The majority of FracTracker’s posts are generally considered articles. These may include analysis around data, embedded maps, summaries of partner collaborations, highlights of a publication or project, guest posts, etc.

By Ted Auch, OH Program Coordinator, FracTracker Alliance

Anyone who has been paying attention to the domestic shale gas conversation knows the issue is fraught with controversy and political leanings. The debate is made only more complicated by the extensive lobbying to promote drilling and related activities. It would be nice to look at shale gas through a purely analytical lens, but it is impossible to decouple the role of politicians and those that fund their campaigns from the myriad socioeconomic, health, and environmental costs/benefits.

As such, this article covers two issues:

Who Gets Funded: the distribution of oil and gas (O&G) funds across the two primary parties in the US, as well as the limited funds awarded to third parties, and

Funding Allocation to a Specialized Committee: industry financing to the Committee on Science, Space and Technology1 the primary house committee responsible for:

…all matters relating to energy research, development, and demonstration projects therefor; commercial application of energy technology; Department of Energy research, development, and demonstration programs; Department of Energy laboratories; Department of Energy science activities; energy supply activities; nuclear, solar, and renewable energy, and other advanced energy technologies; uranium supply and enrichment, and Department of Energy waste management; fossil energy research and development; clean coal technology; energy conservation research and development, including building performance, alternate fuels, distributed power systems, and industrial process improvements; pipeline research, development, and demonstration projects; energy standards; other appropriate matters as referred by the Chairman; and relevant oversight.

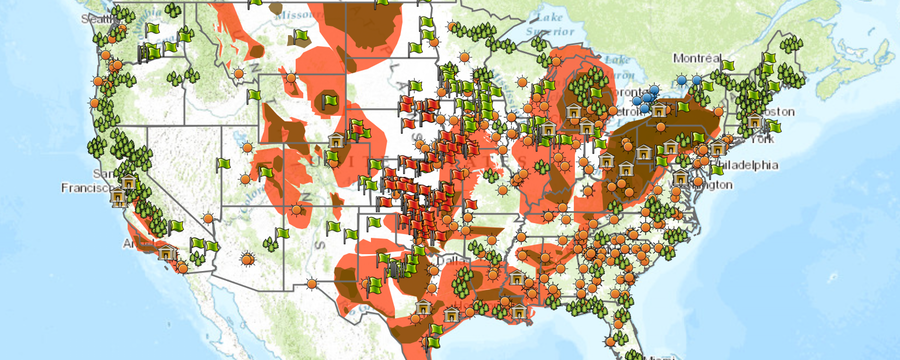

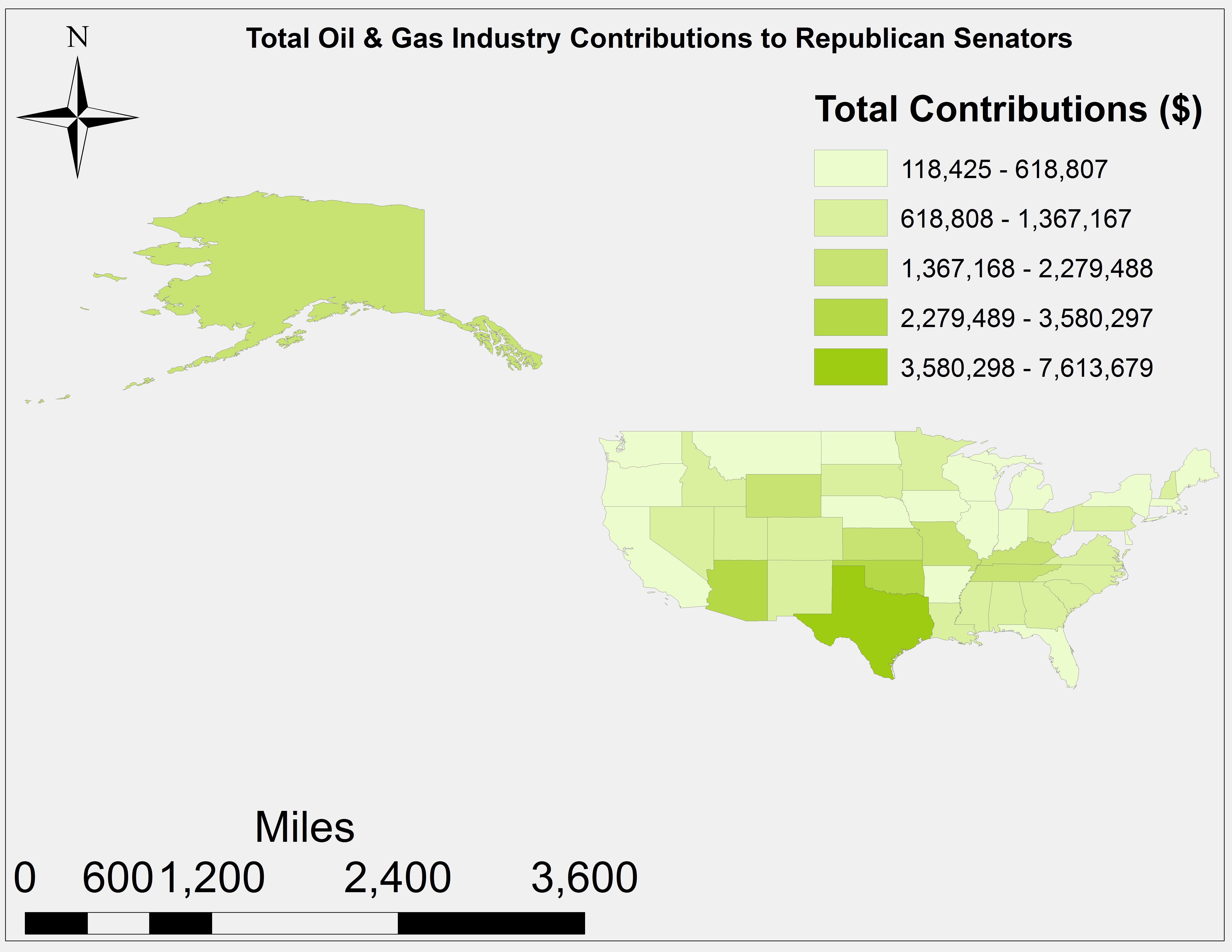

Fig. 1. Relevant Oil & Gas PACs, Institutes, and Think Tanks – as well as Koch Industries and subsidiaries offices (Orange). Click to explore

1. Letting the Numbers Speak

“When somebody says it’s not about the money, it’s about the money.”

The above quote has been attributed to a variety of sources from sports figures to economists, but nowhere is it more relevant than the politics of shale gas. The figures below present campaign financing from O&G industry to the men and women that represent us in Washington, DC.

Data Analysis Process

To follow the shale money path, FracTracker has analyzed data from the: a) total contributions and b) average per representative across Democrats and Republicans. Our Third Party analysis included five Independents in the Senate as well as one Green, one Unaffiliated, one Libertarian, and two Independents in the House.

Results

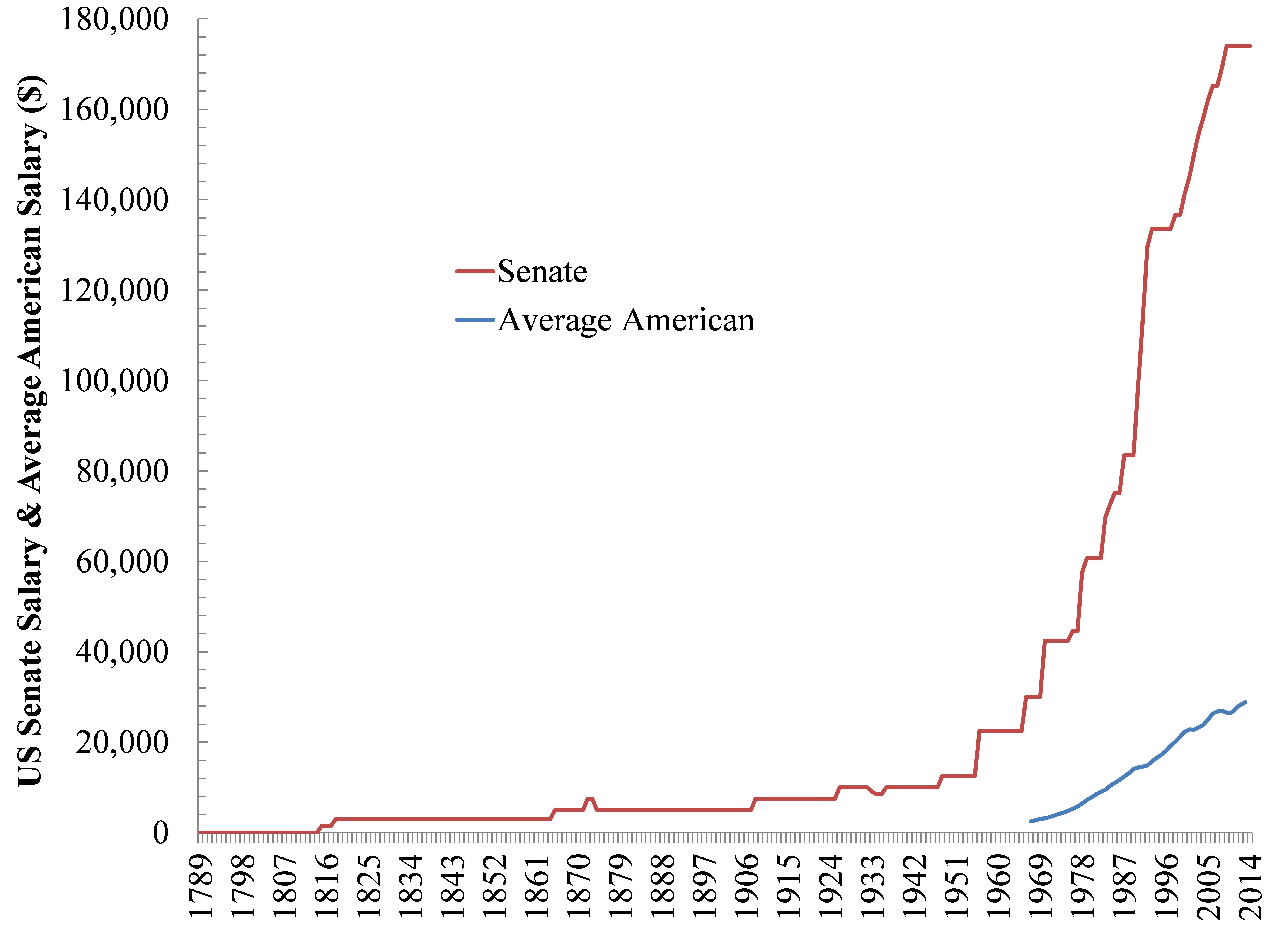

Fig. 3. US Senate Salary (Late 18th Century to 2014) & Average American Salary (1967-2013).

