies to mainland France as well as all French territories. Although France has limited natural gas resources, it is hoped that the ban will be contagious and spread to other countries. This is a prime example of a country making a decision to protect their environment through regulation.

Although France’s banning of fracking was largely symbolic and may not result in a considerable reduction of greenhouse gases related to natural gas exploration, the country is sending a message to the world that we need to facilitate the end of the fossil fuel era and a move toward renewables.

Back to the US, the world’s leading producer of natural gas

Federal regulation on fracking should be holding the oil and gas industry in check by requiring states to meet basic measures to protect people and the environment. States could then develop more stringent regulations as they see fit. It is important that we come to a national consensus on the environmental and health hazards of fracking, and consequently, to adopt appropriate federal regulations.

By Isabelle Weber, FracTracker Alliance Spring 2019 Intern

https://fractracker.org/wp-content/uploads/2019/10/Oil-and-gas-drilling-in-ND.-Photo-by-Nick-Lund-NPCA-2014-feature-scaled.jpg6671500Intern FracTrackerhttps://fractracker.org/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngIntern FracTracker2019-10-10 11:50:142021-04-28 11:55:45How State Regulations Hold Us back and What Other Countries are doing about Fracking

Guest blog by Natalia N. Romanzo, graduate student, Binghamton University, Binghamton, NY

Innovations in geospatial remote sensing technology developed by a research team at Binghamton University’s Geophysics and Remote Sensing Laboratory allow for improved detection of unplugged oil and gas wells. Implementing this technology would allow responsible agencies to more efficiently locate, and then plug, the 30,000+ undocumented oil and gas wells in New York State. Plugging these wells would help residents to assess risks of any wells on or near their property, improve air quality, and keep New York State on track to reaching its greenhouse gas emissions targets.

Dangers of Unplugged Orphan Oil and Gas Wells

In 2018, the United States Environmental Protection Agency (EPA) estimated that nationwide, there were 3.11 million abandoned oil and gas wells. Sixty-nine percent — or 2.15 million — of these wells are not even plugged. Many were drilled prior to the existence of state regulatory programs, subsequently abandoned by their original owners or operators over a century ago, and then left unplugged or poorly plugged. State and federal regulators are in the process of plugging these wells, but the process is slow; many are still unplugged today.

Anthropogenic methane is the cause of a quarter of today’s global warming, and the oil and gas industry is a leading source of these emissions. Every year, oil and gas companies release an estimated 75 million metric tons of methane globally, an amount of gas sufficient to provide electricity for all of Africa twice over. Unplugged wells are often high emitters contributing to this energy waste. A study of almost 140 wells in Wyoming, Colorado, Utah, and Ohio found that more than 40% of unplugged wells leak methane, compared to less than 1% of plugged wells.

Unplugged, incorrectly plugged, as well as active wells can all leak methane. Methane-leaking wells are especially problematic when their locations are undocumented or unknown. Until they are located, undocumented wells that remain unplugged can continue to emit methane into the atmosphere and into drinking water. For example, in Pennsylvania, methane was detected in water samples at average concentrations six times higher in homes less than one kilometer from oil and gas wells. The potential negative impact of unplugged orphan oil and gas wells makes this a pressing environmental concern.

Of the more than 3 million problematic oil and gas wells nationwide, over 35,000 unplugged oil and gas wells may exist in New York State alone. Unplugged or improperly plugged wells that leak methane can pose direct threats to New York State residents, especially for people living nearby to these wells. Many New York State residents are unaware that they have an unplugged well on their property, and could be at risk of potential exposure to uncontrolled releases of gas or fluids from unplugged orphan wells. In one case in Rushville, New York, two dozen unplugged wells emitted methane at explosive levels. An unplugged well in Rome, New York discharged brine to the land surface for decade at a rate of 5 gallons per minute, killing an acre of wetland vegetation. If these wells had been located and assessed, property owners would be better informed and safer.

In addition to directly harming New York State residents and contributing to climate change, unplugged orphan wells also impact New York State’s ability to reach its 2030 emissions targets. New York State recently set ambitious statewide greenhouse gas emissions targets through the Climate Leadership and Community Protection Act to lower emissions by 85% by 2050. However, New York State has only reduced emissions 8% from 1990-2015 levels. If New York State is to reach its emissions targets, it must continue and improve its efforts to locate, assess, and ultimately plug all its orphan oil and gas wells.

Inaccurate Records and Inefficient Detection Methods

The New York State Department of Environmental Conservation (DEC) is responsible for task of mitigating and preventing damage caused by oil and gas wells. Unfortunately, flaws in record keeping have made it difficult to locate undocumented wells. The DEC began record keeping of oil and gas wells in 1983 and took on regulatory authority over wells drilled in the state after 1983. There are strict rules and regulations for plugging wells drilled after 1983, and wells drilled prior to 1983 must comply with applicable regulations. Nevertheless, many older wells are still unaccounted for. In their external review in 1994, staff estimated that 61,000 wells had been developed prior to 1983. However, the agency only has records on about 30,000 of them. Because accurate records do not exist for old wells, it is difficult to monitor, and even locate, them.

Click here for a full-screen view of FracTracker Alliance’s map of all known wells in New York State (data current as of October 2018, to be updated soon).

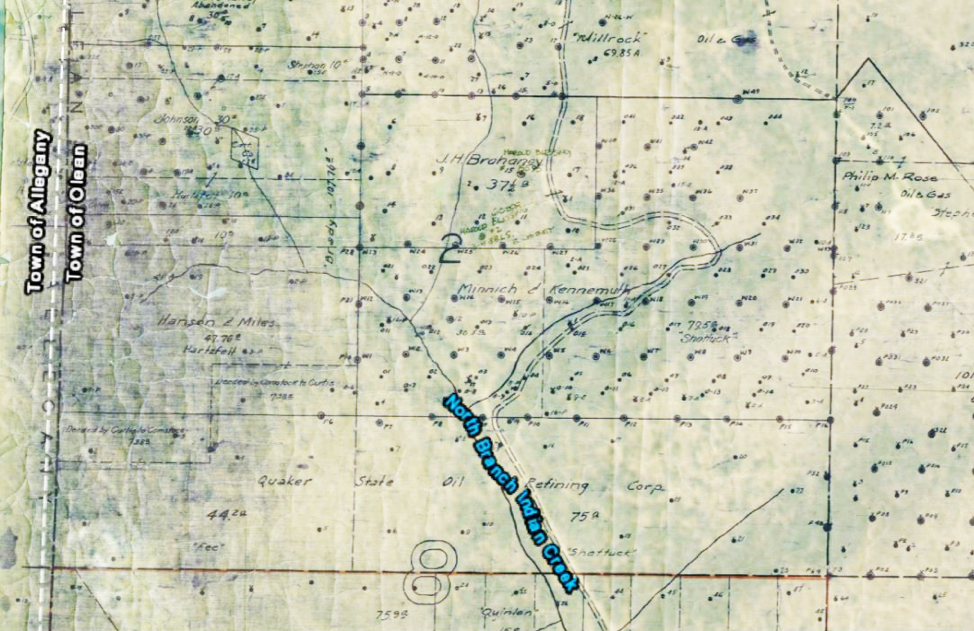

Despite inaccurate records, the DEC does try to locate, assess, and plug old wells using maps created by drilling companies in the late 1800s. A section of one such map can be seen in Figure 1. This map shows proposed oil and gas drilling sites in Cattaraugus County, New York in the late 1800s. It has been georeferenced using ArcGIS mapping software to assign present day coordinates to hand drawn features.

Figure 1. Georeferenced Lease Map, Cattaraugus County, New York

Unfortunately, these maps are not entirely reliable. Some wells may be incorrectly documented on a map as drilled when, in fact, they were merely proposed but never drilled; some wells may have been drilled but never marked on a map. Other wells may have been both marked on a map and drilled, but due to inaccurate survey technologies of the past, the location on the ground is incorrect. As a result, DEC staff are left searching on foot for wells that may or may not be there. Working with limited equipment, in dense brush, and over uneven terrain make the task of finding the abandoned wells even more problematic.

These traditional methods of detection, which include referencing lease maps and searching for wells in the field, are not only time consuming, but are also costly. Using traditional methods of well detection, between 1988 and 2009, the United States Bureau of Land Management spent $3.8 million and only successfully reclaimed 295 well sites. It is clear that on both the federal and state levels, traditional well detecting methods are expensive, cumbersome, and inefficient.

Drones Pave the Way for Oil and Gas Well Detection

Recent improvements in geospatial remote sensing technology have opened opportunities for more efficient well detection. Previously, the battery life of drones and the weight of magnetometers prevented the two technologies from being used together to locate oil and gas wells. Furthermore, because drones must be flown high enough to clear vegetative canopies, methane sensors attached to drones are too far away from the source to accurately detect the location of the well. Due to these technological barriers, the DEC and other environmental departments and agencies have had to rely on inefficient, traditional methods of well detection described above.

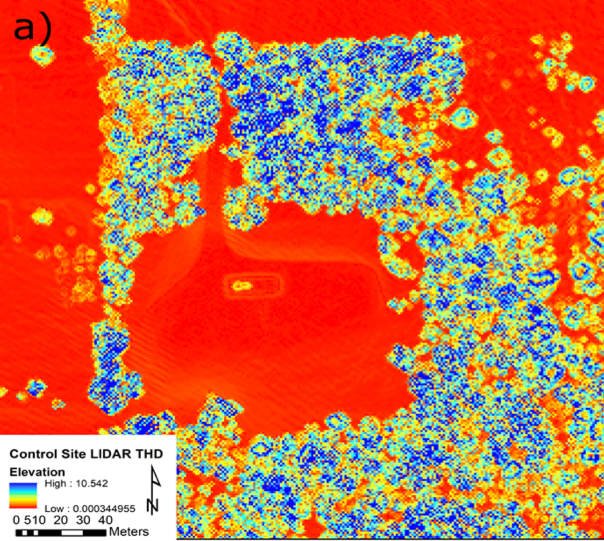

At Binghamton University’s Geophysics and Remote Sensing Laboratory, a research team headed by Professors Timothy de Smet and Alex Nikulin, along with graduate student Natalia Romanzo, and undergraduate students Samantha Wong, Judy Li, and Ethan Penner, is taking on the task of developing a more efficient method to locate oil and gas wells. The Binghamton University research team deployed drones equipped with magnetometers to demonstrate that a high-resolution, low-altitude magnetic survey can successfully locate unmarked well sites.