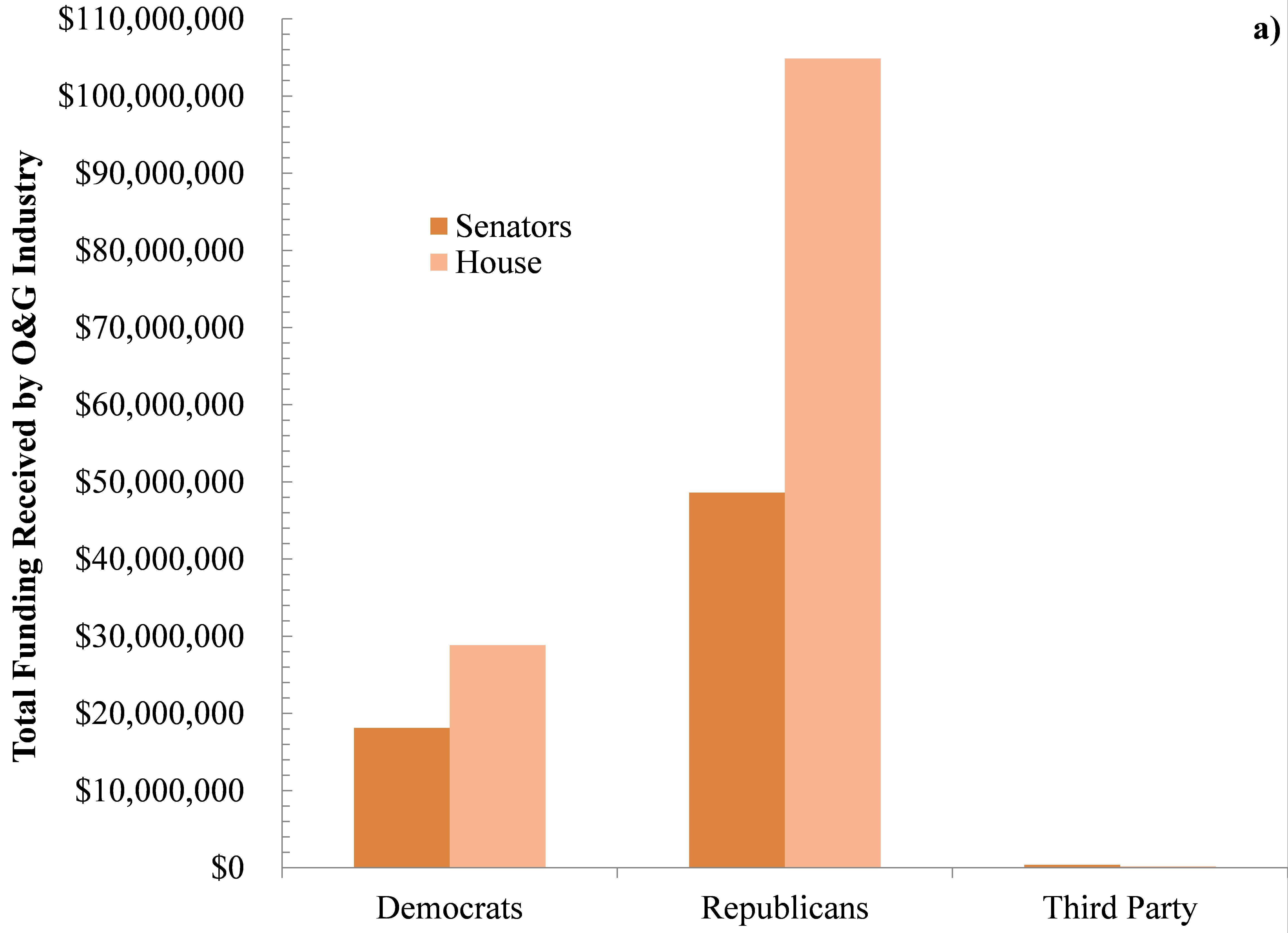

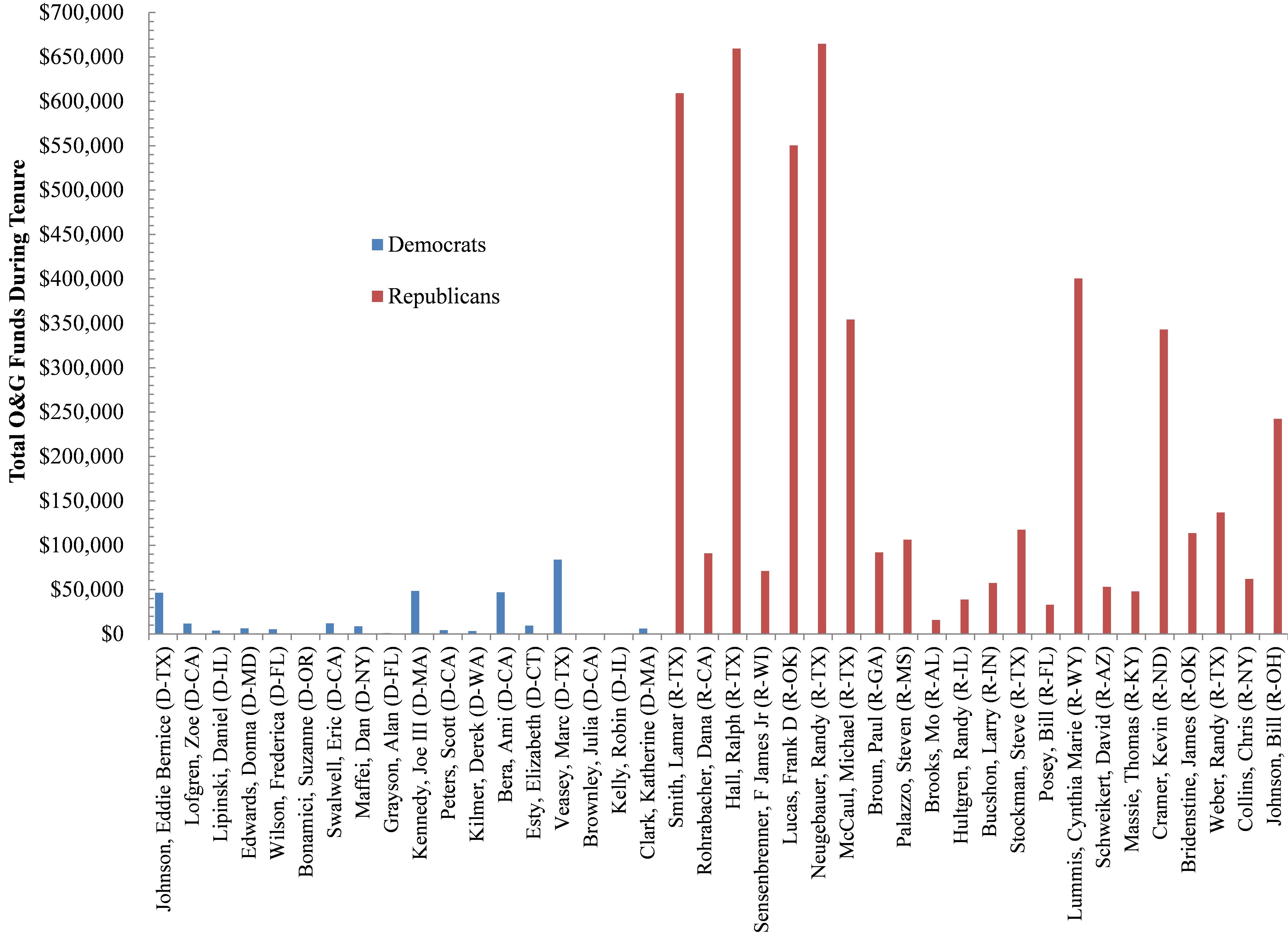

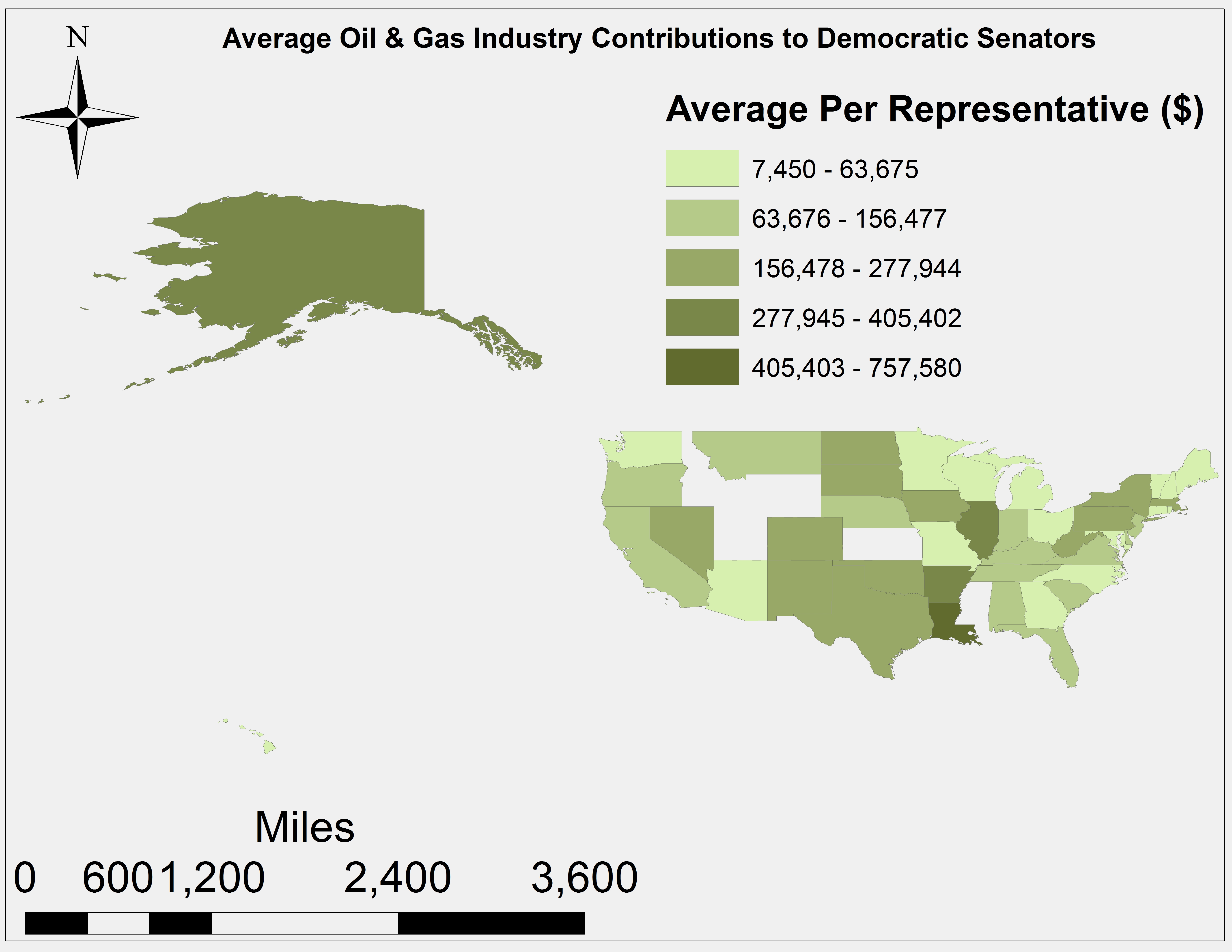

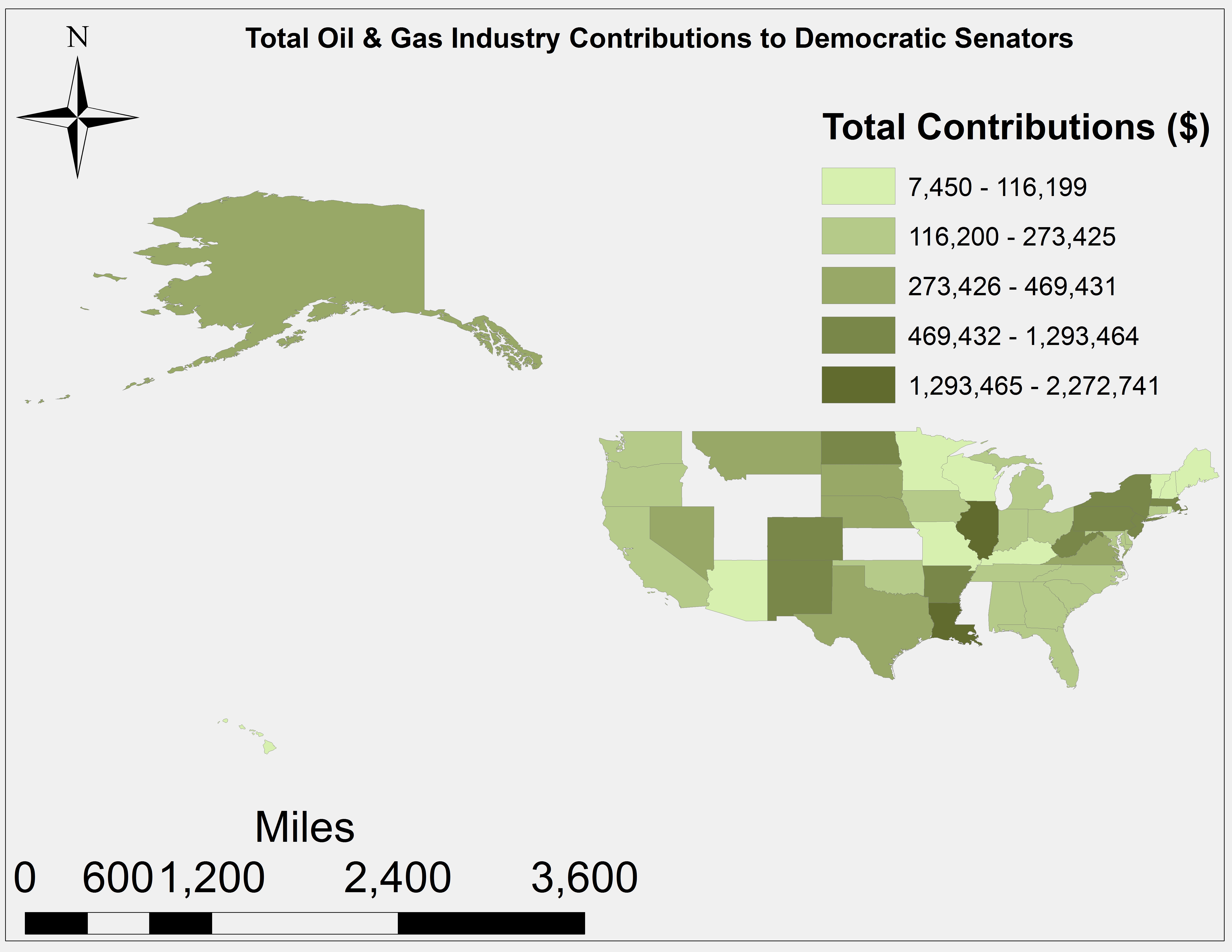

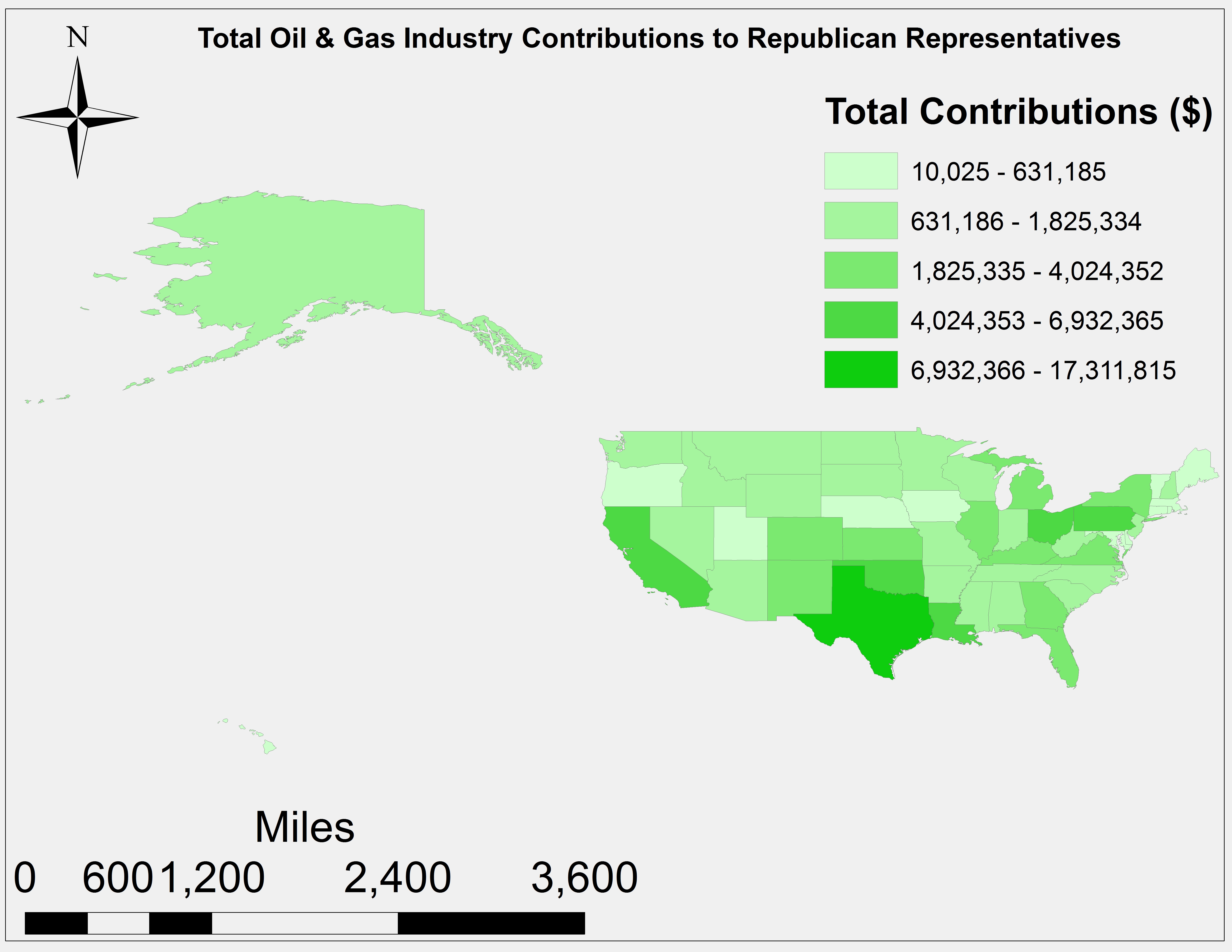

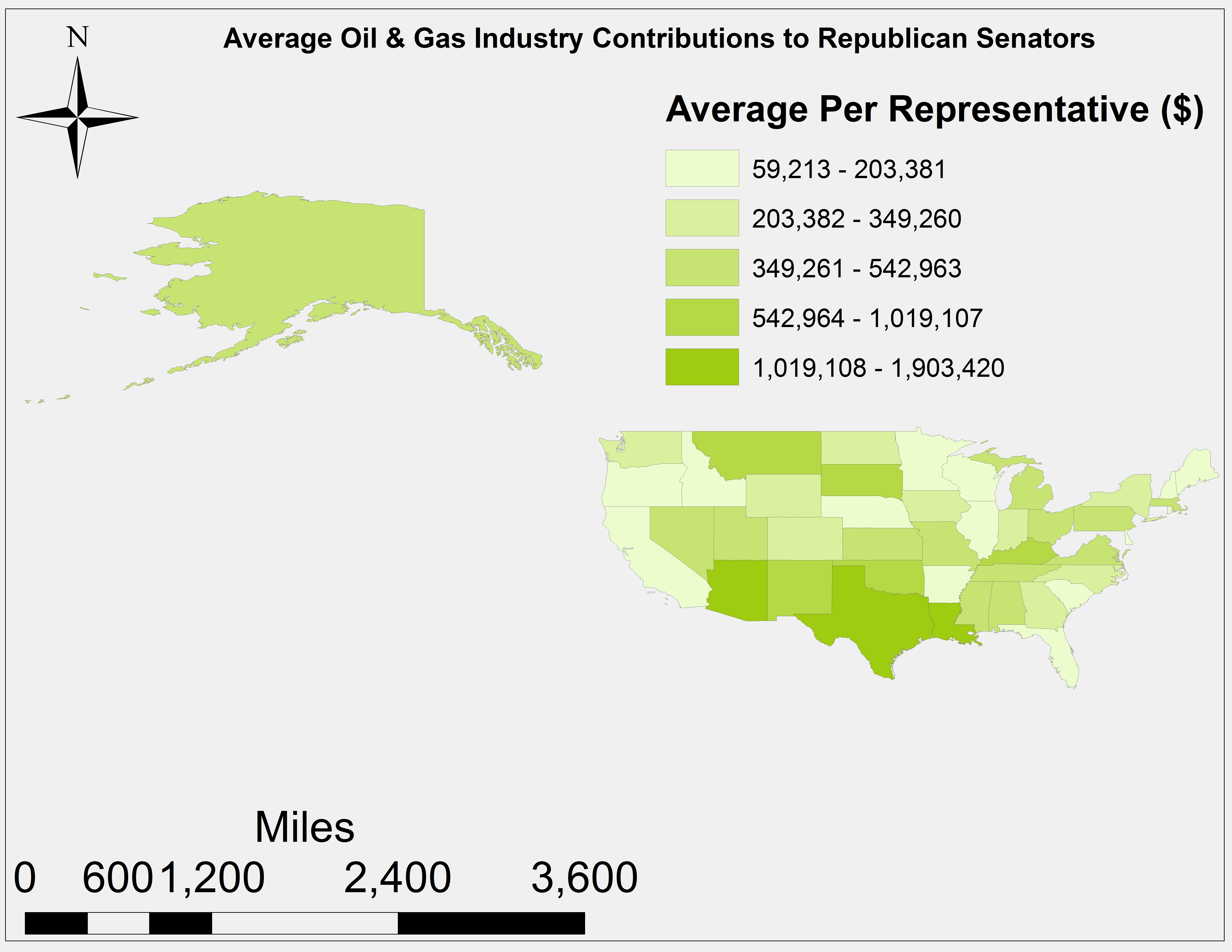

There are sizable inter-party differences across both branches of congress (See Figures 2a-b). In total, Democratic and Republican senators have received $18.1 and $48.6 million from the O&G industry since data collection began in 1990. Meanwhile, Third Party senators have received a total of $385,632 in O&G campaign finance. It stands to reason that the US House would receive more money in total than the senate, given that it contains 435 representatives to the Senate’s 100, and this is indeed the case; Democratic members of the House received $28.9 million to date vs. $104.9 million allocated to the House’ GOP members – or a 3.6 fold difference. Third Party members of the House have received the smallest allotment of O&G political largesse, coming in at $197,145 in total.

To put this into perspective, your average Democratic and Republican senator has seen the gap increase between his/her salary and the average American from $27,536 in 1967 to $145,171 in 2013 (Figure 3).

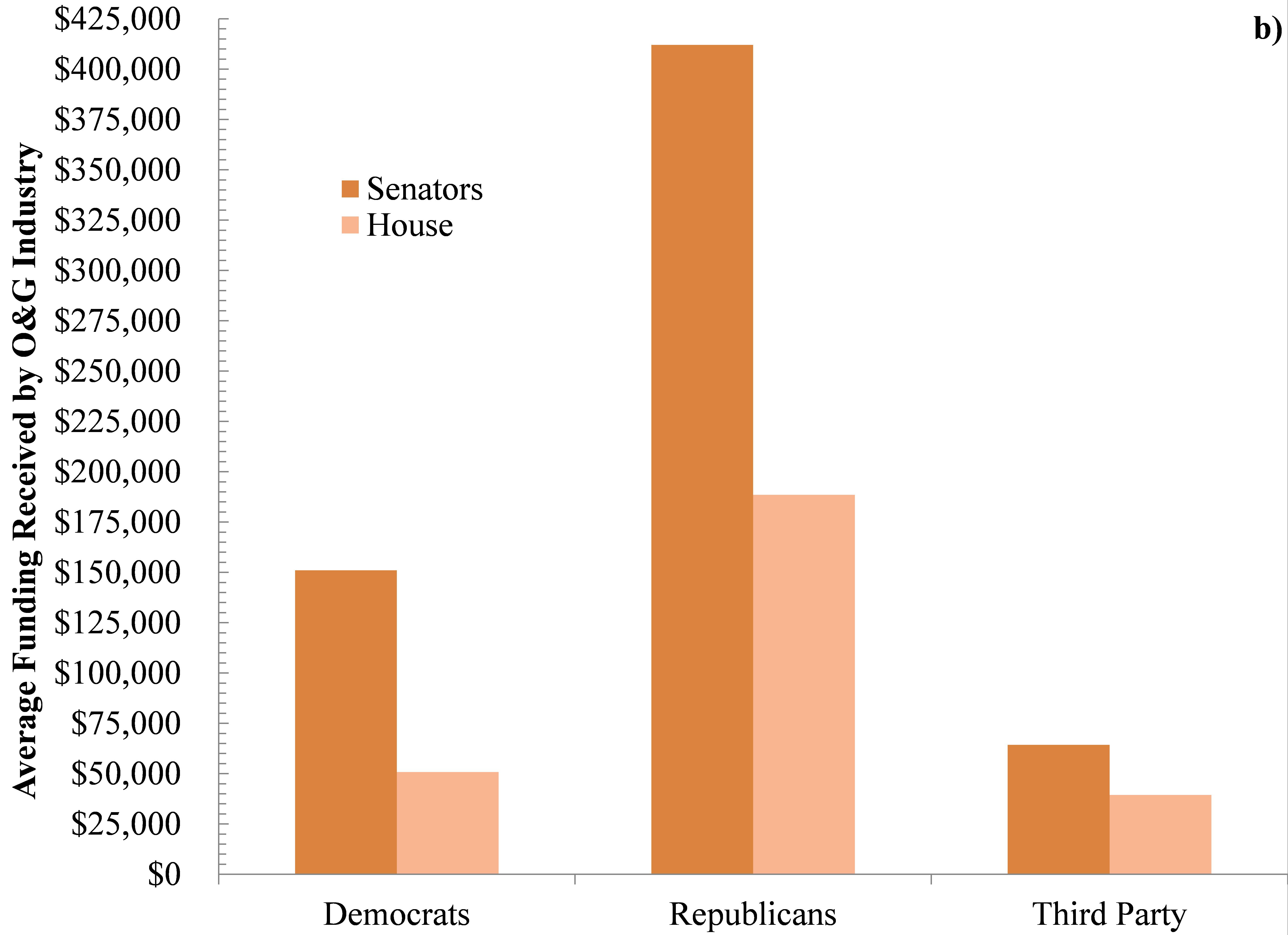

These same individuals have also seen their political war chests expand on average by $151,043 and $412,007, respectively. Third Party senators have seen their campaign funds swell by an average of $64,272 since 1990. Meanwhile, the U.S. Capitol’s Democratic and GOP south wing residents have seen their O&G campaign contributions increase by an average of $50,836 and $188,529, respectively, with even Third Partiers seeing a $38,429 spike in O&G generosity.

Figure 2a. Total funding received by both branches of the US legislative branch

Figure 2b. Average funding received by oil and gas industry

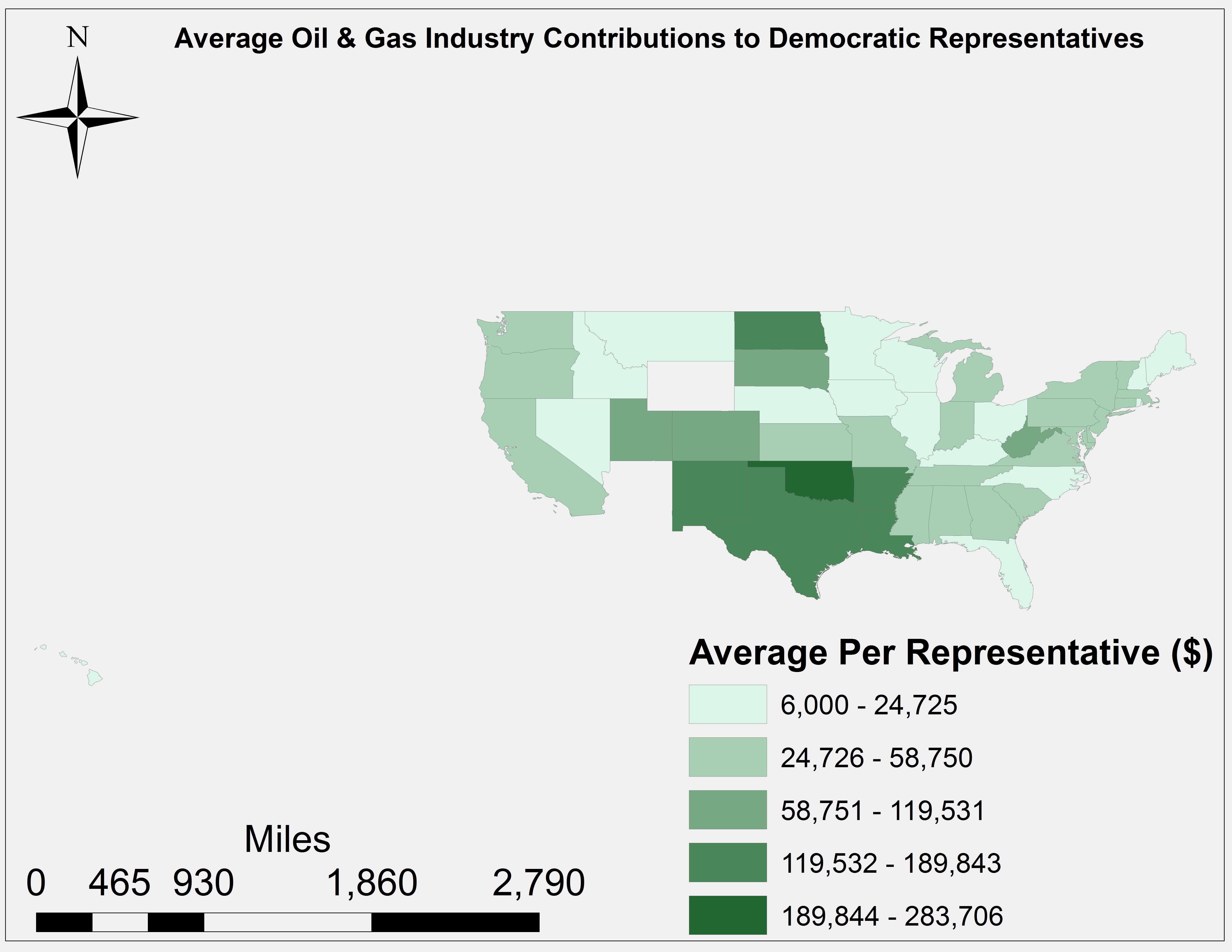

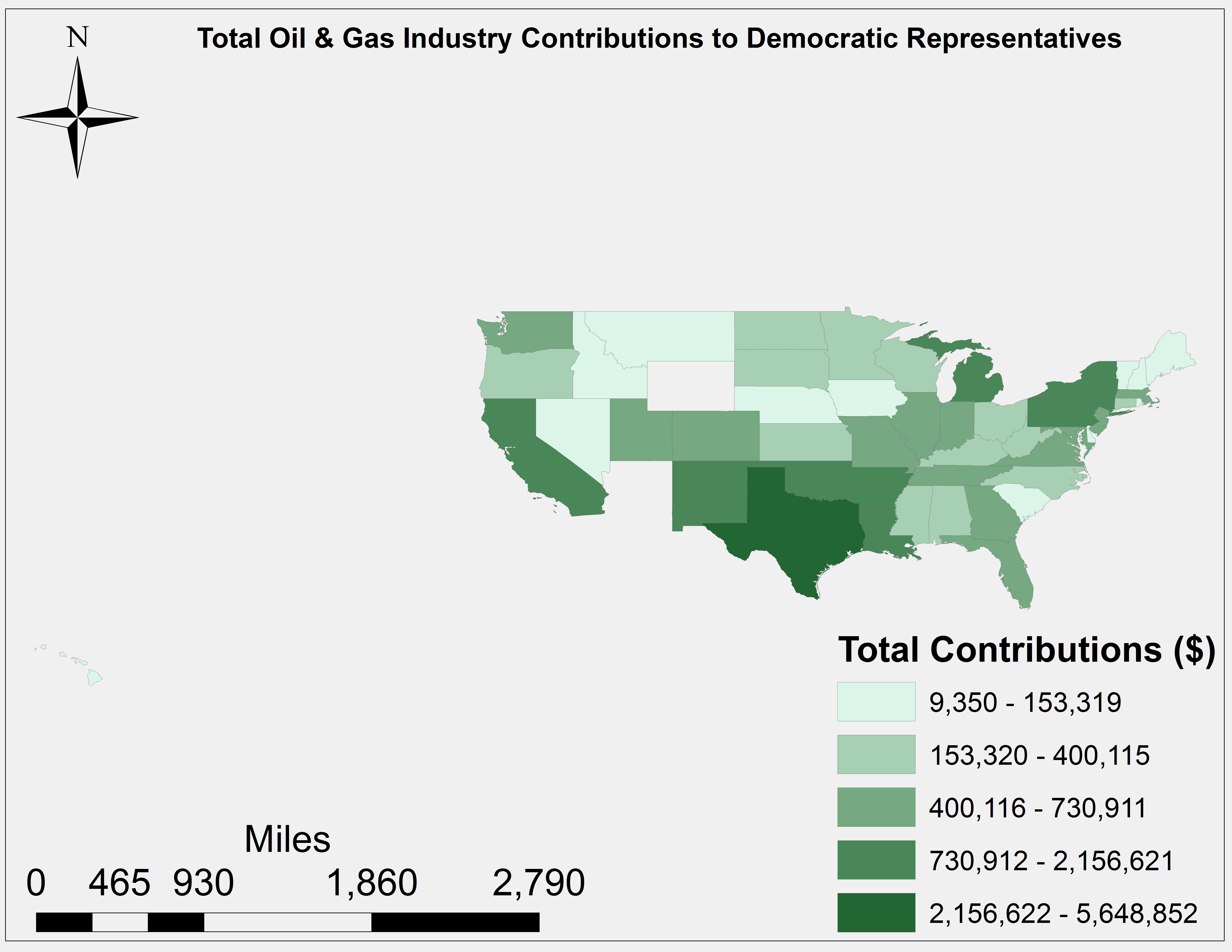

Location is a better predictor of whether a politician supports the O&G industry than his/her political affiliation. At the top of the O&G campaign financing league tables are extraction-intensive states such as Texas, Oklahoma, North Dakota, Alaska, California, and Louisiana. (See Figures 4a-h at the bottom of this article for Average Oil & Gas Contributions to US House Representatives and Senators across the US.)

2. Committee on Science, Space and Technology

The second portion of this post covers influences related to the Committee on Science, Space and Technology (CSST). There is no more powerful group in this country when it comes O&G policy construction and stewardship than CSST. The committee is currently made up of 22 Republicans and 18 Democrats from 21 states. Thirty-five percent of the committee hails from either California (6) or Texas (8), with Florida and Illinois each contributing three representatives to the committee. Almost all (94%) of the O&G campaign finance allocated to CSST has gone to its sitting GOP membership.

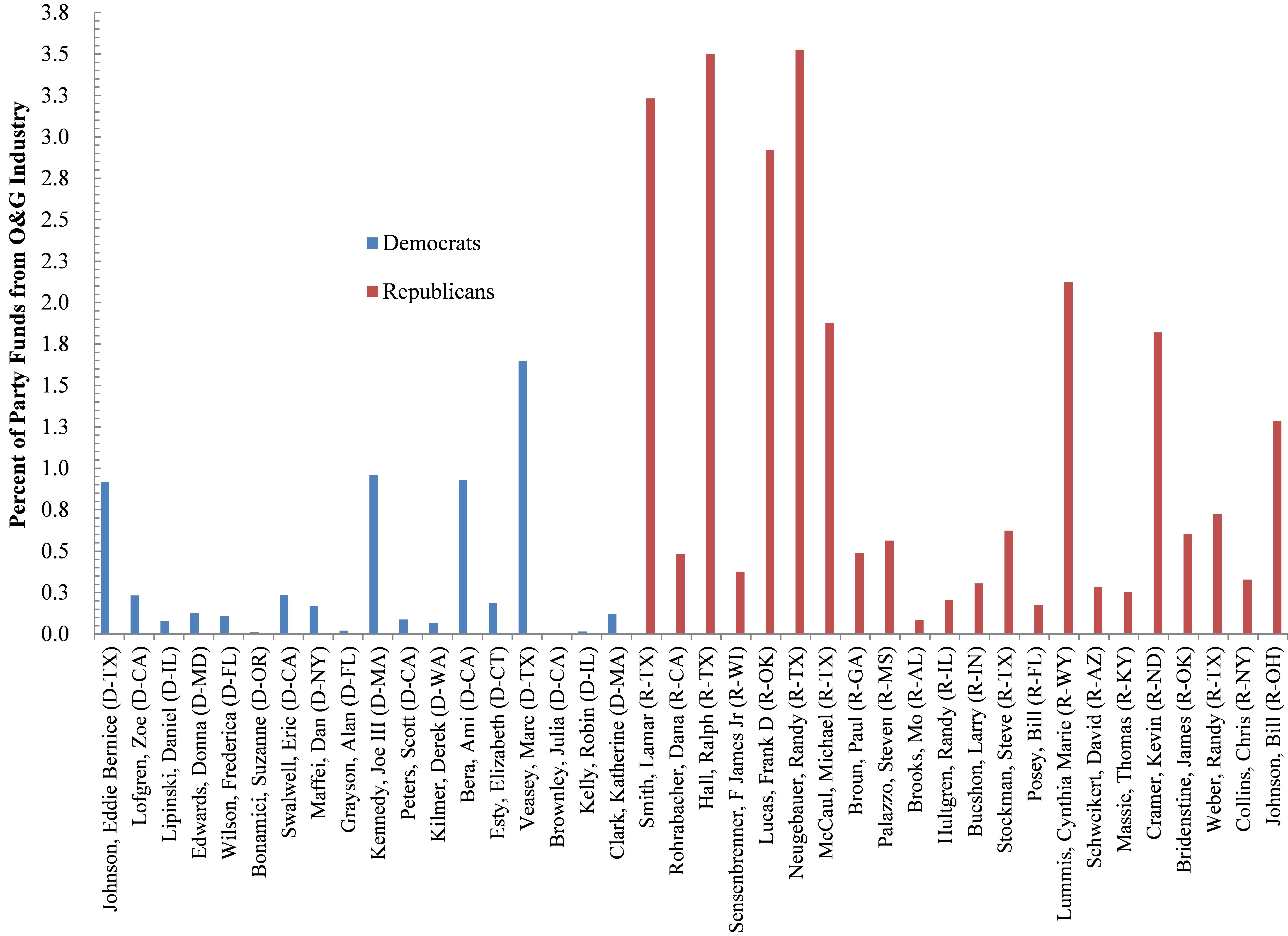

The top three recipients of O&G generosity are all from Texas, receiving 3.2-3.5 times more money than their party averages – totaling $1.93 million or 37% of the total committee O&G financial support. The next four most beholden members of the committee are Frank Lucas and Michael McCaul (TX, $904,709 combined), Cynthia Marie Lummis (WY, $400,400), and Kevin Cramer (ND, $343,000). The average Democratic member of the CSST committee has received 12.8 times less in O&G funding relative to their GOP counterparts; Dallas-Fort Worth Metroplex representatives Marc Veasey and Eddie Bernice Johnson collected a combined $130,350 from industry. Interestingly a member of political royalty, Joe Kennedy III, has collected nearly $50K from the O&G industry, which corresponds to the average for his House Democrat colleagues.

See Figures 5-6 for totals and percentage of party averages of O&G campaign funds contributed to current member of the US House CSST.

Figure 5. Totals

Figure 6. Percentage of party averages

“Don’t Confuse Me With The Facts”

In addition to current do-nothing politicians beholden to the O&G industry, we have prospects such as Republican U.S. Senate candidate Joni Ernst going so far as to declare that the Koch Brothers various Political Action Committees (PACs) started her trajectory in politics. Promising “ ‘to abolish’ the Environmental Protection Agency, she opposes the Clean Water Act, and in May she downplayed the role that human activities have played in climate change and/or rises in atmospheric CO2.

In Ohio it seems realistic to conjecture that OH Governor John Kasich, bracing for a tough reelection campaign, is wary of biting the PAC hands that feed him. He has also likely seen what happened to his “moderate” colleagues in states like Mississippi and Virginia, and in the age of Citizens United and McCutcheon he knows that the Hydrocarbon Industrial Complex will make him pay for anything that they construe as hostile to fossil fuel business as usual.