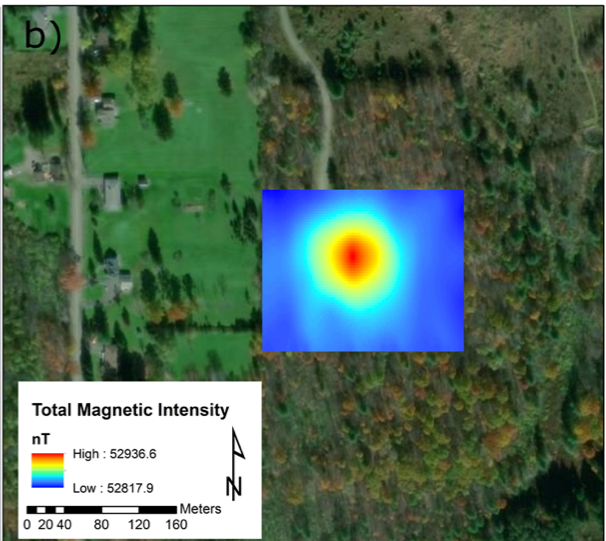

Oil and gas wells have a characteristic magnetic signal that is generated by vertical metal piping fixed in the ground, making them identifiable in a magnetic survey.

Figure 2a. Oil and Gas Well Detected at 40m AGL showing LiDAR Total Horizontal Derivative of the site.

The magnetic signal generated by a well is shown in red in Figure 2b. At 40 meters above ground level (AGL), tree canopies are cleared, while the magnetic anomaly of the well is distinguishable. This drone-based magnetometer method has shown promising results.

Figure 2b. Magnetic Anomaly of an Oil and Gas Well Detected at 40m AGL, showing total magnetic intensity of the site.

To further test remote sensing techniques, the Binghamton University research team worked with Charles Dietrich and Nathan Graber from the NYS DEC to compare the efficiency of different survey methods. Currently, researchers are conducting fieldwork to compare the efficiency of traditional methods of well detection, well detection via a magnetic ground survey, and well detection via a drone-based magnetic survey. This research is showing that using drones equipped with magnetometers is a more efficient way to survey a wide area where wells may be present.

Remote sensing techniques can allow the DEC to more efficiently locate, and then plug, the 30,000+ undocumented oil and gas wells in New York State. Using this new method of well detection, the DEC will be able to inform residents who have unplugged wells on their property, assess the risks of the wells, and plug harmful wells. Residents with wells on or near their property will benefit directly. In addition, and more broadly, New Yorkers will enjoy improved air quality while New York State will be more on track to reaching its emissions targets.

FracTracker thanks Natalia Romanzo for her guest blog contribution. We feel that this technology holds promise for communities impacted by drilling across the nation.

For answers to specific questions about the project, you can email Natalia directly at nromanz1@binghamton.edu.

https://fractracker.org/wp-content/uploads/2019/09/2018-NYS-Oil-and-Gas-Wells-feature-image-2-scaled.jpg6671500Guest Authorhttps://fractracker.org/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngGuest Author2019-09-17 09:00:492021-04-15 14:56:25New Method for Locating Abandoned Oil and Gas Wells is Tested in New York State

By Isabelle Weber, FracTracker Alliance Spring 2019 Intern

Fracking in Pennsylvania: The History

When driving through Pennsylvania, you can see what an impact oil and gas has had on the state. Towns like Oil City and Petrolia speak to the oil and gas industry’s long standing history here. In more recent history, Pennsylvania has been a prime fracking location because of the presence of the Marcellus shale formation that covers over half of the state. With more unconventional oil and gas exploration came impacts to communities, who were denied their right to “clean air, pure water, and the preservation of the natural, scenic, historic, and esthetic values of the environment” as defined by the Pennsylvania Constitution.

Hydraulically fractured wells are often no longer profitable after just one stimulation, after which they are abandoned. Improperly abandoned wells wreak havoc on our communities and our environment. The number of improperly abandoned wells has been increasing over time as companies go bankrupt transfer wells to other companies. These wells can easily go undetected because they are often buried underground, leaving no traces at the surface level.

These unplugged abandoned wells are underneath our homes, our schools, and in our own backyards, negatively impacting our health and the environment.

FracTracker’s West Coast Coordinator Kyle Ferrar shows how abandoned wells are hiding all around us in his investigation of downtown Los Angeles. He used an infrared camera to visualize the plumes of methane and other volatile organic compounds spewing out of abandoned wells in the middle of streets.

Dangers of unplugged abandoned wells

The plugging process consists of filling the well with cement, ensuring that nothing leaks from the well into the surrounding ecosystem. Without that measure in place, the chemical-water solution used to frack the underlying shale, as well as any oil or natural gas still left in the well, can very easily seep into nearby aquifers or into close by waterways. Wells that are not plugged or are not plugged properly leak into nearby aquifers, releasing methane and other volatile organic compounds are continually released from the well into the atmosphere as well. This leakage into the atmosphere and ground water can have disastrous effects on our ecosystem and health.

Abandoned wells are also a dangerous threat because many of their locations are unknown. These wells can ruin the structural integrity of buildings and homes that are unknowingly built on top of them. The methane leaking out of the well is colorless and odorless, meaning that it can easily build-up in homes or elsewhere and cause explosions.

Bankruptcy and Bonds

When an oil and gas company drills a well, they are responsible for making sure that it is plugged properly at the end of the well’s life. This is the case even if the company goes bankrupt. To do this, Pennsylvania government requires that the company put up a bond that is set aside to plug the well properly. This ensures that if the company does go bankrupt, the necessary funds are already set aside to plug the well. Normally, this bond takes the shape of a blanket bond amount of $25,000 which is intended to cover the total expenses that would be incurred in plugging all of the wells a company has in the state. Depending on the number of wells a company possesses, this could mean very little actually being set aside for each individual well.

A shallow well can cost between $8,000 to $10,000 plus, and up to $50,000 or more depending on how difficult it is to plug. In the case of Pennsylvania’s top oil and gas holder Diversified Gas & Oil PLC and its recently acquired. Company Alliance Petroleum Corp, this bond sets aside just $2 per well. With most other companies holding no more than 5,700 wells, this sets aside $4.40 per well. Where the bond amounts fall short in accounting for the cost to plug the hundreds of thousands of abandoned wells across the state, the rest of the cost falls at the feet of taxpayers.

The New Contract

The state government has started to recognize the severity of the situation as they are confronted with a mountain of costs in plugging these wells. To start to mitigate this, the government has recently settled with Diversified Gas & Oil. The company has been ordered to properly plug 1,058 abandoned wells. To do this they have signed on to a $7 million bond with $20,000 to $30,000 bonds for each additional abandoned or non-producing well that is acquired.

Although it is a great start to ensure that these two major companies have the proper bonding amount moving forward, this does not apply to all companies, whose likelihood of going bankrupt puts a lot of financial pressure on Pennsylvanian citizens. Also, these 1,058 wells are only the tip of the iceberg, with the DEP estimating that there are between 100,000 and 560,000 total abandoned wells in Pennsylvania, many of which still have unknown locations.

In the 2017 Pennsylvania Oil and Gas Report, it is stated that: “Currently, more abandoned wells are being added to the state’s inventory than are being addressed through permanent plugging through state-issued contracts. Since 2015, DEP has been able to fund the plugging of oil and gas wells only in emergency situations and/or when residents must be temporarily evacuated from their homes due to imminent threats that legacy wells pose when well integrity is compromised.” They continue on by stating that, considering the historic operating costs and acknowledging the sheer number of wells, properly addressing es the abandoned wells will cost between $150 million and $3.7 billion. The $150 million is an estimation based on the scenario that no more historic legacy wells are discovered, and the $3.7 billion is based on if 200,000 more are found, a more likely scenario.

The funding to cover the costs of plugging these abandoned wells comes from surcharges of $150 and $200 established by the 1984 Oil and Gas Act for each oil well permit and gas well permit. The DEP has received fewer permits in recent years meaning that there are very little funds to resolve this issue. This means that eventually this public health and environmental burden will have to fall at the feet of the taxpayers.

This makes the state’s step in the right direction look more like a tip toe. With no real, substantial plans to locate and address the large amount of wells across the state, the government is putting their people at risk because these abandoned wells are not harmless.

Washington County Case study

Washington County can be used as a window into the abandoned well crisis in Pennsylvania. This county sits in the middle of the Marcellus Shale formation, making it a key site for unconventional oil and gas development. According to the DEP, there are 215 abandoned, orphaned wells in Washington county, but realistically we know that there are likely many more than that.

The Pennsylvania Spatial Data Access (PASDA) has derived a dataset from historical sources to determine the possible locations of other abandoned wells. These historical documents include the WPA, Ksheet, and Hsheet collections. This data set highlights over 6,000 locations where an abandoned oil and gas well could be located.

This is a testament to how many of these wells exist without our knowledge. If this difference in DEP records and possible wells is this great in Washington County, then we face the enormous potential problem of tens of thousands of additional abandoned wells that need to be resolved. The effects of these wells are real and they must be identified quickly.