Close to the Action

Groups like the Koch-funded Americans for Prosperity, Randolph Foundation, and American Legislative Exchange Council (ALEC)2 are unapologetically wedded to continued production of fossil fuels. Nationally and in OH, politicians appear to be listening more to the talking points and white papers of such groups than they do their own constituents.. Therefore, it is no coincidence that DC and its surrounding Virginia suburbs has been colonized by industry mouthpieces, energy policy and economic academic tanks, philanthropies, and Political Action Committees (PACs). See Figure 1 for more information.

Know Your Vote

So when you go to the polls on November 4th, remember that politicians are increasingly beholden not to their constituents but to the larger donors to their campaigns. Nowhere is this more of a concern than US energy policy and our geopolitical linkages to producers and emerging markets. More to the point, when offered an opportunity to engage said officials make sure to bring up their financial links as it relates to how they vote and the types of legislation they write, massage, customize, or outright eliminate. As Plato once said, “The price of apathy towards public affairs is to be ruled by evil men.” Our current selection of politicians at the state and federal level are not evil, but data on O&G politics and campaign financing presented herein do indicate that objectivity with respect to oil and gas legislation has been at the very least compromised.

Figures 4a-h. Average & Total O&G Industry Contributions to US House Representatives and Senators across the US mainland and Alaska

By Mary Ellen Cassidy, Community Outreach Coordinator, FracTracker Alliance

After spending the afternoon travelling to drilling pads and compressor stations for the extraction and processing of unconventional oil and gas in our nearby communities, I travelled to the Niehaus Farm in the beautiful hills of West Virginia to visit with Rich and Felicia Niehaus. As the discussion centered on energy issues, it became evident that there is something crucial missing from the conversation about unconventional oil and gas issues:

energy conservation, energy efficiency, or renewable energy.

Conversations usually cover either fracking or energy conservation, efficiency, and renewables (ECER). It’s the exception for both to be covered in tandem even though they are the two sides of the same coin (Here, and here are examples of that exception). So, how did our conversation at the farm end up turning to ECER? Well, it turns out that this particular farm in West Virginia is entirely solar powered (photo above). Energy for the two barns and a beautiful home comes from rooftop panels installed in May of 2011. After finding funding and rebates to help with the upfront installation costs and participating in a renewable credits program, as of last year the Neihaus family spent $0.00 on utility bills. Their farm even generated a surplus of electricity, which they sold to the utility company as Solar Renewable Energy Credits – or SREC.

Solar farm tour in Cameron, WV

Reviewing the energy produced

Inside the barn

Discussing renewables with Rich

Perceived Barriers to Renewables

Why don’t more people follow this route? I only have anecdotal answers right now. When discussing fracking or unconventional oil and gas with folks, I ask why they haven’t considered solar as an energy source. Their responses vary but generally look like:

It never even entered my mind.

I’ve heard about solar and wind but heard they are really expensive.

No one sells or installs them around here.

Seems like a lot of work and expense.

Unlike the landman from the oil and gas company who calls or visits your home to talk to you about the benefits of selling your mineral rights for fracking or pipelines, no “sunman / windman / efficiencyman” calls or comes to your home to share the benefits of ECERs. There are few billboards or stories in our local or national media telling us how renewables can power the nation and keep the lights on. However, there are few or no print advertisements for solar, no polished TV ads on the clean energy of solar, wind or geothermal.

Basically, while coal, oil and gas are promoted – and receive generous federal incentives – at every turn or click, the benefits of ECER are truly missing from our conversation, locally and nationally.

Dependability

What if we decided to include the benefits of ECER in all of our conversations about fracking and fossilized sources of energy? Here are just a few items to keep in mind when sharing information that would move us to a more positive energy system future.

First, remember that coal, gas and, nuclear plants are highly intermittent over long time periods, such as their operating year or life span, requiring planned and unplanned maintenance and repair. An article in Cleantechnica tells us that as a result of this downtime, nuclear plants only generate electricity 83% of the time; combined cycle natural gas plants, 86% of the time; and coal plants, 88%. “Coupled renewable systems, like wind with solar tied to baseload power like hydropower, geothermal and solar thermal (with molten salt energy storage) are examples of reliable, dependable energy systems. Solar thermal plants are up and running 98% of the time; hydroelectric dams, 95%, and geothermal plants, 91%.1 According to a FracTracker analysis of Ohio wind potential:

If OH were to pursue the additional 900 MW public-private partnership wind proposals currently under review by the Ohio Power Siting Board (OPSB), an additional 900,000-1.2 million jobs, $1.3 billion in wages, $3.9 billion in sales, and $102.9 million in revenue would result. If the state were to exploit 10% more of the remaining wind capacity, the numbers would skyrocket into an additional 5.5-7.1 million jobs, $8.1 million in wages, $23.8 billion in sales, and $627.9 million in public revenues.

Enough Energy to Power a Nation

Sustainably harnessing enough power to fuel a nation requires conservation and efficiency. According to a recent analysis by the Lawrence Livermore National Laboratory, the US actually wastes 61-86% of the energy it produces. This figure is especially outrageous because the tools and technology needed to save a significant portion of this wasted energy are available right now and would easily fall under President Obama’s “shovel ready” label. For instance, in the past few years, net-zero buildings — those that produce as much (or more) clean energy on site as they use annually — have been gaining momentum. More than 400 such buildings are documented globally, with about one-fourth in the U.S. and Canada.

Knowing the considerable negative impacts of fracking, it is incomprehensible that a targeted national energy conservation and efficiency conversation has yet to take place, and that state policies promoting ECER like those in Ohio are actively being undercut. Energy conservation and efficiency, when coupled with renewables have the capability to power the nation.2

Gas – Nonrenewable, Finite, Declining

Unlike ECER, oil and natural gas are finite resources. Additionally, highly productive, economically recoverable shale wells have very high geological depletion rates and will become more difficult and more expensive to access.3 “The average flow from a shale gas well drops by ~50-75% in the first year, and up to 78% for oil”, said Pete Stark, senior research director at IHS Inc (a global information company with expertise in energy and economics). In neighboring Ohio, first-year oil and natural gas production declined by 84% (21-48 barrels of oil per day), with respective declines of 27% and 10% in subsequent years, while freshwater usage increases by 3.6 gallons per gallon of oil. Even the United States’ most productive Bakken shale requires 2,500 new wells per year to maintain 1 million BDD, while traditional fields in Iraq require a mere 60 new wells per year. ECERs, on the other hand, are renewable systems with decline rates calculated in the billions-of-years time frame.

Fossilized Energy – Costs Exceed Benefits

Often you will hear that fracking and fossilized energy are “cheap and affordable.” According to a report by Environment America, the reality is that externalized costs of fossilized energy, were they included on the balance sheet, would make gas, oil and coal costly and unaffordable. Alternatively, 53 Fortune 100 Companies report savings of $1.1 billion annually through energy efficiency and renewable energy.4

Some reports indicate that due to the nature of fossil fuel extraction compared to renewables, there are more jobs to be had in renewables.5 There is also the [significantly higher job, tax revenue, and income] multiplier effect associated with renewable energy technologies. The Union of Concerned Scientists reminds us that,

In addition to creating new jobs, increasing our use of renewable energy offers other important economic development benefits. Local governments collect property and income taxes and other payments from renewable energy project owners. These revenues can help support vital public services, especially in rural communities where projects are often located.

Along with externalized costs, natural gas also gets a preferred boost from our nation’s R&D funding compared to ECER research. This issue does not even include the de facto subsidies provided by our military escapades, which Joe Stiglitz and Linda Bilmes recently put at $3 trillion. In Scientific American’s article, Fracking Hammers Clean Energy Research, David Bello looked at the budget of the ARPA-E (Advanced Research Projects Agency-Energy) and found that five years in, “the gassy revolution was becoming apparent,” with funding going to natural gas research rather than ECER breakthroughs. Bello is of the opinion:

It is also exactly in times of overreliance on one energy source that funding into alternatives is not only necessary, but required. ARPA–E should continue to focus on transformational energy technologies that can be clean and cheap even if political pressures incline the still young and potentially vulnerable agency to look for a better gas tank.

Also, globally, the UN Environmental Program reports that the world spends six times as much money subsidizing fossilized energy as they do renewables. Despite having less government support, renewables have achieved record growth since 2000. The EIA reports that renewables are the fest-growing power source based on percentages, and in 2018 is estimated to rise to 25% of the global gross power generation. The EIA reports that, “On a percentage basis, renewables continue to be the fastest-growing power source… Globally, renewable generation is estimated to rise to 25% of gross power generation in 2018.” Germany alone generates 27% of its energy demand from renewables.

Climate Change – Sources & Solutions

Recent NOAA research suggests fugitive methane leaking from natural gas activity may be substantial, with leakage rates of 4-9% of the total production. This figure is significantly above the 2% recommended level for potential climate change benefits. Ken Caldeira, atmospheric scientist with the Carnegie Institution for Science recently noted:

We have to decide whether we are in the business of delaying bad outcomes or whether we are in the business of preventing bad outcomes. If we want to prevent bad climate outcomes, we should stop using the atmosphere as a waste dump. If we build these natural gas plants, we reduce incentives to build the near zero emission energy system we really need. It is time to start building the near zero emission energy system of the future. Expansion of natural gas is a delaying tactic, not a solution. A switch to natural gas would have zero effect on global temperatures by the year 2100.

Caldiera and Myhrvold’s paper on transitional energy concludes, “If you take 40 years to switch over entirely to natural gas, you won’t see any substantial decrease in global temperatures for up to 250 years [due to the CO2 inertia effect]. There’s almost no climate value in doing it.”

No Longer Missing

To make a short story long, that is what’s missing from the conversation – the great story of the benefits and solutions of ECER. How can we move towards a more positive and diversified energy future if we continue to bury the lead? The real solutions to our energy challenge cannot be relegated to a sidebar conversation. A disconnect between what is and what can be will keep us on the path to dire economic and public health impacts.

Back to the Niehaus farm…

As we were enjoying the fresh air, the pastoral beauty and soft sounds of nature that evening, I tried to picture what this landscape would look like, smell like, sound like, feel like, if instead of enjoying this farm fueled by solar, we were sitting back at one of the many homes bordering a drilling pad or processing facility that I had visited earlier in the day. I tried to envision what the wildlife, streams and skies would look like, what the children’s legacy would be, wondering if we were perhaps too distracted calculating costs instead of values.

When speaking of his investment in solar and his approach to life, Rich shares with us that he subscribes to the ancient Indian proverb, “We do not Inherit the Earth from our Ancestors; we Borrow it from our Children.”

After this “renewed” experience at the farm that evening, I reaffirmed my efforts to not miss any more opportunities to raise the profile of ECERs when people are debating the pros and cons of fracking and fossils. Energy Conservation, Efficiency and Renewables can no longer go missing from our conversations or we allow the myth to flourish that only fossils can “keep the lights on.” With ECERs in the conversation we may actually transition from this “transition fuel,” to a truly transformational future.

As Buckminster Fuller once said:

You never change things by fighting the existing reality. To change something, build a new model that makes the existing model obsolete.

Additional References

To learn more, go to the Rocky Mountain Institute website.

A report by WWF, Ceres, Calvert Investments and David Gardiner and Associates finds that

Addressing the issue of job creation, the Union of Concerned Scientists reports, “Compared with fossil fuel technologies, which are typically mechanized and capital intensive, the renewable energy industry is more labor-intensive. This means that, on average, more jobs are created for each unit of electricity generated from renewable sources than from fossil fuels.”

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2014/10/Solar-Panels-Feature.png400900FracTracker Alliancehttps://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngFracTracker Alliance2014-10-06 12:21:042020-07-21 10:42:46Missing from the Conversation

Sometimes we all need to be more patient. Enforcement of environmental regulations against a corporation rarely happens, and environmental enforcement against an oil and gas corporation is truly an amazing rarity. These do not come our way with any degree of frequency. However, here is one where an operator was finally fined – and in West Virginia.

The enforcement and fine in Tyler County, WV is especially amazing since it follows just weeks after the Trans Energy guilty pleas and fines totaling $600,000 for three violations of the Clean Water Act in Marshall County, WV.

On October 5, 2014, Jay-Bee Oil and Gas Company was fined $240,000

for violations at its Lisby Pad in Tyler County, WV.

Now, finally, after about a year and a half of deplorable operating conditions on one of the worse (readily visible) well pads that we have seen in years, some enforcement action has finally happened.

Findings of Fact

Jay-Bee Oil & Gas, Inc. owns and operates natural gas well sites known as Lisby / TI-03, RPT8, RPT5, Coffman, W701, TI213, McIntyre, and Hurley, which are located in West Virginia. Here is the timeline for inspections and complaints related to this site:

March 28, 2014 – Personnel from the Division of Air Quality (DAQ) conducted an inspection at the Lisby / TI-03 Well Pad in response to a citizen odor complaint.

April 1, 2014 – Personnel from the DAQ conducted a follow-up inspection at the Lisby 1 T1-03 Well Pad. Visible emissions were observed from the permanent production storage tanks.

April 17, 2014 – Personnel from the DAQ conducted a follow-up inspection at the Lisby 1 TI-03 well pad in response to additional citizen odor complaints

July 18, 2014 – In response to a citizen complaint, personnel from the DAQ conducted an inspection at the Lisby 1 T1-03 Well Pad. Objectionable odors and visible emissions were observed from the thief hatch of one of the permanent production storage tanks. A visible liquid leak was also observed on a pipe located at the tank nearest to the vapor recovery unit.

September 30, 2014 – Jay-Bee Oil and Gas Company agrees to pay a total civil administrative penalty of two hundred forty thousand dollars ($240,000) to resolve the violations described in this Order (PDF).

Of Note

This enforcement action was not done by the WVDEP Office of Oil & Gas, who seem to only politely try to encourage the drillers to somewhat improve their behavior. The WVDEP Department of Air Quality issued this Notice of Violation and enforcement.

Most of this air quality enforcement process started because of the continued, asphyxiating, toxic gas fumes that poured off the Jay-Bee Lisby pad for months. The residents were forced to move away and have not returned due to lack of confidence that it is safe to live in this area yet. These residents join the growing ranks of others, who are now referred to as Marcellus refugees.

Inadequate vapor recovery system lead to residue forming on tank from escaping fumes

Additional Resources

Below are links to some of the newspaper articles on the same mismanaged well pad:

I regularly visit the Jay Bee Lisby pad on Big Run in Tyler County, WV. Given its significant and continuing problems over the past year, and also due to the total absence of any environmental enforcement, it is important to give all those JB well pads extra attention. In fact, I happened upon a few new issues during my recent visits and site inspections on Sept. 11, 2014 and again on Oct. 1st.

There seems to be an effort by Jay-Bee to literally bury their evidence in a ditch along their poorly constructed well pad. New dirt has recently been put into the low area along the jersey barriers (photo above). It appears that they are trying now to build some type of well pad, whereas most drillers usually build a proper well pad before they drill the wells.

An additional issue is the orange fluid pouring out of the well pad (photos below). While I have conducted my own sampling of this contaminant, regulatory sampling should be conducted soon to find out the nature of this fluid and its source from the Jay Bee Lisby pad.

Orange Liquid Seeping from Lisby Pad

Orange Liquid Close Up

Given the many spills at this pad, this issue is not surprising. However, we still need to find out what this is, as it will not be going away on its own. JB should not be allowed to bury its evidence before they are required to test and reclaim the whole area.

Please keep in mind that the law might allow a driller to force a well pad on a land owner to recover the gas, and to also locate it next to a stream, but it does not give them the right to contaminate and pollute private property – which has been done here numerous times.

Readings from conductivity meter

When I sampled the fluid from the puddle below the orange stream and tested its conductivity, the meter read ~2.34 millisiemens – or 2340 microsiemens (photo right).

The orange fluid continues to flow under the fence and beyond their limits of disturbance. However, given the wide area covered in sludge after the January explosion, it is hard to say where their limits of disturbance actually stop.

By Bill Hughes, WV Community Liaison, FracTracker Alliance

Read more Field Diary articles here.

The following correspondence comes to FracTracker from a community member in West Virginia. It highlights in a very personal way the day-to-day nuisances of living with intense drilling activity nearby.

This Is Home

The 170-plus acre parcel of land where we live and farm has been in our family for over 50 years. I have worked on our road that comes into our property for 40 of those years. I know what the road should look like and have put a lot of personal work into maintaining it over the years (like most folks do who live on many of these smaller roads, even though they are a legal State right-of-way). We have been experiencing a lot of problems here due to the exploration and production of the natural gas resources. We would like to see major improvement really soon.

In all my years I have never seen this amount of dust or this amount of mud and slop after a small rainfall, of all of the loose gravel that makes traction near impossible. And I have never before been blocked and delayed or stopped on my road, and my wife has never been as upset, concerned and fearful and agitated about driving down our lane because of all the big trucks and rude drivers.

I have tried to work with the gas companies and their subcontractors for some years. My Mom and I have a separate property nearby where another well pad is located. I have recently allowed a new gas pipeline to be put through my farmland. I have tried to be patient and tolerant and easy going for the past three years. However, like some neighbors on nearby roads have found out, that doesn’t always work. Some of the hundreds of drivers and employees are courteous, polite, and respectful and yield the road when we are traveling. Some others are downright rude and disrespectful. They must not live around here, and it is obvious they do not care at all about the local residents.

Dirt and Mud

Clumps of mud that employees of a construction and excavating company dragged off of the well pad

We will give you some examples of the problems from our viewpoint. Let’s start with dirt, mud, and dust since those have been an on-going problem since the pipeline guys started here over 6 months ago. See photos right.

Surely they knew that it was likely to happen and they knew it did happen. They left the mud on our road. The construction employees drove by and watched a neighbor pick up and carry the mud to the side of the road.

This was not a one-time occurrence. This has happened every time this summer when we had rain. Our lane has been treated like it was a private lease road. So far it seems that our WV DOH (West Virginia Division of Highways) has been ineffective in improving the situation.

Another mud tracking issue

For the most part when companies are moving dirt they seem to do a good job. All we ask is that they keep their mud on their property and off our road.

I have never before seen big mud blobs like the one to the right on our road. It is unnecessary, uncalled for and avoidable. Seeing these frequently is a visible sign that at hardly any of the industry cares about the neighbors near here. I was given some of the Engineering Plans for the well pad and its access road. It spells out that the contractor is responsible to never drag mud out onto the public road. And what to do if it happens.

I recently reviewed some well pad construction plans. To paraphrase, the plans say don’t make a mess in public, but if and when you do clean up after yourself. Sounds like stuff that was covered in Kindergarten, doesn’t it? It promotes good policy and it keeps peace in the neighborhood.

Dust Storms

The next example of another problem that we should not have to live with, occurs when all of that mud on our road dries out. DUST, as can be seen in the next three pictures, is a very common occurrence.

Guests were visiting here recently and had to follow a dust storm down the road. The trucker probable never saw her car. He probably could not see anything behind him.

Trucks

More Trucks

Means Lots of Dust

Broken Phone Lines

Another problem that has happened over and over has been has been all the times that contractors have broken our phone line. It seemed that no one ever thought to call the 800 phone number to have utilities marked. In addition, after they were marked, no one paid any attention to where the flags were. This is a very basic task, but it seems to be beyond what some of the contractors could figure out and do. See photos below. Note the broken and temporary splice in my phone line that looks like a dozer operator did it. The phone line was then lying on the top of the gravel road.

The photos below show our phone line after it was again dug up and broken last week. Even with the phone company markers to tell the operators exactly where the line was, they dug into it. Someone is not paying attention.

By the way, we do not own or use a cell phone, so being able to depend on a working landline is important to us. We could understand this incident happening one time, but not more often than that.

Construction Equipment on Public Roadway

Construction equipment on the road

We appreciate that a few weeks ago the construction contractor put some small gravel on the top part of the roadway near the well pad entrance. However we are not sure how long that gravel will last because of all the dirt that has been dropped on it, but mainly because of all the heavy construction equipment that has been running on the public road every day.

The gravel is being pulverized daily and contributes to the dust problem. Also a large pile of loose gravel and big rock is now spread out on the roadway at the sharp right, uphill turn past the compressor station entrance. This makes it difficult for smaller vehicles to get any traction. Well pad guys all drive bigger 4-wheel drive trucks, so it doesn’t seem to matter to them. But my family drives smaller cars.

A neighbor was again walking the road last week picking up clumps of mud and large rock to get them off the road.

Also, we have been told that all this construction equipment is not supposed to be using the state right-of-way anyway, at any time. Are these off road construction pieces of equipment insured, and registered and licensed to be used on a public roadway?

Blocked Roads

Roadblock on Turkey Run, WV

Another frequent problem is having our roads blocked many times causing many delays.

On Election Day my wife went to get my mom to take her to vote and had to wait on yet another truck blocking the road. These truckers seem to always think they always have the right of way, the right to block our roads, and the right to stop residential traffic at any time for their convenience. Last week a flagger stopped me just to allow construction employees to exit the well pad. Good neighbors would not do that. The truck to the right had the road completely closed for over an hour, with a track hoe behind it being used to unload the pipe. There is enough land around here to get these trucks off our road when unloading them. Even our local loggers know to do that.

Being a Better Neighbor

All of these problems are nothing new to other residents here in Wetzel County. My friends in the Silver Hill area have complained about the same type of problems for years, and eventually the operator there finally figured out how to be a better neighbor.

With all the problems in many other areas by multiple companies, one would think that by now the gas drillers and all their many subcontractors would have come up with a set of what works and what doesn’t. I think they are called best practices. We should not have to continually keep doing the same inconsiderate things all over again at each well pad site in every area. It is possible to learn from mistakes made elsewhere. We should be looking for constant improvements in our operations, as these issues are more than an inconvenience.

This article is one of many in our Community Insights section. Learn more>

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2014/08/TruckBlog.png400900FracTracker Alliancehttps://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngFracTracker Alliance2014-09-25 10:09:172020-07-21 10:42:45More than an Inconvenience

We recently received a request for unconventional (fracking) drilling data in Southwestern Pennsylvania counties and municipalities. Specifically, the resident wanted to know the following information:

Number of drilled wells in Southwestern PA counties, and in each municipality,

How many wells are producing natural gas in each municipality, and

The number of well violations reported there.

The following counties in Southwestern PA were studied (based on available electronic data): Allegheny, Armstrong, Beaver, Butler, Cambria, Fayette, Greene, Indiana, Somerset, Washington, and Westmoreland.

The well production data was compiled from a production report found on the Pennsylvania DEP Office of Oil and Gas website. This report detailed production values from unconventional gas wells statewide from January 2014 – June 2014. The well violation data was compiled using the Pennsylvania DEP Office of Oil and Gas’s interactive Oil and Gas Compliance report. From here, a compliance report was created using the following criteria: All PA regions, counties, and municipalities, all well operators, unconventional wells only, and wells inspected from 1/1/2000 – 9/9/2014.

Drilling Data Trends

Once all of the data was compiled, we created a spreadsheet that included a ratio of violations/wells for each municipality and county. Below are a few observations that stood out to us, followed by possible explanations for what has been reported.

Slightly less than 1/3 of all wells drilled in the 11 counties selected for this analysis have committed some sort of violation (.31).

The ratio of violations to wells drilled in Somerset County is 1.38, by far the largest ratio discovered. This means than more than one violation has been cited for every well drilled in that area, but that does not mean that every well carries with it a violation. The second largest ratio would be Cambria County at 1.00.

If you break down the numbers and look at municipality trends, the largest violation/wells ratio by municipality is found in Stewart Township, Fayette County (9.00). There have been 18 reported violations in association with the 2 wells drilled in the area.

Of the 60 municipalities that recorded no violations, South Buffalo Township in Armstrong County has the most wells drilled with 20.

Across the 11 counties studied, Allegheny County has the lowest ratio of violation/wells (.007).

Violations were reported in Somerset Township, Somerset County. No wells were drilled in this area, however.

Violations were reported in Wayne Township, Greene County, yet no wells were reported to be drilled in the municipality.

Explaining Some Data Caveats

Why is Allegheny County seeing such a low violation/well ratio?

Across the 11 counties studied, Allegheny County has the lowest ratio of violation/wells (.007).

Allegheny is the most populated county studied in Southwestern PA. Oil and gas drillers in the county, therefore, have the largest audience watching them. This may be encouraging the drillers to be more cautious or follow rules and regulations more strictly. Another possible explanation is that inspectors may be more lenient when reporting violations in in Allegheny County. Additionally, drillers operating primarily in Allegheny County may be are more likely to or are more capable of drilling according to the regulations. A final possibility is that Allegheny County is one of the last counties in this region to be heavily drilled, perhaps allowing for more best practices to be implemented on site compared to well pads established early on.

Violations With No Wells?

Violations were reported in Somerset Township, Somerset County. No wells were drilled in this area, however. These violations could have occurred when constructing the well pad. If construction has stopped at this site since the violation, there would not have been any wells drilled. Additionally, there may be an error in the dataset as to the actual location (e.g. county) of the well pad.

Violations were reported in Wayne Township, Greene County, yet no wells were reported to be drilled in the municipality. The PA DEP has informed FracTracker that these violations were actually reported for a well pad located in Center Township, Greene County. The entry for Wayne Township was a recording error on their part. Our data has been updated to reflect the proper number of violations reported in Center Township, as well as the removal of any activity in Wayne Township.

Download the Spreadsheet

The spreadsheet we supplied to this resident can be downloaded as a compliance report.

Updated PA Map

Explore our map of PA unconventional wells and violations by clicking on the map below:

Last updated: September 19, 2014

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2014/09/SWPA-Map.png400900FracTracker Alliancehttps://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngFracTracker Alliance2014-09-22 16:06:592020-07-21 10:42:45Comparing Unconventional Drilling in Southwestern PA

By Karen Edelstein, NY Program Coordinator, FracTracker Alliance

Since 2011, North Dakota crude oil from the Bakken Shale Play has made its way to refineries on the east coast via freight trains. This means of oil transportation is becoming increasingly common, as plans for pipeline development have been falling short, but demand for more energy development continues to climb (see New York Times, April 12 , 2014). In addition to the Bakken crude, there are also currently proposals under consideration to ship crude by rail from Alberta’s tar sands region, along these same routes through New York State.

Alarm about the danger of these “bomb trains” came sharply into public focus after the disaster in Lac Mégantic, Québec in July 2013 when a train carrying 72 carloads of the highly volatile Bakken oil derailed, setting off a massive series of explosions that leveled several blocks of the small town, killing 47 people (photo above). The crude from the Bakken is considerably lighter than that of other oil and gas deposits, making it more volatile than the crude that has been traditionally transported by rail.

Quantifying the Risk

As estimated by the National Transportation Safety Board, with deliveries at about 400,000 barrels a day headed to the Atlantic coast, about a 20-25% of this volume passes through the Port of Albany, NY. There were recent approvals for 3 billion gallons to be processed through Albany. The remainder of the crude is delivered to other ports in the US and Canada. Any oil travelling by rail through the Port of Albany would also pass through significant population centers, including Buffalo, Rochester, and Syracuse, NY. Binghamton, NY is also bisected by commercial rail lines.

In the past year, the New York Times, as well as other media, have reported on the threat of disasters similar to what occurred in Québec last summer, as the freight cars pass through Albany. Not only is the oil itself volatile, safety oversight is extremely spotty. According to The Innovation Trail, “… a 2013 report from the Government Accountability Office noted that the Federal Railroad Administration only examines 1-percent of the countries rail road infrastructure.”

RiverKeeper, in their recent report on the topic, notes:

Nationwide, shipping crude oil by rail has jumped six-fold since 2011, according to American Association of Railroads data, and rail shipments from the Bakken region have jumped exponentially since 2009.

This ad-hoc transportation system has repeatedly failed — and spectacularly.

The fires resulting from derailments of Bakken crude oil trains have caused fireballs and have burned so hot that emergency responders often can do nothing but wait—for days—to let the fires burn themselves out.

The Guardian has reported that a legacy of poor regulation and safety failures led to the disaster in Québec, leading to bankruptcy of Montreal, Maine & Atlantic Railways (MMA), and numerous class action suits. Records show that MMA was particularly lax in maintaining their rail cars and providing training for their employees. Meanwhile, in the US, critics of rail transport of volatile crude oil point to inadequate monitoring systems, training, and, importantly, prepared and available emergency response teams that would be able to respond to explosions or disasters anywhere along the route. The size of a explosion that could occur would easily overwhelm volunteer fire and EMT services in many small towns.