These are some of the physical effects of abandoned wells:

Fig 1. A Collapsed Well Opening – A Physical Hazard (photo credit: Friends of Oil Creek State Park)

Fig. 2. Well Spouting Acid Water. Well later plugged by DEP (photo credit: Friends of Oil Creek State Park)

Fig. 3. Oil Seepage (photo credit:(photo credit: Friends of Oil Creek State Park)

Fig. 4. Abandoned Well and Storage Tank (photo credit: Friends of Oil Creek State Park)

Conclusion

Pennsylvania is facing a mountain of an issue with decades of work ahead. The state must act quickly to ensure the health and protection of our people and our environment, which entails taking active steps to secure an adequate budget to resolve this issue. To start, the state should identify where all of the wells are, set up a financial plan that puts the cost of the plugging process for these wells back onto the oil and gas companies, and begin to take active measures to plug the wells quickly and efficiently.

https://fractracker.org/wp-content/uploads/2019/08/Abandoned-wells-PA-feature.png6671500Intern FracTrackerhttps://fractracker.org/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngIntern FracTracker2019-08-08 14:17:382025-05-02 14:45:21Abandoned Wells in Pennsylvania: We’re Not Doing Enough

https://fractracker.org/wp-content/uploads/2019/07/DSC_0624_LowRes-scaled.jpg9821500Shannon Smithhttps://fractracker.org/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngShannon Smith2019-08-07 09:36:032026-04-28 15:34:37Wildness Lost – Pine Creek

FracTracker is closely mapping and following the petrochemical build-out in Appalachia, as the oil and gas industry invests in petrochemical manufacturing. Much of the national attention on the build-out revolves around the Appalachian Storage Hub (ASH), a venture spearheaded by Appalachian Development Group.

The ASH involves a network of infrastructure to store and transport natural gas liquids and finds support across the political spectrum. Elected officials are collaborating with the private sector and foreign investors to further development of the ASH, citing benefits such as national security, increased revenue, job creation, and energy independence.

Left out of the discussion are the increased environmental and public health burdens the ASH would place on the region, and the fact that natural gas liquids are the feedstock of products such as plastic and resins, not energy.

The “Shale Revolution” brought on by high-volume hydraulic fracturing (fracking) in this region encompasses thousands of wells drilled into the Marcellus and Utica-Point Pleasant shale plays across much of the Allegheny Plateau. This area spans from north of Scranton-Wilkes Barre, Pennsylvania, just outside the Catskills Mountains to the East in Susquehanna County, Pennsylvania, and down to the West Virginia counties of Logan, Boone, and Lincoln. The westernmost extent of the fracking experiment in the Marcellus and Utica shale plays is in Noble and Guernsey Counties in Ohio.

Along the way, producing wells have exhibited steeper and steeper declines during the first five years of production, leading the industry to develop what they refer to as “super laterals.” These laterals (the horizontal portion of a well) exceed 3 miles in length and require in excess of 15 million gallons of freshwater and 15,000 tons of silica sand (aka, “proppant”)[1].

The resource-intense super laterals are one way the industry is dealing with growing pressure from investors, lenders, the media, state governments, and the public to reduce supply costs and turn a profit, while also maintaining production. (Note: unfortunately these sources of pressures are listed from most to least concerning to industry itself!)

Another way the fracking industry is hoping to make a profit is by investing in the region’s natural gas liquids (NGLs), such as ethane, propane, and butane, to support the petrochemical industry.

The Appalachian Storage Hub

Continued oil and gas development are part of a nascent effort to establish a mega-infrastructure petrochemical complex, the Appalachian Storage Hub (ASH). For those that aren’t familiar with the ASH it could be framed as the fracking industry’s last best attempt to lock in their necessity across Appalachia and nationwide. The ASH was defined in the West Virginia Executive as a way to revitalize the Mountain State and would consist of the following:

“a proposed underground storage facility that would be used to store and transport natural gas liquids (NGLs) extracted from the Marcellus, Utica and Rogersville shales across Kentucky, Ohio, Pennsylvania and West Virginia. Construction of this hub would not only lead to revenue and job creation in the natural gas industry but would also further enable manufacturing companies to come to the Mountain State, as the petrochemicals produced by shale are necessary materials in most manufacturing supply chains…[with] the raw materials available in the region’s Marcellus Shale alone…estimated to be worth more than $2 trillion, and an estimated 20 percent of this shale is composed largely of ethane, propane and butane NGLs that can be utilized by the petrochemical industry in the manufacturing of consumer goods.”

This is yet another example of fracking rhetoric that appeals to American’s sense of patriotism and need for cheaper consumer goods (in this case, plastics), given that they are seeing little to no growth in wages.

While a specific location for underground storage has not been announced, the infrastructure associated with the ASH (such as pipelines, compressor stations, and processing stations) would stretch from outside Pittsburgh down to Catlettsburg, Kentucky, with the latter currently the home of a sizeable Marathon Oil refinery. The ASH “would act like an interstate highway, with on-ramps and off-ramps feeding manufacturing hubs along its length and drawing from the available ethane storage fields. The piping would sit above-ground and follow the Ohio and Kanawha river valley.”

The politics of the ASH – from Columbus and Charleston to Washington DC

Elected officials across the quad-state region are supporting this effort invoking, not surprisingly, its importance for national security and energy independence.

State-level support

West Virginia Senator Joe Manchin (D) went so far as to introduce “Senate Bill 1064 – Appalachian Energy for National Security Act.” This bill would require Secretary of Energy Rick Perry and his staff to “to conduct a study on the national security implications of building ethane and other natural-gas-liquids-related petrochemical infrastructure in the United States, and for other purposes.”

Interestingly, the West Virginia Senator told the West Virginia Roundtable Inc’s membership meeting that the study would not examine the “national security implications” but rather the “additional security benefits” of an Appalachian Storage Hub and cited the following to pave the way for the national security study he is proposing: “the shale resource endowment of the Appalachian Basin is so bountiful that, if the Appalachian Basin were an independent country, the Appalachian Basin would be the third largest producer of natural gas in the world.”

Senator Manchin is not the only politician of either party to unabashedly holler from the Appalachian Mountaintops the benefits of the ASH. Former Ohio Governor, and 2016 POTUS primary participant, John Kasich (R) has been a fervent supporter of such a regional planning scheme. He is particularly outspoken in favor of the joint proposal by Thailand-based PTT Global Chemical and Daelim to build an ethane cracker in Dilles Bottom, Ohio, across the Ohio River from Moundsville, West Virginia. The ethane cracker would convert the region’s fracked ethane into ethylene to make polyethylene plastic. This proposed project could be connected to the underground storage component of the ASH.

Dilles Bottom, OH ethane cracker site. Photo by Ted Auch, aerial assistance provided by LightHawk.

Not to be outdone in the ASH cheerleading department, West Virginia Governor Jim Justice (R), who can’t seem to find any common ground with Democrats in general nor Senator Manchin specifically, is collaborating with quad-state governors on the benefits of the ASH. All the while, these players ignore or dismiss the environmental, social, and economic costs of such an “all in” bet on petrochemicals and plastics.

Even the region’s land-grant universities have gotten in on the act, with West Virginia University’s Appalachian Oil and Natural Gas Research Consortium and Energy Institute leading the way. WVU’s Energy Institute Director Brian Anderson pointed out that, “Appalachia is poised for a renaissance of the petrochemical industry due to the availability of natural gas liquids. A critical path for this rebirth is through the development of infrastructure to support the industry. The Appalachian Storage Hub study is a first step for realizing that necessary infrastructure.”

utilize a new or significantly improved technology;

avoid, reduce or sequester greenhouse gases;

be located in the United States; and,

have a reasonable prospect of repayment.

This type of Public-Private Investment Program is central planning at its finest, in spite of the likelihood that the prospects of the ASH meeting the second and fourth conditions above are dubious at best (even if the project utilizes carbon capture and storage technologies).

Public-Private Investment Programs have a dubious past. In her book “Water Wars,” Vandana Shiva discusses the role of these programs globally and the involvement of institutions like the World Bank and International Monetary Fund:

“public-private partnerships”…implies public participation, democracy, and accountability. But it disguises the fact that the public-private partnership arrangements usually entail public funds being available for the privatization of public goods…[and] have mushroomed under the guise of attracting private capital and curbing public-sector employment.”

In response to the Department of Energy’s Title XVII largesse, Congresswoman Pramila Jayapal and Ilhan Omar introduced Amendment 105 in Rule II on HR 2740. According to Food and Water Watch, this amendment would restrict “the types of projects the Department of Energy could financially back. It would block the funding for ALL projects that wouldn’t mitigate climate change.”

The only condition of Department of Energy’s Title XVII loan program ASH is guaranteed to meet is the third (be located in the United States), but as we’ve already mentioned, the level of foreign money involved complicates the domestic facade.

Foreign involvement in the ASH lends credence to Senator Manchin’s and others’ concerns about where profits from the ASH will go, and who will be reaping the benefits of cheap natural gas. The fact that the ASH is being heavily backed by foreign money is the reason Senator Manchin raised an issue with the outsized role of state actors like Saudi Arabia and China as well as likely state-backed private investments like PTT Global Chemical’s. The Senator even cited how a potential $83.7 billion investment in West Virginia from China’s state-owned energy company, China Energy, would compromise “domestic manufacturing and national security opportunities.”

“Critical” infrastructure

With all of the discussion and legislation focused on energy and national security, many don’t realize the output of the ASH would be the production of petroleum-based products: mainly plastic, but also fertilizers, paints, resins, and other chemical products.

Bills like this and the not unrelated “critical infrastructure” bills being shopped around by the American Legislative Exchange Council will amplify the rural vs urban and local vs state oversight divisions running rampant throughout the United States. The reason for this is that yet another natural resource boom/bust will be foisted on Central Appalachia to fuel urban growth and, in this instance, the growth and prosperity of foreign states like China.

Instead of working night and day to advocate for Appalachia and Americans more broadly, we have legislation in statehouses around the country that would make it harder to demonstrate or voice concerns about proposals associated with the ASH and similar regional planning projects stretching down into the Gulf of Mexico.