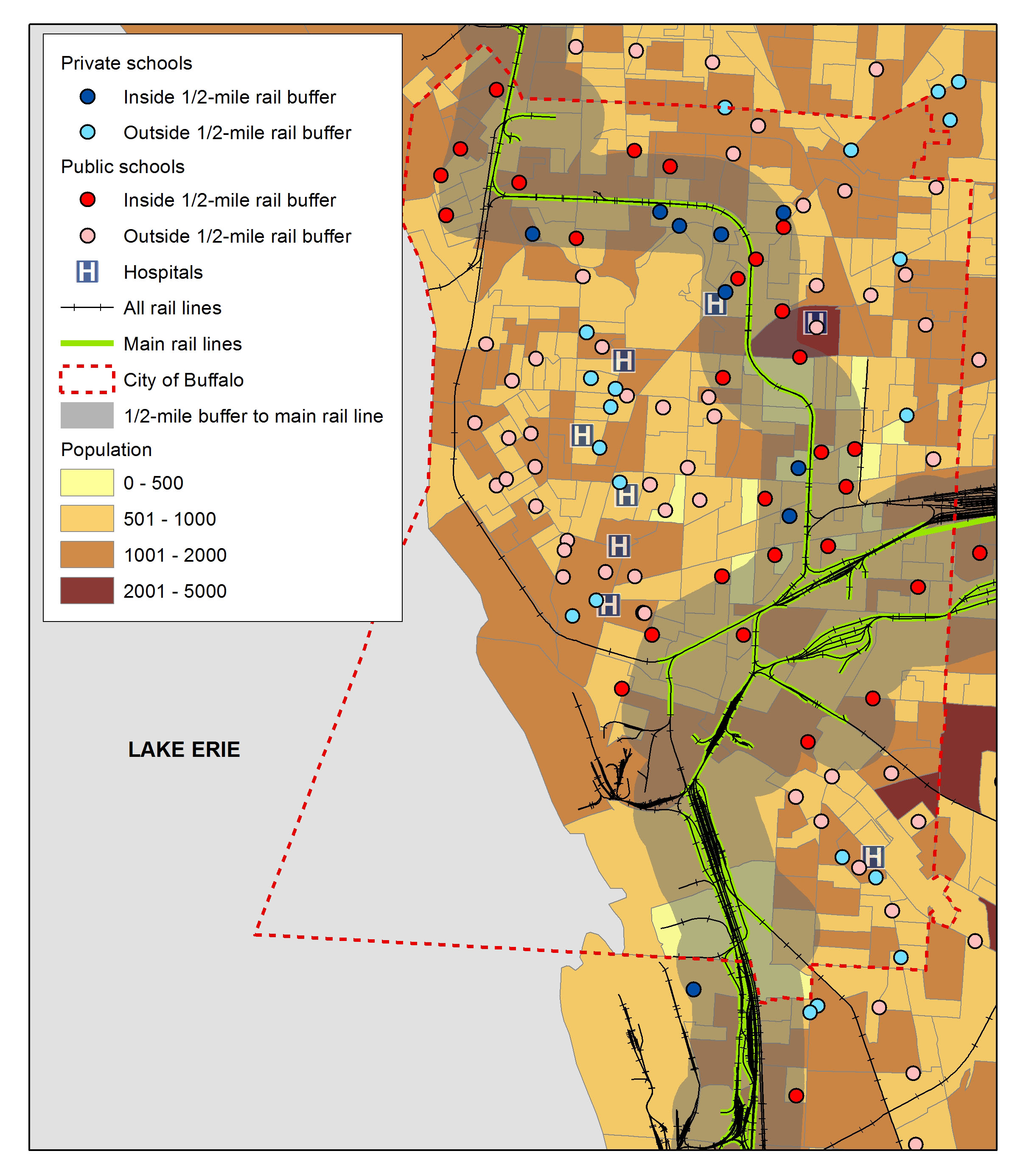

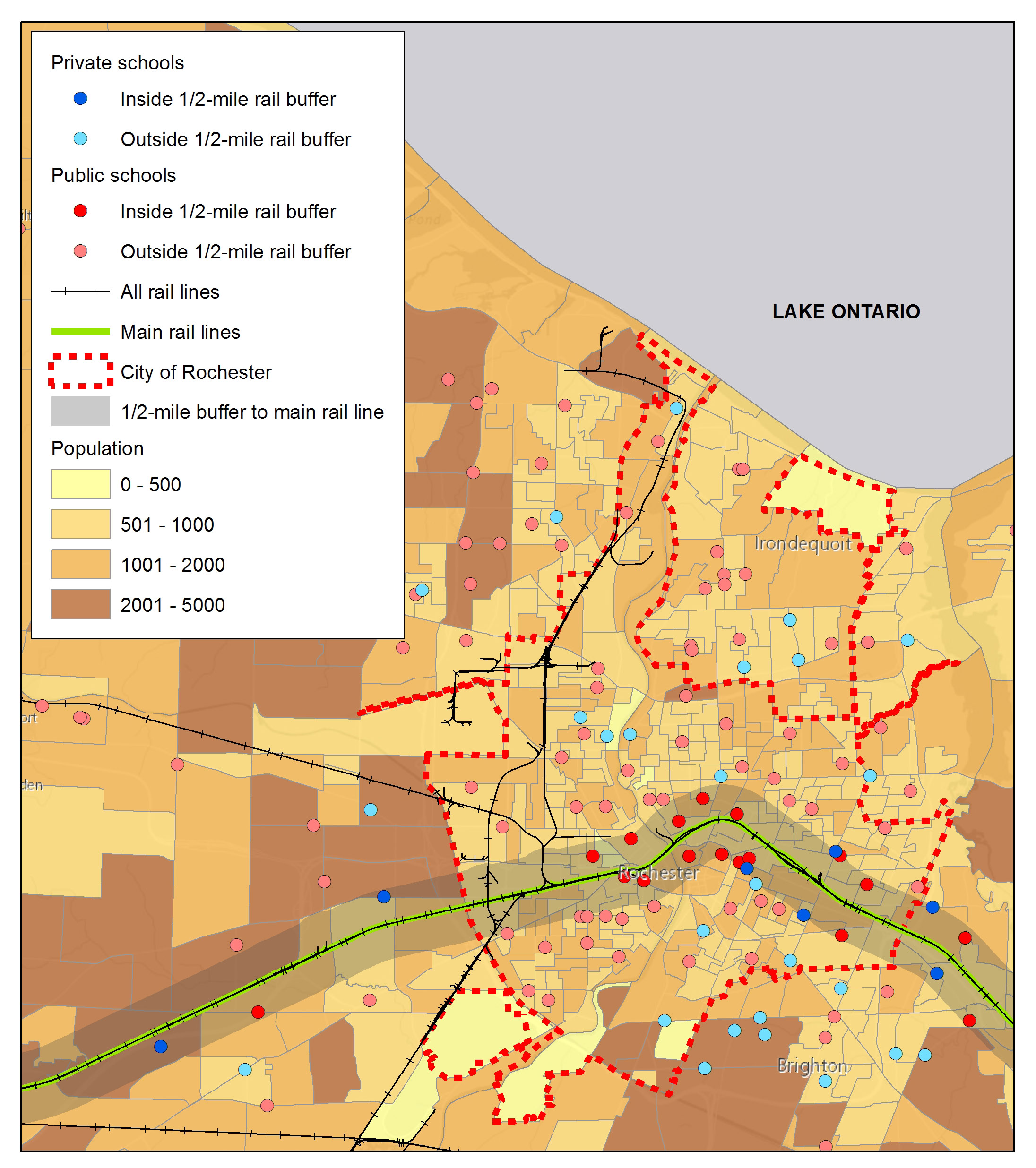

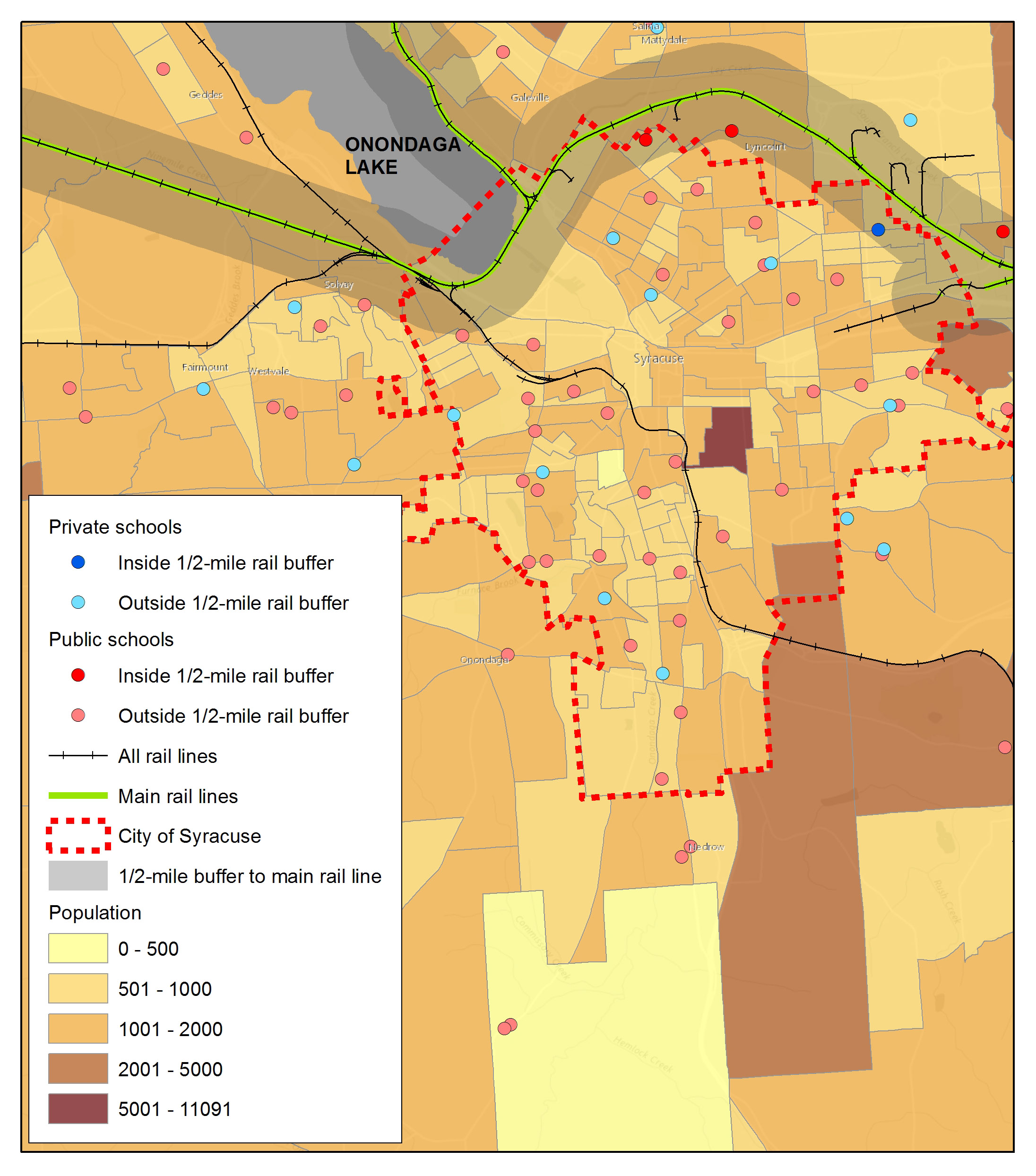

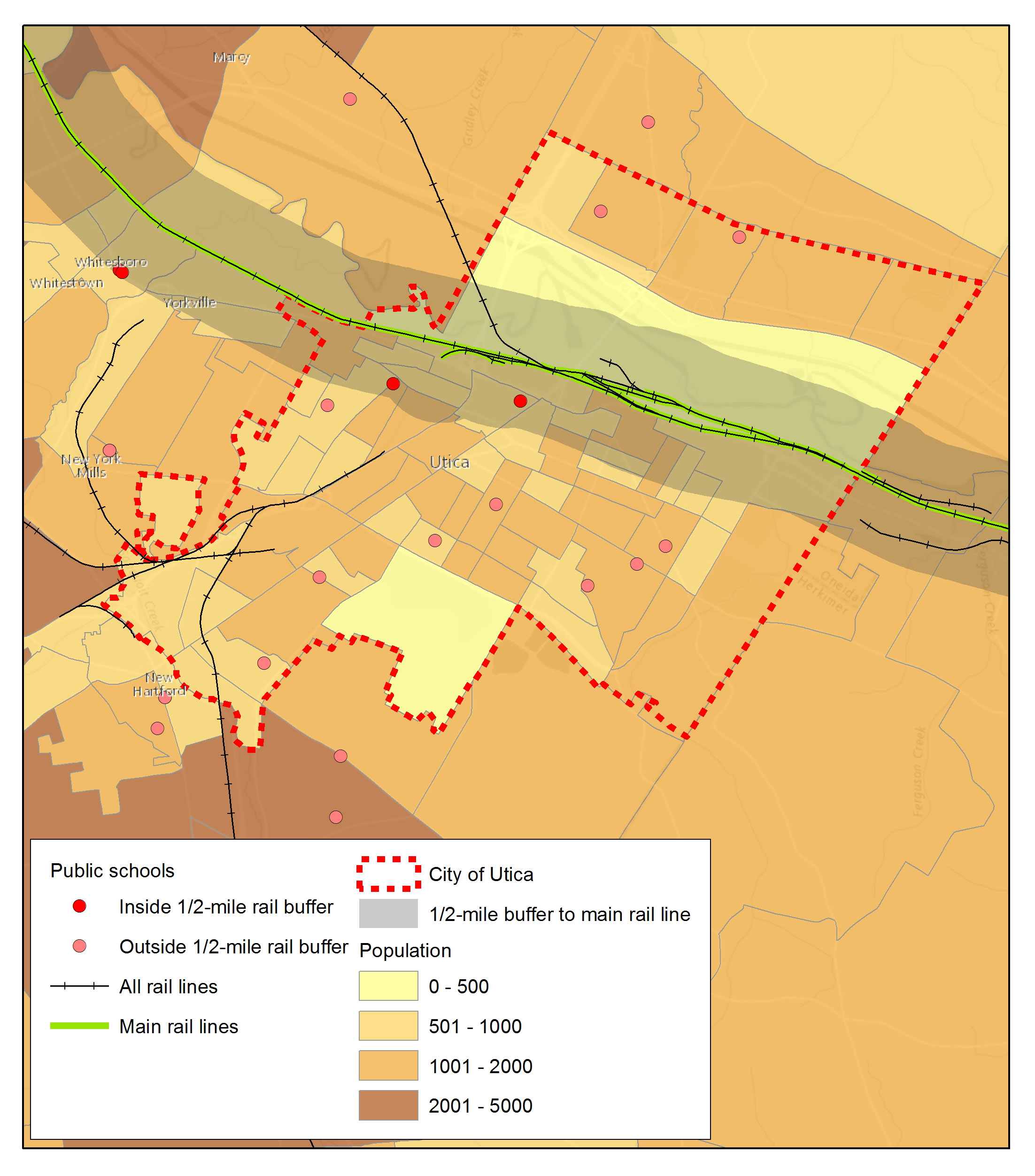

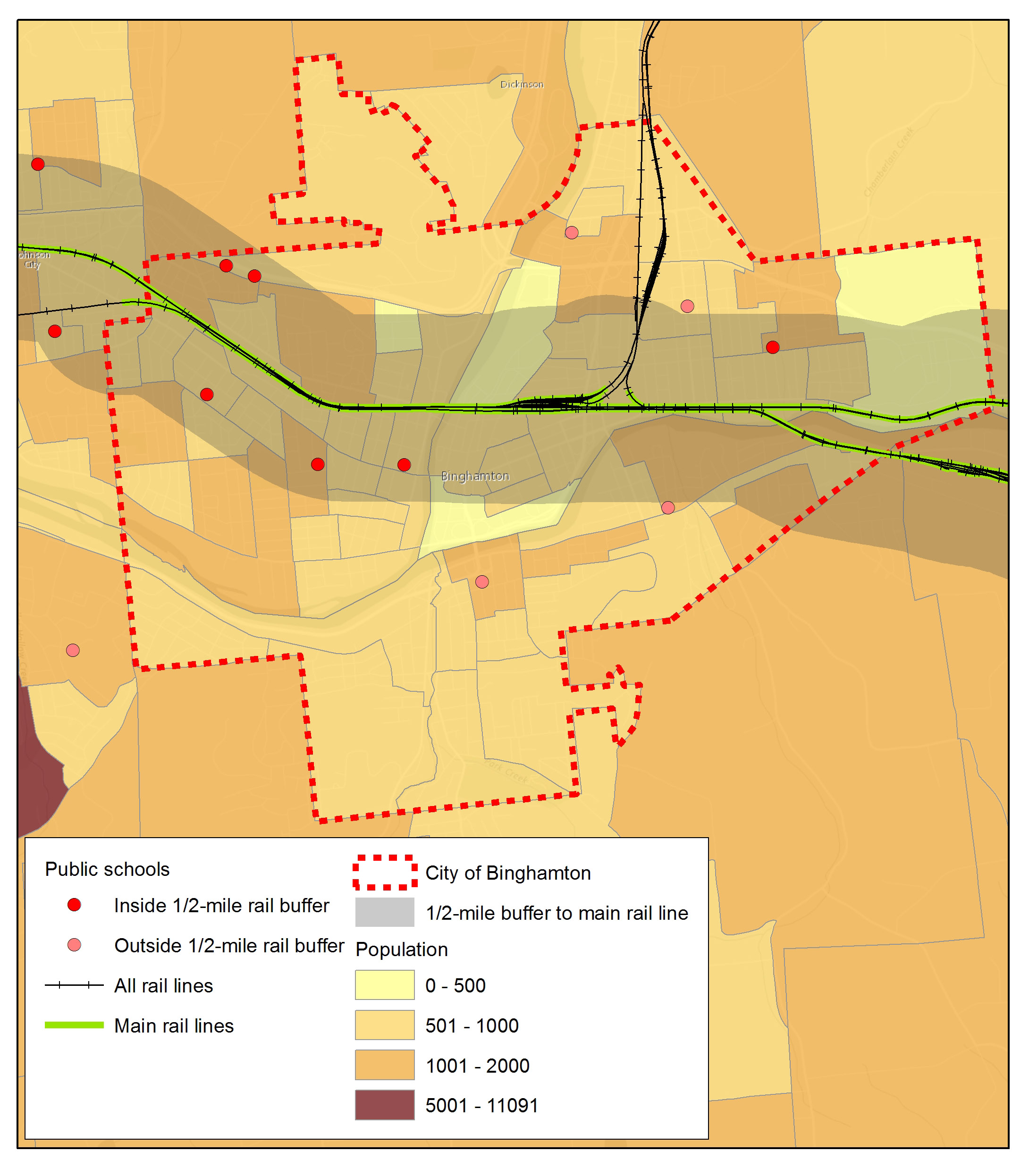

These same trains pass through other major cities in Western and Central New York, including Buffalo, Rochester, Syracuse, and Utica. Not only are the railroads in proximity to significant population centers, they are also close to scores of K-12 schools, endangering the wellbeing of thousands of children (Table 1). In fact, across New York State, 495 K-12 public schools, or 12% of the total in the state, are within a half-mile of major railways–the standard evacuation distance for accidents involving railcars filled with flammable liquids and gases, as recommended by the US Department of Transportation (DOT) in their Emergency Response Guidebook. The US DOT also recommends an isolation zone of 1600 meters (1.0 miles) around any railcars filled with those materials if they are on fire.

Map of NYS Rail Lines and K-12 Schools

Click on this interactive map or pan through the state to explore regions outside of Rochester, NY. For a full-screen view of this map, with a legend, click here.

Fig. 1. Buffalo Rail Lines & Proximity to Schools

For example, on their way through the City of Buffalo crude-carrying freight trains pass within a half-mile of residences of more than 86,000 people, as well as 20 public schools and 4 private schools, and within a half-mile of homes of nearly 60,000 people, 15 public schools, and 5 private schools, on the way through Rochester. See Figures 1-5.

Our work stands in support of and extends the excellent analyses already focusing on the Port of Albany done this past summer by the Natural Resources Defense Council and Healthy Schools Network. (See their report, which looked at the north-south rail corridor in New York State that passes along the Hudson River, within close proximity to 75 K-12 schools).

Table 1. Summary of population statistics in proximity to railways for five New York State cities

City

Population

(2010 US Census)

Within ½ Mile of Freight Rail Way

% Population

# K-12 public schools in city

# K-12 private schools in city

Buffalo

261,310

33%

28

8

Rochester

214,989

27.4%

15

5

Syracuse

145,168

16%

4

1

Utica

62,230

28.5%

2

0

Binghamton

47,376

63.5%

6

0

Figures 2-5. Proximity maps for Rochester, Syracuse, Utica, and Binghamton, NY

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2014/09/Train-Lac-Megantic-Feature.png400900Karen Edelsteinhttps://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngKaren Edelstein2014-09-12 16:46:182020-07-21 10:42:45Off the Rails: Risks of Crude Oil Transportation by Freight in NY State and Beyond

Part of the FracTracker Truck Counts Project By Mary Ellen Cassidy, Community Outreach Coordinator, FracTracker Alliance

I was recently invited by a community member to visit his home. It sits in a valley that is surrounded by drilling pads, as well as compressors and processing stations. While walking down the road that passes directly in front of his home, several caravans of gas trucks roared past and continued far into the evening. Our discussion about the unexpected barrage of this new invasion of intense truck traffic was frequently interrupted by the noise of the diesel engines passing nearby. Along with the noise, truck headlights pierced through the windows of the home, and dust flew up from the nearby road onto his garden.

There are many stories like this about homes and families impacted by the increased truck traffic associated with fracking-related activities. FracTracker is currently working with some of these communities to document the intensity of gas and oil trucks travelling their roads. In response to these concerns we have a launched a pilot Truck Counts project to provide support, resources, and networking opportunities to communities struggling with high volume gas truck traffic.

Preliminary Results

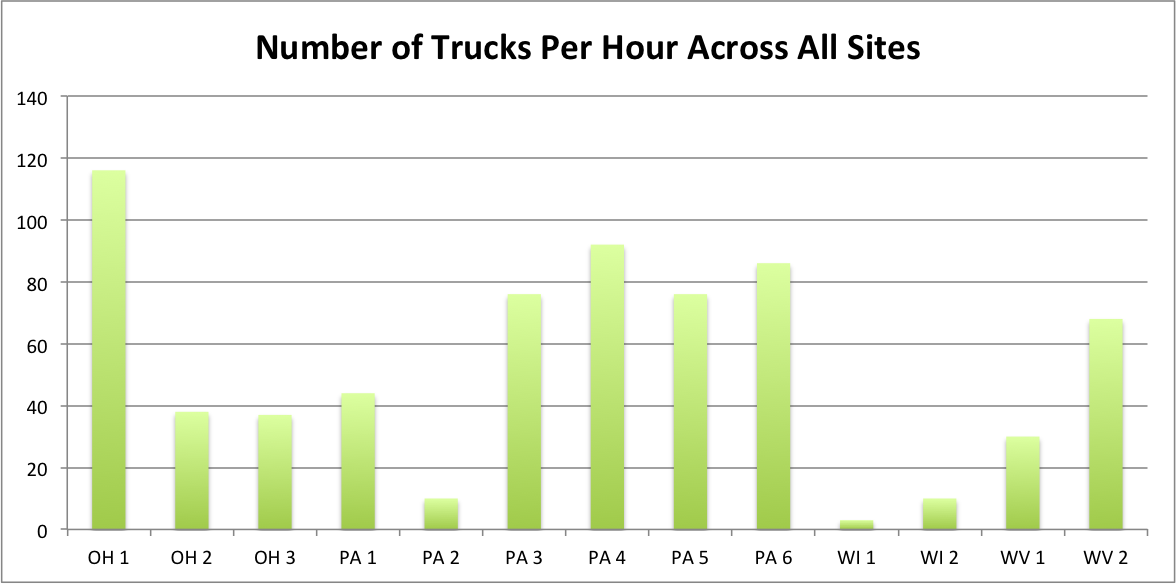

Volunteers in PA, WV, OH and WI have already started to participate in the project, with some interesting results, photos, observations, and suggestions.