Producing wells mapped

Impacts from the ASH and associated ethane cracker proposals will include but are not limited to: an increase in the permitting of natural gas wells, an increase in associated gas gathering pipelines across the Allegheny Plateau, and an exponential increase in the production of plastics, all of which are harmful to the region’s environment and the planet.

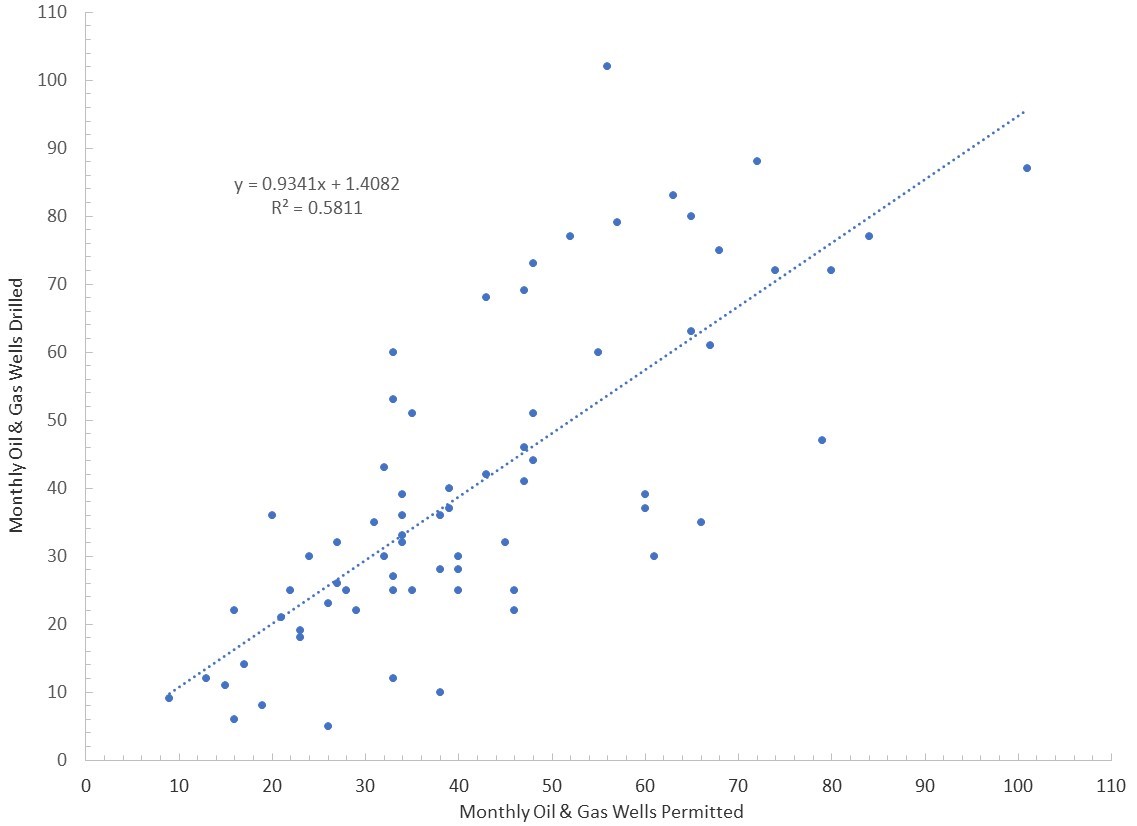

The production of the region’s fracked wells will determine the long-term viability of the ASH. From our reading of things, the permitting trend we see in Ohio will have to hit another exponential inflection point to “feed the beast” as it were. Figure 1 shows an overall decline in the number of wells drilled monthly in Ohio.

Figure 2, below it, shows the relationship between the number of wells that are permitted verse those that are actually drilled.

Figures 1. Monthly (in blue) and cumulative (in orange) unconventional oil and gas wells drilled in Ohio, January, 2013 to November, 2018

Figure 2. Permitted Vs Drilled Wells in Ohio, January, 2013 to November, 2018

That supply-demand on steroids interaction will likely result in an increased reliance on “super laterals” by the high-volume hydraulic fracturing industry. These laterals require 5-8 times more water, chemicals, and proppant than unconventional laterals did between 2010 and 2012.

Given this, we felt it critical to map not just the environmental impacts of this model of fracking but also the nuts and bolts of production over time. The map below shows the supply-demand links between the fracking industry and the ASH, not as discrete pieces or groupings of infrastructure, but rather a continuum of up and downstream patterns.

The current iteration of the map shows production values for oil, natural gas, and natural gas liquids, how production for any given well changes over time, and production declines in newer wells relative to those that were fracked at the outset of the region’s “Shale Revolution.” Working with volunteer Gary Allison, we have compiled and mapped monthly (Pennsylvania and West Virginia) and quarterly (Ohio)[2] natural gas, condensate, and natural gas liquids from 2002 to 2018.

This map includes 15,682 producing wells in Pennsylvania, 3,689 in West Virginia, and 2,064 in Ohio. We’ve also included and will be updating petrochemical projects associated with the ASH, either existing or proposed, across the quad-states including the proposed ethane cracker in Dilles Bottom, Ohio and the ethane cracker under construction in Beaver County, Pennsylvania, along with two rumored projects in West Virginia.

We will continue to update this map on a quarterly basis, will be adding Kentucky data in the coming months, and will be sure to update rumored/proposed petrochemical infrastructure as they cross our radar. However, we can’t be everywhere at once so if anyone reading this hears of legitimate rumors or conversations taking place at the county or township level that cite tapping into the ASH’s infrastructural network, please be sure to contact us directly at info@fractracker.org.

By Ted Auch, Great Lakes Program Coordinator, FracTracker Alliance with invaluable data compilation assistance from Gary Allison

Feature Photo: Ethane cracker plant under construction in Beaver County, PA. Photo by Ted Auch, aerial assistance provided by LightHawk.

[1] For a detailed analysis of the HVHF’s increasing resource demand and how lateral length has increased in the last decade the reader is referred to our analysis titled “A Disturbing Tale of Diminishing Returns in Ohio” Figures 12 and 13.

[2] Note: For those Bluegrass State residents or interested parties, Kentucky data is on its way!

https://fractracker.org/wp-content/uploads/2019/07/Cracker-Plant-2-scaled.jpg6831500Ted Auch, PhDhttps://fractracker.org/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngTed Auch, PhD2019-07-23 14:37:052021-04-15 14:56:27The Underlying Politics and Unconventional Well Fundamentals of an Appalachian Storage Hub

California regulators halt well permitting after Consumer Watchdog and FracTracker reveal a surge in well permits under California Governor Newsom

October 24th, 2019 update:

There have been several exciting updates since FracTracker Alliance and Consumer Watchdog released a report on fracking and regulatory corruption under Governor Newsom’s administration, detailed in the article below.

On July 11th, 2019, immediately following the report’s release, Governor Newsom fired Ken Harris, head of California’s Division of Oil, Gas, and Geothermal Resources (DOGGR).

“The Governor has long held concerns about fracking and its impacts on Californians and our environment, and knows that ultimately California and our global partners will need to transition away from oil and gas extraction. In the weeks ahead, our office will work with you to find new leadership of (the division) that share this point of view and can run the division accordingly.”

FracTracker Alliance supports the governor’s decision and hopes that new leadership acts in the best interests of Californians while moving the state towards 100% renewable energy.

Two months later in September, it was announced that no new fracking permits had been approved in California since the report was issued. We’re thrilled to see this immediate cessation. Yet, while new fracking activity has halted, other forms of oil and gas development continue to threaten Californian’s health and natural resources.

FracTracker Alliance’s review of public records found that DOGGR issued approximately 1,200 permits for steam injection and other “enhanced recovery” techniques through September 2nd, a 60% increase from the 749 permits issued in the same period last year. Sources within DOGGR revealed that at least 40 illegal oil spills from wells were ongoing in Kern and Santa Barbara Counties.

A final development came on October 12th, when Governor Newsom signed a bill to prevent oil and gas development on state lands. As state lands often neighbor federal lands, this bill will play a role in protecting federal land from pipelines, wells, and other polluting infrastructure. Newsom also changed the name of DOGGR to the “Geologic Energy Management Division,” and modified its mission to include protecting public health and environmental quality.

We remain hopeful that Newsom will take a bold stance in leading California away from fossil fuels.

Original July 11th, 2019 FracTracker article:

FracTracker Alliance and Consumer Watchdog have uncovered new data showing an increase in oil and gas permitting by California regulators in 2019 compared to 2018, calling into question Governor Gavin Newsom’s climate commitment. Even more concerning, this investigation found that state regulators are heavily invested in the oil companies they regulate.

FracTracker Alliance’s new report with Consumer Watchdog compares oil and gas permitting policies of the current Governor Gavin Newsom’s administration with that of former Governor Jerry Brown’s administration.

The former lieutenant governor to Brown, Governor Newsom has set out to make a name for himself. As part of stepping out of Brown’s shadow, Newsom has expressed support for a Just Transition away from fossil fuels. Governor Newsom’s 2020 budget plan includes environmental justice measures and an unprecedented investment to plan for this transition that includes investments in job training.

Yet five months into Governor Newsom’s first term, regulators are on track to allow companies to drill and “frack” more new oil and gas wells than Brown allowed in 2018. The question now is: will Governor Newsom actually take the next step that Brown could not, and prioritize the reduction of oil extraction in California?

In addition, the Consumer Watchdog report reveals that eight California regulators with the Division of Oil, Gas, and Geothermal Resources (DOGGR) are heavily invested in the oil companies they regulate. FracTracker and Consumer Watchdog are calling for the the removal of DOGGR officials with conflicts of interest, and an immediate freeze on new well approval. Read the letter to Governor Newsom here.

Governor Brown’s Legacy

Around the world, Brown is recognized as a climate warrior. His support of solar energy technology and criticisms of the nuclear and fossil fuel industry was ultimately unique in the late 1970’s.