To-date, truck counts have varied significantly, as to be expected. Some of the sites where we chose to count passing trucks were very close to drilling activity, and some were more remote. While developing the counting protocol, we often included large equipment and tanker trucks, as well as gas company personnel vehicles (as indicated by white pickup trucks and company logos on the side). While the data vary, the spikes in truck counts do tell the story of a bigger and broader issue – the influx of heavy equipment during certain stages of drilling can be a significant burden on the local community. In total, we counted 676 trucks over 13 sites The average number of trucks that passed by per hour was 44, with a high of 116 an hour, and a low of 5.

About the Project

FracTracker Truck Counts partners with communities to: help identify issues of concern related to high volume gas truck traffic; collect data, photos, videos and narratives related to gas truck traffic; and analyze and share results through shared database and mapping options.

What motivates volunteers to join us in our Truck Counts program? Community concerns include dust, diesel exhaust, spills, accidents, along with other health and safety issues, as well as the cost and inconvenience of deteriorating road conditions resulting from the increased weights and numbers of vehicles. So, what do we already know about the extent of the damages caused by heavy truck traffic?

Public Safety

Several studies have found that shale gas development is strongly linked to increased traffic accidents and that the increases cannot be attributed only to more trucks and people on the road.

Unlike gas truck traffic issues from past oil and gas booms, this recent shale gas boom impacts traffic and public safety in many different ways. The hydraulic fracturing process requires 2,300 to 4,000 truck trips per well, where older drilling techniques needed one-third to one-half as many trips. Another difference is the speed of development that often far outpaces the capacity of communities to build better roads, bridges, install more traffic signals or hire extra traffic officers. Some experts explain increased truck traffic related accidents by pointing to regulatory loopholes such as federal rules that govern how long truckers can stay on the road being less stringent for drivers in the oil and gas industry. Others note that out of state drivers in charge of large heavy duty loads are not always accustomed to the regional weather patterns or the winding, narrow and hilly country roads that they travel.

An Associated Press analysis of traffic deaths in six drilling states shows that in some counties, fatalities have more than quadrupled since 2004 when most other American roads have become much safer in that period (even with growing populations). Marvin Odum, who runs Royal Dutch Shell’s exploration operations in the Americas, said that deadly crashes are “recognized as one of the key risk areas of the business”. Along with the community, gas truck drivers themselves are at risk. According to a study by the National Institute for Occupational Safety and Health, vehicle crashes are the single biggest cause of fatalities to oil and gas workers. The AP study finds that:

In North Dakota drilling counties, the population has soared 43% over the last decade, while traffic fatalities increased 350%. Roads in those counties were nearly twice as deadly per mile driven than the rest of the state

From 2009-2013-

Traffic fatalities in West Virginia’s most heavily drilled counties…rose 42%. Traffic deaths in the rest of the state declined 8%.

In 21 Texas counties where drilling has recently expanded, deaths/100,000 people are up an average of 18 % while for the rest of Texas, they are down by 20%.

Traffic fatalities in Pennsylvania drilling counties rose 4%, while in the rest of the state they fell 19 %.

New Mexico’s traffic fatalities fell 29%, except in drilling counties, where they only fell 5%.

A separate analysis by Environment America using data from the Upper Great Plans Institute finds that – “While the expanding oil industry in North Dakota has produced many benefits, the expansion has also resulted in an increase in traffic, especially heavy truck traffic. This traffic has contributed to a number of crashes, some of which have resulted in serious injuries and fatalities.” In the Bakken Shale oil region of North Dakota, the number of highway crashes increased by 68% between 2006 and 2010, with the share of crashes involving heavy trucks also increasing over that period.”1

Truck accident and spill in WV. Wetzel County Action Group photo, copyright of Ed Wade, Jr.

Public health concerns do not end with traffic accidents and fatalities. An additional cost of heavy gas truck traffic is the strain it places on emergency service personnel. A 2011 survey by State Impact Pennsylvania in eight counties found that:

Emergency services in heavily drilled counties face a troubling paradox: Even though their population has fallen in recent years, 911 call activity has spiked — by as high as 46 percent, in one case.” Along with the demands placed on emergency responders from the number of increased calls, it also takes extra time to locate the accidents since many calls are coming from transient drivers who “don’t know which road or township they are in.

In Bradford County, a heavily drilled area, increased traffic has delayed the response times of emergency vehicles. According to an article in The Daily Review, firefighters and emergency response teams are delayed due to the increased number of accidents, gas trucks breaking down, and gas trucks running out of fuel (some companies only allow refueling once a night).

Road Deterioration and Regional Costs

Roadway degradation from truck traffic. Wetzel County Action Group photo, copyright of Ed Wade, Jr.

An additional cost often passed on to the impacted communities is infrastructure maintenance. In an article from Business Week, Lynne Irwin, director of Cornell University’s local roads program in Ithaca, New York, states, “Measures to ensure that roads are repaired don’t capture the full cost of damage, potentially leaving taxpayers with the bill.”

This Food and Water Watch Report calculated the financial burden imposed on rural counties by traffic accidents alone, estimating that if the heavy truck accident rate in fracked counties had matched those untouched by the boom, $28 million would have been saved.2

Garrett County is currently struggling with anticipating potential gas traffic and road costs. The Garrett County Shale Gas Advisory Committee uses recent studies from RESI ‘s New York and Pennsylvania data to project gas truck traffic for 6 wells/pad at 22,848 trips/pad and 91,392 total truck trips the first year with increasing numbers for the next 10 years. Like many counties, Garrett County also faces the issue that weights and road use are covered by State, not County code. There is a possibility, however, that the County could determine best “routes” for the trucks. (This is a prime example of the need and benefit for truck counts.)

Although truck companies and contractors pay permit fees, often they are either insufficient to cover costs or are not accessible to impacted counties. The Texas Tribune reports, “The Senate unanimously passed a joint resolution which would ask voters to approve spending $5.7 billion from the state’s Rainy Day Fund, including $2.9 billion for transportation debt. But little, if any, of that money is likely to go toward repairing roads in areas hit hardest by the drilling boom.”

Commenting on the argument that gas companies already pay their fair share for road damages they cause, George Neal posts calculations on the Damascus Citizens for Sustainability website that lead him to conclude that, although “the average truck pays around 27 times the fuel taxes an average car pays… according to the Texas Department of Transportation, they do 8,000 times the damage per mile driven and drive 8 times as far each year.”

The funds needed to fill the gap between the costs of road repairs and the amount actually paid by the oil and gas companies must come from somewhere. According to a draft report from the New York Department of Transportation looking at potential Marcellus Shale development costs, “The annual costs to undertake these transportation projects are estimated to range from $90 to $156 million for State roads and from $121-$222 million for local roads. There is no mechanism in place allowing State and local governments to absorb these additional transportation costs without major impacts to other programs and other municipalities in the State.”

Poor Air Quality

Caravan of trucks. Photo by Savanna Lenker, 2014.

Along with public safety and infrastructure costs, increased truck traffic associated with unconventional oil and gas extraction is found to be a major contributor to public health costs due to elevated ozone and particulate matter levels from increased emissions of heavy truck traffic and the refining and processing activities required.

In addition to ozone and particulate matter in the air, chemicals used for extraction and development also pose a serious risk. A recent study in the journal of Human and Ecological Health Assessment found that 37% of the chemicals used in drilling operations are volatile and could become airborne. Of those chemicals, more than 89% can cause damage to the eyes, skin, sensory, organs, respiratory and gastrointestinal tracts, or the liver, and 81% can cause harm to the brain and nervous system. Because these chemicals can vaporize, they can enter the body not only through inhalation, but also absorption through the skin.

The Union of Concerned Scientists note that air pollution from traffic may be worsened in North Dakota by the use of unpaved roads that incorporate gravel containing a fibrous mineral called erionite, which has properties similar to asbestos. Trucks driving over such gravel roads can release harmful dust plumes into the air, which could present health risks for workers and area residents

To address and solve these problems associated with heavy truck traffic, information is needed to assess both qualitatively and quantitatively the scope of the increased truck traffic and its impacts on communities. Collection and analysis of data, as well as community input, are needed to both understand the scope of the problem and to inform effective solutions.

Joining FracTracker’s Truck Counts

In response to community concerns about the impacts of increased truck traffic in their community, FracTracker has developed the Truck Count project to document the intensity of oil and gas traffic in your region, map heavy traffic locations, and offer networking opportunities for impacted communities.

Participation in FracTracker’s Truck Counts can provide grassroots organizations with a valuable opportunity to collect local data, engage volunteers, and educate stakeholders and the public. The data, pictures and narratives collected can be used to support concerned citizens’ efforts to reroute traffic from schools, playgrounds and other sensitive areas; to inform decision makers, public health researchers, and transportation agencies; to serve as a potential launching point for more detailed, targeted studies on public health and safety along with economic development analyses; to compare costs and benefits of oil and gas energy sources to the cost and benefits of energy conservation, efficiency and renewable energy.

Also, by sharing your community’s counts and stories on FracTracker.org, you serve other communities by increasing the awareness of the impacts of oil and gas truck traffic nationwide.

FracTracker’s Truck Counts provides the following resources to conduct the counts:

information and education on gas and oil truck identification,

data sheets for easy counting, and

tips for selecting safe and accessible counting locations in your community.

We look forward to working with you and supporting your community. If you are interested in working on this important crowdsourcing project with us, please contact:

In addition, a 2013 study from Resources for the Future found that shale gas development is linked to traffic accidents in Pennsylvania with a significant increase in the number of total accidents and accidents involving a heavy truck in counties with a relatively large degree of shale gas development as compared to counties with less (or no) development.

The 2013 Food and Water Watch Report finds similar correlations. Shale gas drilling was associated with higher incidents of traffic accidents in Pennsylvania. This trend was strongest in counties with the highest density of fracking wells. The decrease in the average annual number of total vehicle crashes was 39% larger in unfracked rural counties than in heavily fracked counties. (analysis based on data from US Census Bureau, PA DEP and PennDOT).

In a recent Karnes County, Texas analysis “Traffic accidents and fatalities have skyrocketed in the shale boom areas….with an increases of 1,000% in commercial motor vehicle accidents from 2008-2011.

According to a 2013 Texas Public Threat Safety Report, “In the three Eagle Ford Shale counties where drilling is most active, the number of crashes involving commercial vehicles rose 470 percent between 2009 and 2011. In the 17 counties that make up the Permian Basin, fatal car crashes involving commercial vehicles have nearly tripled from 14 in 2010 to 41 in 2012.

As a result of heavily using of publicly available infrastructure and services, fracking imposes both immediate and long-term costs on taxpayers. An Environment Texas study reveals that, “Trucks required to deliver water to a single fracking well cause as much damage to roads as 3.5 million car journeys, putting massive stress on roadways and bridges not constructed to handle such volumes of heavy traffic. Pennsylvania estimates that repairing roads affected by Marcellus Shale drilling would cost $265 million”.

Researchers from the RAND Corporation and Carnegie Mellon University looked at the design life and reconstruction cost of roadways in the Marcellus Shale formation in Pennsylvania. Their findings in Estimating the Consumptive Use Costs of Shale Natural Gas Extraction on Pennsylvania Roadways, note that local roads are generally designed to support passenger vehicles, not heavy trucks, and that “the useful life of a roadway is directly related to the frequency and weight of truck traffic using the roadway.” The study’s findings include:

“The estimated road-reconstruction costs associated with a single horizontal well range from $13,000 to $23,000. However, Pennsylvania often negotiates with drilling companies to rebuild smaller roads that are visibly damaged, so the researchers’ conservative estimate of uncompensated roadway damage is $5,000 and $10,000 per well.

While the per-well figure of $5,000-$10,000 appears small, the increasingly large number of wells being drilled means that substantial costs fall on the state: “Because there were more than 1,700 horizontal wells drilled [in Pennsylvania] in 2011, the statewide range of consumptive road costs for that year was between $8.5 and $39 million,” costs paid by state transportation authorities, and thus taxpayers.”

The feature photo at the top of the page was taken by Savanna Lenker, 2014.

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2014/09/TruckCounts.png400900FracTracker Alliancehttps://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngFracTracker Alliance2014-09-11 15:18:072020-07-21 10:42:44Here They Come Again! The Impacts of Oil and Gas Truck Traffic

Commentary on Shale Gas Operations: First in a Series of Articles

By Bill Hughes, Community Liaison, FracTracker Alliance

Statoil Well Pad Fire: June 28-29, 2014

The early riser residents along Long Ridge Road in Monroe County are among the first in Ohio to see the sun coming up over the West Virginia hills. It rose about 6:00 am on the morning of June 28th. Everyone assumed that this would be a normal Saturday morning. Well, at least as normal as it had been for the better part of two years since the site preparation and drilling started.

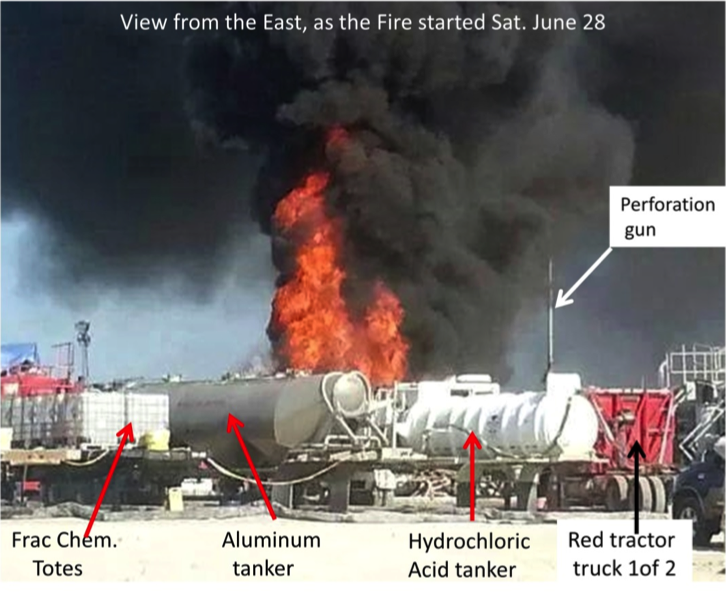

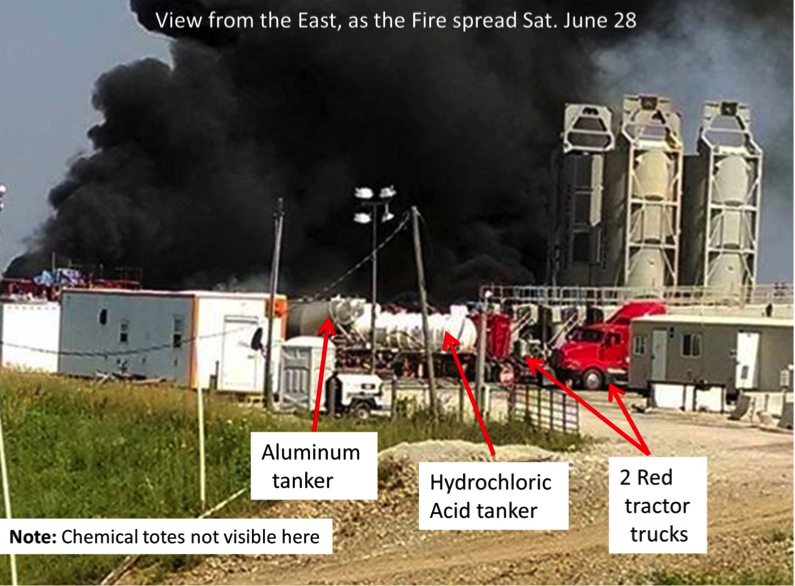

For those residents on Long Ridge who were not early risers, the blaring sirens, the smell of acrid smoke, and the presence of fire trucks and other emergency vehicles shortly after 9:00 am must surely have made them wonder if they were in the midst of a nightmare. A quick glance outside toward the Statoil Eisenbarth well pad and they would have seen this view:

Figure 1. View from the southeast, as the fire spread on Sat. June 28th

The image in Fig. 1 would be enough to make most folks feel somewhat panicky and consider evacuating the neighborhood. That is exactly what soon happened – definitely not the start of a normal Saturday morning.

Adjusting to the New Normal

The traffic in the area had been a problem ever since site preparation started on the nearby well pad. The State expected the drillers to keep up the road. Crews also provided lead escort vehicles to help the many big trucks negotiate the narrow road way and to clear the residential traffic. Access to the well site required trucks to climb a two-mile hill up to the ridge top.