In 1980, during his second term as Governor and short presidential campaign, he decried that fellow democrat and incumbent President Jimmy Carter had made a “Faustian bargain” with the oil industry. Since then, he has continued to push for state controls on greenhouse gas emissions. To end his political career, Brown hosted an epic climate summit in San Francisco, California, which brought together climate leaders, politicians, and scientists from around the world.

While Brown championed the reduction of greenhouse gas emissions, his policies in California were contradictory. While front-line communities called for setbacks from schools, playgrounds, hospitals and other sensitive receptors, Brown ignored these requests. Instead he sought to spur oil production in the state. Brown even used state funds to explore his private properties for oil and mineral resources that could be exploited for personal profit.

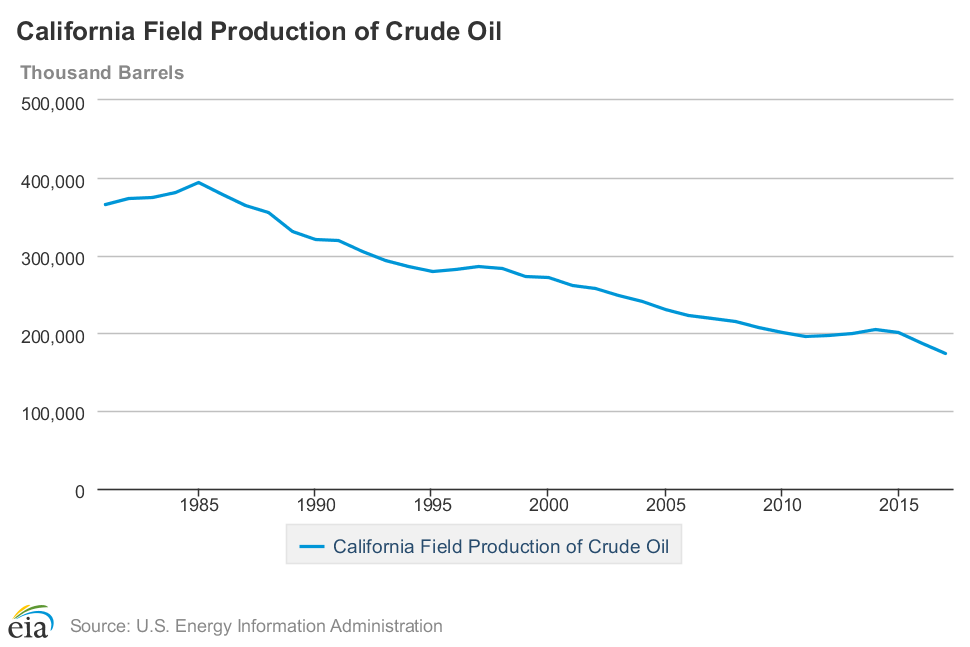

Brown’s terms in the Governor’s office show trends of increasing oil and gas production. The chart in Figure 1 shows that during his first term (1979-1983), California oil extraction grew towards a peak in production. Then in 2011 at the start of Brown’s second term (2011-2019), crude oil production again inflected and continued to increase through 2015, ending a 25-year period of relatively consistent reduction.

We are therefore interested in looking at existing data to understand if moving forward, Governor Newsom will continue Brown’s legacy of support for California oil production. We start by looking at the first half of 2019, the beginning of Governor Newsom’s term, to see if his administration will also allow the oil and gas industry to increase extraction in California.

Figure 1. Chart of California’s historic oil production, from the EIA

Analysis

The FracTracker Alliance has collaborated with the non-profit Consumer Watchdog to review records of oil and gas well permits issued in 2018 and thus far into 2019.

Records of approved permits were obtained from the CA Department of Conservation’s Division of Oil Gas and Geothermal Resources (DOGGR). Weekly summaries of approved permits for the 52 weeks of 2018 and the first 22 weeks of 2019 (January 1st-June 3rd) were compiled, cleaned, and analyzed. Notices of well stimulations were also included in this analysis. The data is mapped here in the Consumer Watchdog report, as well as in more detail below in the map in Figure 2.

Figure 2. Map of California’s Permits, 2018 and 2019

At FracTracker, we are known for more than simply mapping, so we have, of course, extracted all the information that we can from this data. The dataset of DOGGR permits included details on the type of permit as well as when, where, and who the permits were granted. With this information we were able to answer several questions.

Of particular note and worthy of prefacing the data analysis was the observation of the very low numbers of permits granted in the LA Basin and Southern California, as compared to the Central Valley and Central Coast of California.

First, what are the types of permits issued?

Regulators require operators to apply for permits for a number of activities at well sites. This dataset includes permits to drill wells, including re-drilling existing wells, permits to rework existing wells, and permits to “sidetrack”. Well stimulations using techniques such as hydraulic fracturing and acid fracturing also require permits, as outline in CA State Bill 4.

How many permits have regulators issued?

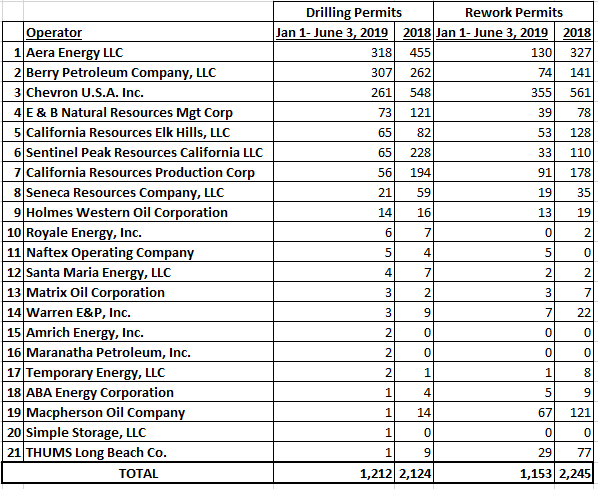

In 2018, DOGGR approved 4,368 permits, including 2,124 permits to drill wells. In 2019, DOGGR approved 2,366 permits from January 1 – June 3, including 1,212 permits to drill wells. At that rate, DOGGR will approve 5,607 total permits by the end of 2019, including 2,872 wells.

That is an increase of 28.3% for total permits and an increase of 35.3% for drilling oil and gas wells.

DOGGR also issued 222 permits for well stimulations in 2018. So far in 2019, DOGGR has issued 191 permits for well stimulations, an increase of 103.2%.

Who is applying for permits?

As shown in Table 1 below, the operators Chevron U.S.A. Inc., Aera Energy LLC ( a joint conglomerate of Shell Oil Company and ExxonMobil), and Berry Petroleum Company, LLC dominate the drilling permit counts for both 2018 and 2019.

Aera has obtained the most drilling permits thus far into 2019, while Chevron obtained the most permits in 2018, almost 100 more than Aera. In 2019, Chevron was issued almost 3 times the amount of rework permits as Aera, and both have outpaced Berry Petroleum.

Table 1. Permit Counts by Operator

Where are the permits being issued?

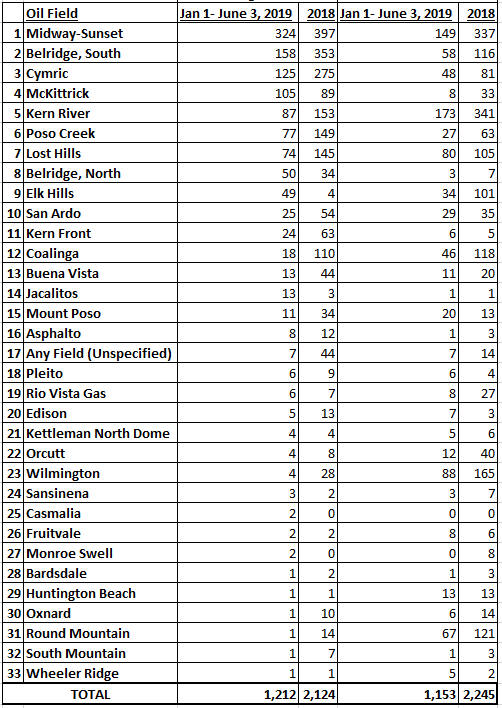

Data presented in Table 2 indicate which fields are being targeted for drilling and rework permits. While the 2019 data represents less than half the year, the number of drilling permits is almost equal to the total drilling permit count for 2018.

Majority players in the Midway-Sunset field are Berry Petroleum and Chevron. South Belridge is dominated by Aera Energy and Berry Petroleum. The Cymric field is mostly Chevron and Aera Energy; McKittrick is mostly Area Energy and Berry Petroleum. The Kern River field, which has by far the most reworks (most likely due to its massive size and age) is entirely Chevron.

The details of this analysis show that DOGGR has allowed for a modest increase in permits for oil and gas wells in 2019. The increase in well stimulations in 2019 is estimated to be larger, at 103.2%.

There was the consideration that this could be a seasonal phenomenon since we extrapolated from data encompassing just less than the first half of the year. But upon reviewing data for several other years, that does not seem to be the case. The general trend was instead increasing numbers of permits as each year progresses, with smaller permit counts through the first half of the year.

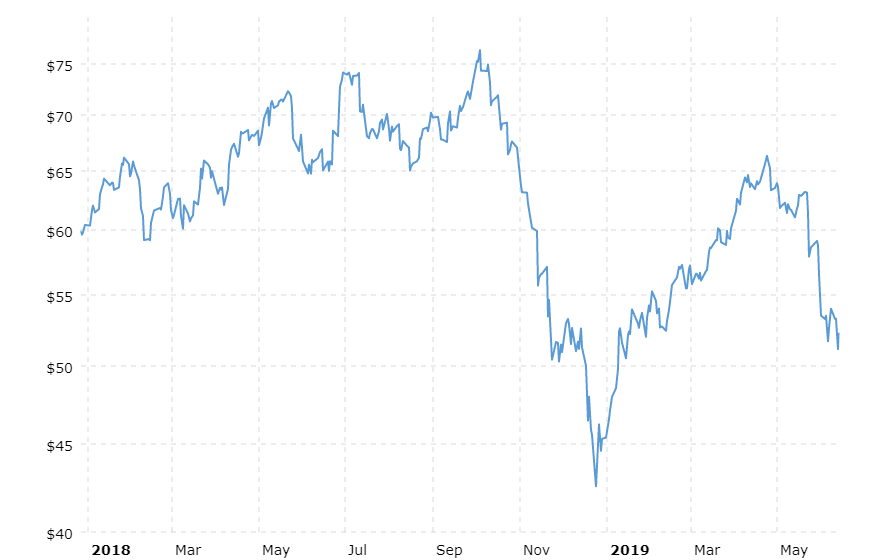

Oil prices do not provide much explanation either. The chart in Figure 3 shows that crude prices were higher in 2018 than they have been for the vast majority of 2019. The increase in permits could be the result of oil and gas operators like Chevron and Aera anticipating a stricter regulatory climate under Governor Newsom. Operators may be securing as many permits as possible, while DOGGR is still liberally issuing them. This could be a consequence of the Governor’s recognition of the need for California to begin a managed decline of fossil fuel production and end oil drilling in California.

Could this be an early industry death rattle?

Figure 3. Crude prices in 2018 and 2019

By Kyle Ferrar, Western Program Coordinator, FracTracker Alliance

https://fractracker.org/wp-content/uploads/2019/07/inglewood-field-ca-feature-1-scaled.jpg6671500Kyle Ferrar, MPHhttps://fractracker.org/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngKyle Ferrar, MPH2019-07-11 14:48:462021-04-15 14:56:28Permitting New Oil and Gas Wells Under the Newsom Administration

A new bill proposed by California State Assembly Member Al Muratsuchi (D), AB345, seeks to establish a minimum setback distance of 2,500′ between oil and gas wells and sensitive sites including occupied dwellings, schools, healthcare facilities, and playgrounds. A setback distance for oil and gas development is necessary from a public health standpoint, as the literature unequivocally shows that oil and gas wells and the associated infrastructure pose a significant risk to the communities that live near them.

FracTracker Alliance conducted a spatial analysis to understand the impact a 2,500’ well setback would have on oil and gas expansion in California. In a previous report, The Sky’s Limit California (Oil Change Internal, 2018), Fractracker data showed that 8,493 active or newly permitted oil and gas wells were located within a 2,500’ buffer of sensitive sites. At the time it was estimated that 850,000 Californians lived within the setback distance of at least one of these oil and gas wells.

This does not bode well for Californians, as a recently published FracTracker literature review found that health impacts resulting from living near oil and gas development include cancer, infant mortality, depression, pneumonia, asthma, skin-related hospitalizations, and other general health symptoms. Studies also showed that health impacts increased with the density of oil and gas development, suggesting that health impacts are dose dependent. Living closer to more oil and gas sites means you are exposed to more health-threatening contamination.

An established setback is therefore necessary to alleviate some of these health burdens carried by the most vulnerable Environmental Justice (EJ) communities. Health assessments by the Los Angeles County Department of Health and studies on ambient air quality near oil fields by Occidental College Researchers support the assumption that 2,500′ is the necessary distance to help alleviate the harsh conditions of degraded air quality. Living at a distance beyond 2,500′ from an oil and gas site does not mean you are not impacted by air and water contamination. Rather the concentrations of contaminants will be less harmful. In fact studies showed that health impacts increased with proximity to oil and gas, with associated impacts potentially experienced by communities living at distances up to 9.3 miles (Currie et al. 2017) and 10 miles (Whitworth et al. 2017).

Assembly Bill 345

This analysis assesses the potential impact of State Assembly member Al Muratsuchi’s Assembly Bill 345 on California’s oil and gas extraction and production. Specifically, AB345 establishes a minimum 2,500’ setback requirement for future oil and gas development. It does not however directly address existing oil and gas permits.

The bill includes the following stipulations and definitions:

All new oil and gas development, that is not on federal land, are required to be located at least 2,500′ from residences, schools, childcare facilities, playgrounds, hospitals, or health clinics.

In this case the redrilling of a previously plugged and abandoned oil or gas well or other rework operation is to be considered new oil and gas development.

“Oil and gas development” means exploration for and drilling production and processing of oil, gas or other gaseous and liquid hydrocarbons; the flowlines; and the treatment of waste associated with that exploration, drilling, production, and processing.

“Oil and gas development” also includes hydraulic fracturing and other stimulation activities.

“Rework operations” means operations performed in the well bore of an oil or gas well after the well is completed and equipped for production, done for the purpose of securing, restoring, or improving hydrocarbon production in the subsurface interval that is the open to production in the well bore.

The bill does not include routine repairs or well maintenance work.

Map

Figure 1. Map of Wells within a 2,500′ Setback Distance from Sensitive Receptor Sites. The map below shows the oil and gas wells and permits that fall within the 2,500′ setback distance from sensitive receptor sites. Summaries of these well counts and discussions of these well types are included below as well.

Map of Wells within a 2,500′ Setback Distance from Sensitive Receptor Sites

The California Environmental Justice Alliance (CEJA) has just released their 2018 Environmental Justice Agency Assessment, which used FracTracker’s data and mapping to assess environmental equity in the state regulation of oil permitting and drilling. The report issued the Division of Oil, Gas, and Geothermal Resources (DOGGR) a failing grade of ‘F’. According to the report, “DOGGR is aware that the proposed locations of many drilling activities are in or near EJ communities, but approves permits irrespective of known health and safety risks associated with neighborhood drilling.”

FracTracker’s analysis of low income communities in Kern County shows the following:

There are 16,690 active oil and gas production wells located in census blocks with median household incomes of less than 80% of Kern’s area median income (AMI).

Therefore about 25% (16,690 out of 67,327 total) of Kern’s oil and gas wells are located within low-income communities.

Of these 16,690 wells, 5,364 of them are located within the 2,500′ setback distance from sensitive receptor sites such as schools and hospitals (32%) vs 13.1% for the rest of the state.

Using freshly published Division of Oil, Gas, and Geothermal Resources (DOGGR) data (6/3/19), we find that there are 9,835 active wells that fall within the 2,500’ setback distance, representing 13.1% of the total 74,775 active wells in the state.

There are 6,558 idle wells that fall within the 2,500’ setback distance, of nearly 30,000 total idle wells in the state. Putting these idle wells back online would be blocked if the wells require reworks to restart or ramp up production. For the most part operators do not intend for most idle wells to come back online. Rather operators are just avoiding the costs of plugging and properly abandoning the wells. To learn more about this issue, see our recent coverage of idle wells here.

Of the 3,783 permitted wells not yet in production, or “new wells,” 298 (7.8%) are located within the 2,500’ buffer zone.

Getting a count of plugged wells within the setback distance is more difficult because there is not a complete dataset, but there are over 30,000 wells in areas with active production that would be blocked from being redrilled. In total there are 122,209 plugged wells listed in the DOGGR database.

Permits

We also looked at permit applications that were approved in 2018, including permits for drilling new wells, well reworks, deepening wells and well sidetracks. This may be the most insightful of all the analyses.

Within the 2018 permit data, we find that 4,369 permits were approved. Of those 518 permits (about 12%) were granted within the proposed 2,500’ setback. Of the permits 25% were for new drilling, 73% were for reworks, and 2% were for deepening existing wells. By county, 42% were in Kern, 24% were in Los Angeles, 14% in Ventura, 6% in Santa Barbara, 3% in Fresno, and 2% or less in Glenn, Monterey, Sutter, San Joaquin, Colusa, Solano, Orange and Tehama, in descending order.

SCAQMD Notices

In LA, Rule 1148.2 requires operators to notify the South Coast Air Quality Management District (SCAQMD) of activities at well sites, including stimulations and reworks. These data points are reiterative of the “permits” discussed above, but the dataset is specific to the SCAQMD and includes additional activities. Of the 1,361 reports made to the air district since the beginning of 2018 through April 1, 2019; 634 (47%) were for wells that would be impacted by the setback distance; 412 incidences were for something other than “well maintenance” of which 348 were for gravel packing, 4 for matrix acidizing, and 65 were for well drilling. We are not sure where gravel packing falls, in reference to AB345.

A major consideration is that this rule may force many active wells into an idle status. If the onus of plugging wells falls on the state, these additional idle wells could be a major liability for the public. Fortunately AB1328 recently defined new idle well rules. The rules entice operators to plug and abandon idle wells. If rule 1328 is effective at reducing the stock of idle wells, these two bills could complement each other. (For more information on idle wells, read FracTracker’s recent analysis, here: https://fractracker.org/2019/04/idle-wells-are-a-major-risk/)

State Bill 4 Well Stimulation Reporting

We also analyzed data reported to DOGGR under the well stimulation requirements of CA State Bill 4 (SB4), the 2013 bill that set a framework for regulating hydraulic fracturing in California. Part of the bill required an independent scientific study to be conducted on oil and gas well stimulation, including acid well stimulation and hydraulic fracturing. Since 2016 operators have been required to secure special permits to stimulate wells, which includes hydraulic fracturing and several other techniques. To learn more about this state regulation read FracTracker’s coverage of SB4. From January 1, 2016 to April 1, 2019, there have been 576 well stimulation treatment permits granted under the SB4 regulations. Only 1 hydraulic fracturing event, permitted in Goleta, would have been impacted by a 2,500’ setback in 2018.

Support for AB345

After being approved by the CA Assembly Natural Resources Committee in a 7-6 vote, the bill did not make it up for a vote in the Senate Appropriations Committee during the 2019 legislative session. The bill was described by the committee as “promising policies that need more time for discussion.” AB345 is now a two-year bill in the state Senate and will be reconsidered by the committee in January of 2020. The Chairperson of the Appropriations Committee, Lorena Gonzalez, indicated her general support for the policy and committed to working with the author to find a way to move the bill forward at the end of the session.

By Kyle Ferrar, Western Program Coordinator, FracTracker Alliance

Feature image by David McNew, Getty Images

https://fractracker.org/wp-content/uploads/2019/06/SignalHill_DavidMcNew_GettyImages_edit.jpg400900Kyle Ferrar, MPHhttps://fractracker.org/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngKyle Ferrar, MPH2019-07-02 12:03:382021-04-15 14:56:29Impact of a 2,500′ Oil and Gas Well Setback in California

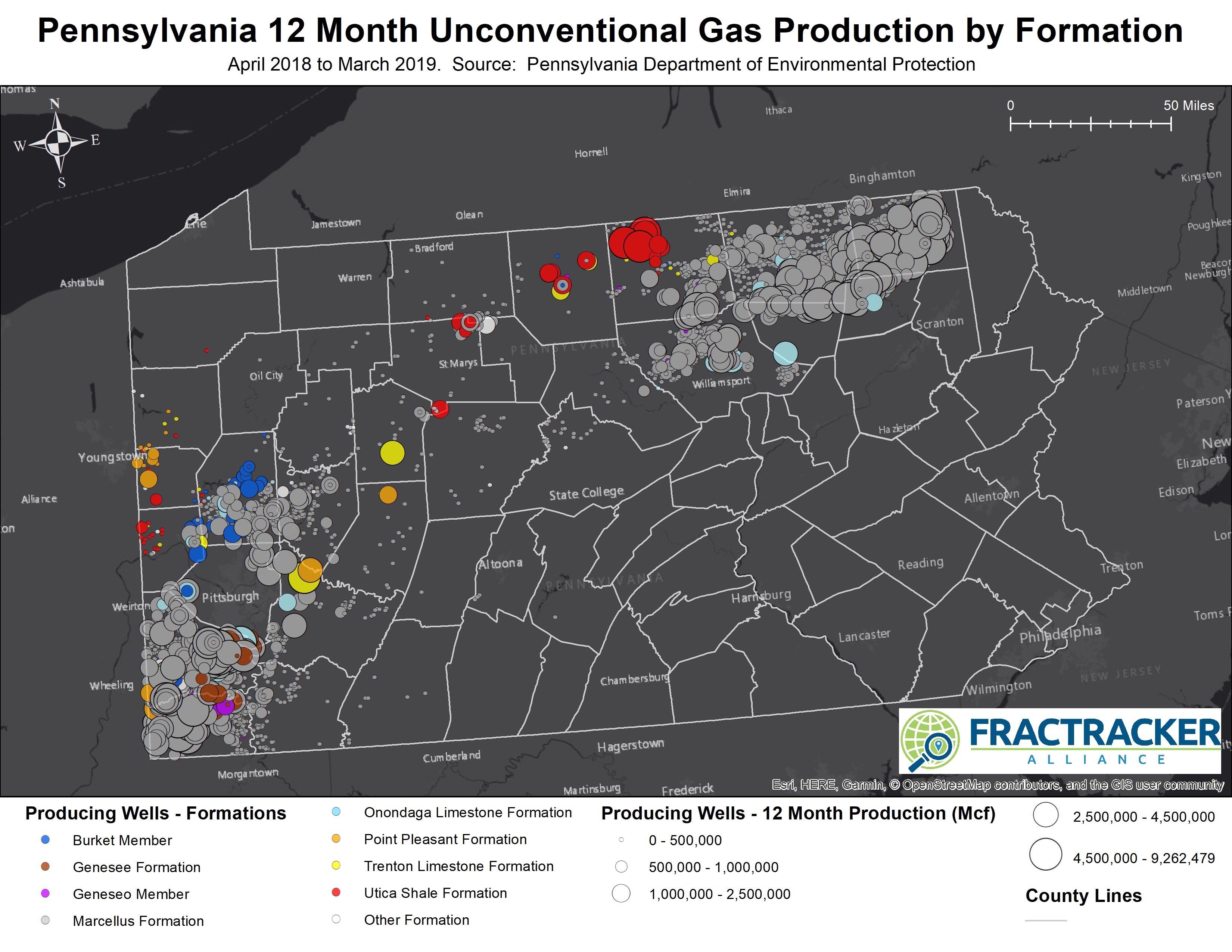

The FracTracker Alliance tends to look mostly at the impacts of drilling, from violations affecting surface and ground water to forest fragmentation to neighbors breathing diesel exhaust near disposal wells. We also try to give residents tools to help predict where future activity will occur, but as this article details, such predictive tools can do little more than trail moving targets. To that end, we have taken a look into areas where gas production is high for unconventional wells in the state, which are likely sites of future development.

The Pennsylvania Department of Environmental Protection’s (DEP) Production Report is self-reported by the various operators active in the state. Unconventional wells generate a large quantity of natural gas, measured in thousands of cubic feet (Mcf), as well as limited amounts of oil and condensate, both of which are measured in 42 gallon barrels. In this analysis, we are only considering the gas production.

In the map above, you can click on any well to learn more about the production values, along with a variety of other information including the well’s formation and age. The age was calculated by counting days from the spud date to the end of the report cycle, March 31, 2019.

Top Average Gas Production by County – April 2018 to March 2019

County

Producing Wells

Avg. Production (Mcf)

Production Rank

Avg. Age of Producing Wells

Age Rank

Wyoming

251

1,269,156

1

5 Yr / 10 Mo / 4 Days

12

Sullivan

128

1,087,868

2

5 Yr / 2 Mo/ 24 Days

8

Allegheny

117

1,075,018

3

4 yr/ 2 Mo / 7 Days

2

Susquehanna

1,429

1,066,734

4

5 Yr / 6 Mo / 22 Days

10

Greene

1,131

796,755

5

5 yr / 10 Mo / 28 Days

13

Figure 1 – This table shows the top five counties in Pennsylvania for per-well unconventional gas production. The final column shows the county ranking for the average age of wells, from youngest to oldest

We can also see this data summarized by county, where average production and age values are available on a county by county basis (see Figure 1). Hydrocarbon wells are known to decrease production steeply over time, a phenomenon known as the decline curve, so it is not surprising to see a relatively young inventory of wells represented in the list of top five counties with per-well gas production. Age is not the only factor in production values, however, as certain geographies simply contain more accessible gas resources than others.

Figure 2 – 12 month gas production and age of well. Production is usually much higher during the earliest phases of the well’s production life. This does not include wells that have been plugged or taken out of production. Click on image for full-sized view.

In Figure 2, we look at the production of all unconventional wells in the state, expecting to see the highest production in younger wells. This mostly appears to be the case, but as mentioned above, there are also hot and cold spots with respect to production. A notable variable in this consideration is producing formation.

Since 93% (8,730 out of 9,404) of unconventional wells reporting gas production are in the Marcellus Shale Formation, the traditional hot spots in the northeastern and southwestern portions of the state heavily skew the overall totals in terms of both production and number of wells. Other formations of note include the Onodaga Limestone (137 wells, 1.5% of total), Burket Member (117 wells, 1.2%), Genesee Formation (104 wells, 1.1%), and the Utica Shale (99 wells, 1.1%) (Figure 3).

Figure 3 – Unconventional gas production over 12 months, showing formation. Click on image for full-sized view.

Drillers have been exploring some of these formations for decades. In fact, the oldest producing well that is currently classified as unconventional was 13,435 days old as of March 31, which works out to 36 years, 9 months, and 12 days.

However, this is fairly rare – only 384 (4%) of the 9,404 producing wells were more than 10 years old. 5,981 wells (64%) are between 5 and 10 years old, with the remaining 3,039 wells (32%) younger than 5 years old.

This does not take into account wells of any age that have been plugged or otherwise taken out of production.

Age of Pennsylvania’s active wells

< 5 years old

5-10 years old

> 10 years old

Utica Shale

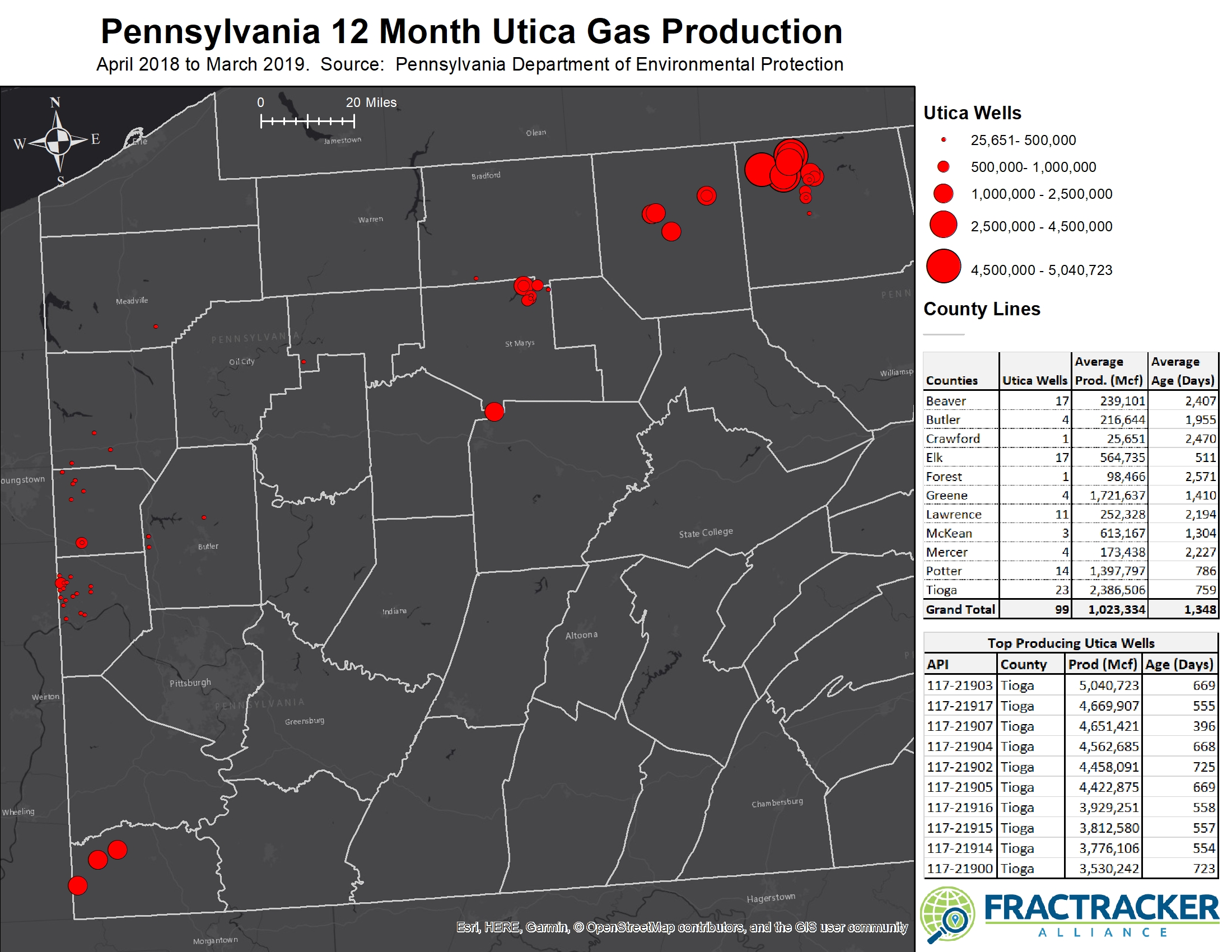

The Utica Shale is worth a special mention here for a couple of reasons. First, we must acknowledge its prominence in neighboring Ohio, which has 2,160 permitted Utica wells to go with just 40 permitted Marcellus wells, the prevalence of the two plays seems to invert just as one passes over the state line. And yet, the most productive Utica wells are near the border with New York, not Ohio.

In fact, each of the top 11 producing Utica wells during the 12 month period were located in Tioga County. It’s worth noting that these are all between one and two years old, which would have given the wells time to be drilled, fracked, and brought into production, while still being in the prime of their production life. Compared to the Marcellus, sample size quickly becomes an issue when analyzing the Utica in Pennsylvania (Figure 4).

Figure 4 – Producing Utica wells in Pennsylvania. Note that the cluster of heavily producing wells in Tioga and Potter Counties near the New York border are mostly young wells where higher production would be expected. Click on image for full sized view.

Second, portions of the Utica are known for their wet gas content, meaning that the gas has significant quantities of natural gas liquids (NGLs) including ethane, propane, and butane, which are gaseous at ambient temperatures but typically condensed into liquid form by oil and gas companies. These are used for specialized fuels and petrochemical feedstocks, and are therefore more valuable than the methane in natural gas.

The production report does not capture the amount of NGLs in the gas, but a map from the Energy Information Administration shows the entire play, noting that the composition is dryer on the eastern portions of the play. In fact, a wet gas composition along the Ohio border might help to explain continued interest in what are otherwise well below average gas production results for Pennsylvania.

A Moving Target

It is difficult to predict where the industry will focus its attention in the coming months and years, but taking a look at production and formation data can give us a few clues. Obviously, operators who found a particularly productive pocket of hydrocarbons are likely to keep drilling more holes in the ground in those areas until production is no longer profitable. Therefore, impacts to water, air, and nearby residents can be expected to continue in heavily drilled areas largely because the production level makes it attractive for drillers.

On the other hand, we should not assume that areas that are currently not productive are off the table for future consideration, either. Different formations are productive in different geographies, so a sweet spot for the Marcellus might be a dud in the Utica, or vice versa.

Finally, when comparing production, we must always take the age of the well into consideration, as all oil and gas wells can be expected to start off with a short period of very high production, followed by years of ever-diminishing returns throughout the expected 10 to 11 year lifecycle of the well. Because of this, what seems like a hotspot now may look below average in a similar analysis in three to four years, particularly in formations with relatively light drilling activity. This means that the top list of production by well could change over time, so be sure to check back in with FracTracker to see how events unfold.

By Matt Kelso, Manager of Data and Technology, FracTracker Alliance

https://fractracker.org/wp-content/uploads/2019/06/Washington-County-Rig-2-scaled.jpg6671500Matt Kelso, BAhttps://fractracker.org/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngMatt Kelso, BA2019-06-10 12:07:422021-04-15 14:56:30Production and Location Trends in PA: A Moving Target

Designating a well as “idle” is a temporary solution for operators, but comes at a great economic and environmental cost to Californians

Idle wells are oil and gas wells which are not in use for production, injection, or other purposes, but also have not been permanently sealed. During a well’s productive phase, it is pumping and producing oil and/or natural gas which profit its operators, such as Exxon, Shell, or California Resources Corporation. When the formations of underground oil pools have been drained, production of oil and gas decreases. Certain techniques such as hydraulic fracturing may be used to stimulate additional production, but at some point operators decide a well is no longer economically sound to produce oil or gas. Operators are supposed to retire the wells by filling the well-bores with cement to permanently seal the well, a process called “plugging.”

A second, impermanent option is for operators to forego plugging the well to a later date and designate the well as idle. Instead of plugging a well, operators cap the well. Capping a well is much cheaper than plugging a well and wells can be capped and left “idle” for indefinite amounts of time.

Well plugging

Unplugged wells can leak explosive gases into neighborhoods and leach toxic fluids into drinking waters. Plugging a well helps protect groundwater and air quality, and prevents greenhouse gasses from escaping and expediting climate change. Therefore it’s important that idle wells are plugged.

Wells are left idle for two main reasons: either the cost of plugging is prohibitive, or there may be potential for future extraction when oil and gas prices will fetch a higher profit margin. While idle wells are touted by industry as assets, they are in fact liabilities. Idle wells are often dumped to smaller or questionable operators.

Orphaned wells

Wells that have passed their production phase can also be “orphaned.” In some cases, it is possible that the owner and operator may be dead! Or, as often happens, the smaller operators go out of business with no money left over to plug their wells or resume pumping. When idle wells are orphaned from their operators, the state becomes responsible for the proper plugging and abandonment.

The cost to plug a well can be prohibitively high for small operators. If the operators (who profited from the well) don’t plug it, the costs are externalized to states, and therefore, the public. For example, the state of California plugged two wells in the Echo Park neighborhood of Los Angeles at a cost of over $1 million. The costs are much higher in urban areas than, say, the farmland and oilfields of the Central Valley.

Since 1977, California has permanently sealed about 1,400 orphan wells at a cost of $29.5 million, according to reports by the Division of Oil, Gas, and Geothermal Resources (DOGGR). That’s an average cost of about $21,000 per well, not accounting for inflation. From 2002-2018, DOGGR plugged about 600 wells at a cost of $18.6 million; an average cost of about $31,000.

The map above shows the locations of idle wells in California. There are 29,515 wells listed as idle and 122,467 plugged or buried wells as of the most recent DOGGR data, downloaded 3/20/19. There are a total of 245,116 oil and gas wells in the state, including active, idle, new (permitted) or plugged.

Of the over 29,000 wells are listed as idle, only 3,088 (10.4%) reported production in 2018. Operators recovered 338,201 barrels of oil and 178,871 cubic feet of gas from them in 2018. Operators injected 1,550,436,085 gallons of water/steam into idle injection wells in 2018, and 137,908,884 cubic feet of gas.

The tables below (Tables 1-3) provide the rankings for idle well counts by operator, oil field, and county (respectively). Chevron, Aera, Shell, and California Resources Corporation have the most idle wells. The majority of the Chevron idle wells are located in the Midway Sunset Field. Well over half of all idle wells are located in Kern County.

Table 1. Idle Well Counts by Operator

Operator Name

Idle Well Count

1

Chevron U.S.A. Inc.

6,292

2

Aera Energy LLC

5,811

3

California Resources Production Corporation

3,708

4

California Resources Elk Hills, LLC

2,016

5

Berry Petroleum Company, LLC

1,129

6

E & B Natural Resources Management Corporation

991

7

Sentinel Peak Resources California LLC

842

8

HVI Cat Canyon, Inc.

534

9

Seneca Resources Company, LLC

349

10

Crimson Resource Management Corp.

333

Table 2. Idle Well Counts by Oil Field

Oil Field

Count by Field

1

Midway-Sunset

5,333

2

Unspecified

2,385

3

Kern River

2,217

4

Belridge, South

2,075

5

Coalinga

1,729

6

Elk Hills

958

7

Buena Vista

887

8

Lost Hills

731

9

Cymric

721

10

Cat Canyon

661

Table 3. Idle Well Counts by County

County

Count by County

1

Kern

17,276

2

Los Angeles

3,217

3

Fresno

2,296

4

Ventura

2,022

5

Santa Barbara

1,336

6

Orange

752

7

Monterey

399

8

Kings

212

9

San Luis Obispo

202

10

Sutter

191

Risks

According to the Western States Petroleum Association (WSPA) the count of idle wells in California has increased from just over 20,000 idle wells in 2015 to nearly 30,000 wells in 2018! That’s an increase of nearly 50% in just 3 years!

A U.S. EPA report on idle wells published in 2011 warned that existing monitoring requirements of idle wells in California was “not consistent with adequate protection” of underground sources of drinking water. Idle wells may have leaks and damage that go unnoticed for years, according to an assessment by the state Department of Conservation (DOC). The California Council on Science and Technology is actively researching this and many other issues associated with idle and orphaned wells. The published report will include policy recommendations considering the determined risks. The report will determine the following:

State liability for the plugging and abandoning of deserted and orphaned wells and decommissioning facilities attendant to such wells

Assessment of costs associated with plugging and abandoning deserted and orphaned wells and decommissioning facilities attendant to such wells