Fig. 2. Neighbors’ views of the fire

Until June 28th, most folks had become accustomed to the extra noise, diesel fumes, and congestion and delays that always come with any shale gas well exploration and development in the Marcellus shale gas active area. Most of the neighbors had gotten used to the new normal and reluctantly tolerated it. Even that was about to change, dramatically. As the sun got higher in the eastern sky over WV, around 9:00 AM, suddenly the sky started to turn dark. Very dark. Sirens wailed. Red trucks started a frenzied rush down Long Ridge from all directions. There was a fire on the well pad. Soon it became a very large, all consuming fire. Smoke, fire, bitter fumes, and no one seemed to know yet exactly what had happened, and what was likely to happen soon.

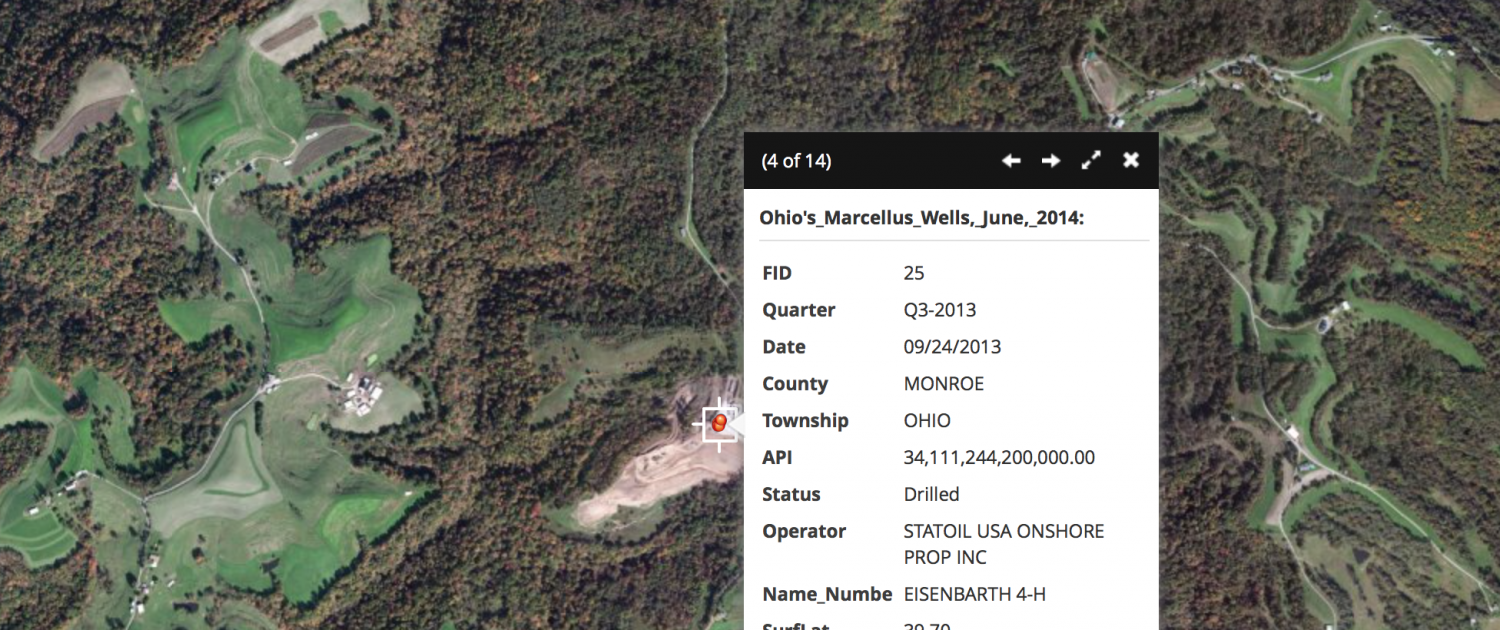

This gas well location, called the Eisenbarth pad, recently changed operators. In January 2013, the well pad property and its existing well and equipment were bought out by Statoil, a company based in Norway. Statoil had since drilled seven more wells, and even more were planned. The original single well was in production. Now in late spring and early summer of 2014 the new wells were to be “fracked.” That means they were ready to be hydraulically fractured, a procedure that follows the completion of the drilling process.

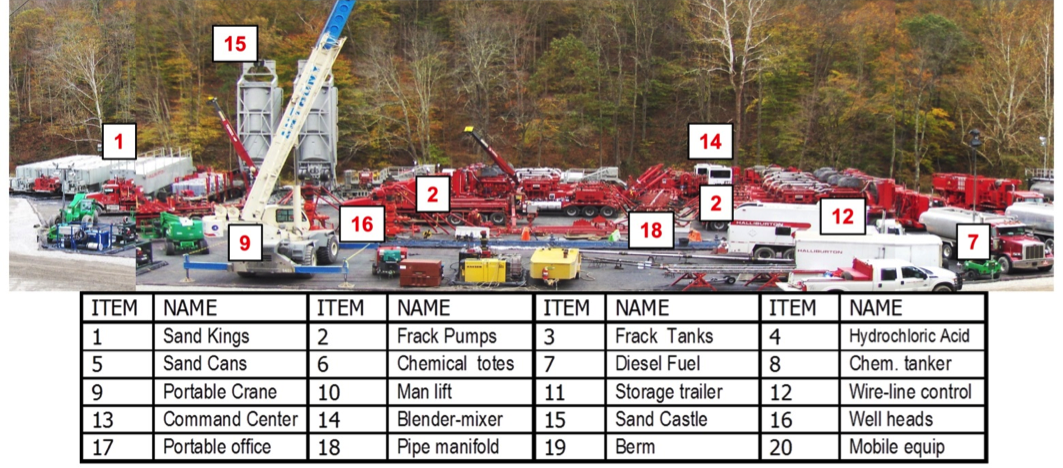

Statoil hired as their fracturing sub-contractor Halliburton. All of the fracturing pump trucks, sand kings, Sand Castles, and control equipment were owned and operated by Halliburton. The fracturing process had been ongoing for some weeks when the fire started. The eastern Ohio neighbors now watched ~$25 million worth of equipment go up in smoke and flames (Fig. 2). The billowing smoke was visible for over 10 miles.

Industrial accidents are not rare in the Ohio Valley

Many of the residents nearby had worked in the coal mining industry, aluminum plants, chemical plants, or the coal fired power plant that were up and down the Ohio River. Many had since retired and had their own industrial accident stories to tell. These were frequently private stories, however, which mostly just their co-workers knew about. In an industrial plant, the common four walls and a roof kept the dangerous processes confined and enabled a trained response to the accidents. The traditional, industrial workplace had well-proven, customized workplace safety standards. Professional maintenance personnel were always nearby. In stark contrast, unconventional gas well pads located in our rural communities are very different. They are put in our hayfields, near our homes, in our pastures and just down the road. You cannot hide a community accident like this.

Sept 2014 Update: Video of the fire, Copyright Ed Wade, Jr.

Print Media Coverage of the Fire

Within days, many newspapers were covering the well pad fire story. The two nearby weekly newspapers, one in Monroe County, Ohio and the other in Wetzel County, West Virginia both had detailed, long articles the following week.

Fig. 3. View from the east as the fire started

The Monroe County Beacon on July 2, 2014 said that the fire spread quickly from the small original fire which was totally surrounded within the tangled complex of equipment and high pressure piping. Early Saturday morning, the first responder would likely have seen a rather small somewhat localized fire as shown in Fig. 2. The photo to the right (Fig. 3) is the view from the east, where the access road is on Long Ridge road. This point is the only access into the Statoil well pad. The view below, showing some still intact tanker trucks in the foreground, is looking west toward the well location. Pay attention to the couple of trucks still visible.

The Monroe County emergency director said it was his understanding that the fire began with a ruptured hydraulic hose. The fluid then ignited on a hot surface. He said, “…by 9:10 AM the fire had spread to other pumps on the location and was spreading rapidly over the well pad.” Emergency responders needed water now, lots of it. There is only one narrow public road to the site at the top of a very long, steep hill and only one narrow entrance to the densely congested equipment on the pad. Many Volunteer Fire Departments from both Ohio and West Virginia responded. A series of tanker trucks began to haul as much water to the site as possible. The combined efforts of all the fire departments were at best able to control or contain but not extinguish the powerful, intensely hot and growing blaze. The Volunteer firemen did all they could. The EMS director and Statoil were very grateful for the service of the Volunteer Fire Departments. There was a major loss of most equipment, but none of the 45-50 workers on site were injured.

Fig. 4. Well pad entrance

The article from the Wetzel Chronicle also praised the coordinated effort of all the many fire departments. At first they attempted to fight the fire, and then prudently focused on just trying to limit the damage and hoping it did not spread to the well heads and off the well pad itself. The New Martinsville fire chief also said that, “… the abundance of chemicals and explosives on the site, made attempts to halt the fire challenging, if not nearly impossible… Numerous plans to attack the fire were thwarted each time by the fires and numerous explosions…” The intense heat ignited anything nearby that was at all combustible. There was not much choice but to let the fire burn out.

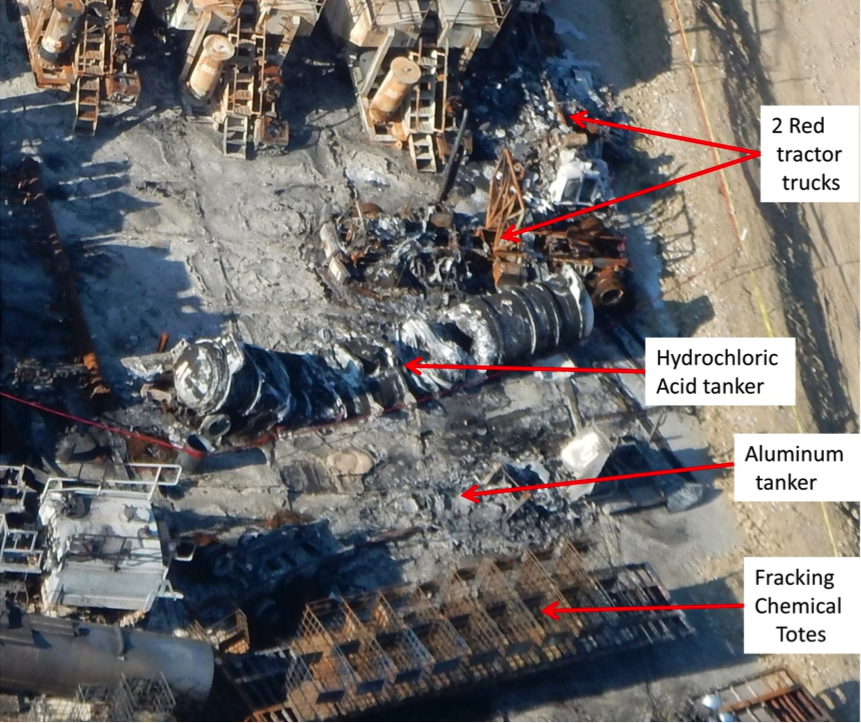

Eventually the view at the well pad entrance as seen from the east (Fig. 3) would soon look like the overhead view (Fig. 5). This aerial imagery shows what little remained after the fire was out – just some aluminum scrap melted into the decking is left of the original, white Hydrochloric Acid tanker truck. Everything near it is has almost vaporized.

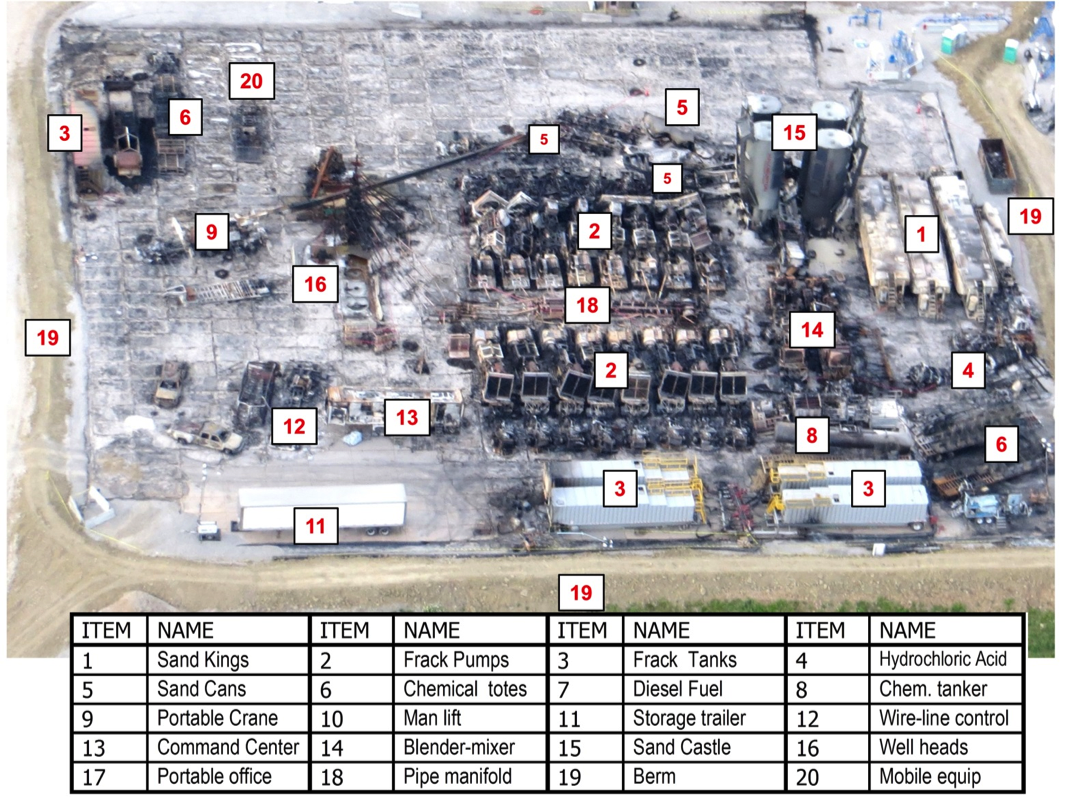

Figure 5. Post-fire equipment identification

Efforts to Limit the Fire

Fig. 6. Protected white trailer

An excellent example of VFD’s successfully limiting the spread of the fire and controlling the extreme heat can be seen in the photo to the right (Fig. 6). This white storage trailer sure seems to be a most favored, protected, special and valuable container. It was.

It was filled with some particularly dangerous inventory. The first EPA report explains it thus:

A water curtain was maintained, using pump lines on site, to prevent the fire from spreading to a trailer containing 1,100 pounds of SP Breaker (an oxidizer), 200 pounds of soda ash and compressed gas cylinders of oxygen (3-2000 lb.), acetylene (2-2000 lb.), propane (6-20 lb.), among miscellaneous aerosol cans.

Fig. 7. Post-fire pad layout

Yes, this trailer got special treatment, as it should. It contained some hazardous material. It was also at the far southwest corner of the well pad with minimal combustibles near it. That was also the closest corner to the nearby holding pond, which early on might have held fresh water. Now the holding pond is surely very contaminated from flowback and runoff.

The trailer location can be seen in the picture to the right in the red box (Fig. 7), which also shows the complete well pad and surrounding area. However, in comparison to the one white storage trailer, the remainder of the well pad did not fare so well. It was all toast, and very burned toast at that.

Columbus Dispatch and the Fish Kill

Besides the two local newspapers, and Wheeling Jesuit researchers, the Columbus Dispatch also covered the story and provided more details on the 3- to 5-mile long fish kill in the stream below the well pad. Additional facts were added by the two EPA reports:

Those reports list in some detail many of the chemicals, explosives, and radiological components on the well pad. Reader note: Get out your chemical dictionary, or fire up your Google search. A few excerpts from the first EPA report are provided below.

…Materials present on the Pad included but was not limited to: diesel fuel, hydraulic oil, motor oil, hydrochloric acid, cesium-137 sources, hydrotreated light petroleum distillates, terpenes, terpenoids, isoproponal, ethylene glycol, paraffinic solvents, sodium persulfate, tributyl tetradecyl phosphonium chloride and proprietary components… The fire and explosion that occurred on the Eisenbarth Well Pad involved more than 25,000 gallons of various products that were staged and/or in use on the site… uncontained run-off was exiting the site and entering an unnamed tributary of Opossum Creek to the south and west and flowback water from the Eisenbarth Well #7 was spilling onto the well pad.

Reader Warning: If you found the above list overly alarming, you might choose to skip the next equally disturbing list. Especially since you now know that this all eventually flowed into our Ohio River.

The EPA report continues with more specific chemical products involved in the fire:

Initial reports identified the following products were involved and lost in the fire: ~250 gallons of hydrochloric acid (28%), ~7,040 gallons of GasPerm 1000 (terpenes, terpenoids, isopropanol, citrus extract, proprietary components), ~330 gallons of LCA-1 (paraffinic solvents), ~ 1900 gallons of LGC-36 UC (hydrotreated light petroleum distillate, guar gum), ~1000 gallons of BC-140 (monoethanolamine borate, ethylene glycol), ~3300 gallons of BE-9 (tributyl tetradecyl phosphonium chloride), ~30,000 gallons of WG-36 (polysaccharide gel), ~1,000 gallons of FR-66 (hydrotreated light petroleum distillate), ~9000 gallons of diesel fuel, ~300 gallons of motor and hydraulic oil.

Even more details of the incident and the on-site chemicals are given in the required Statoil 30-day report (PDF).

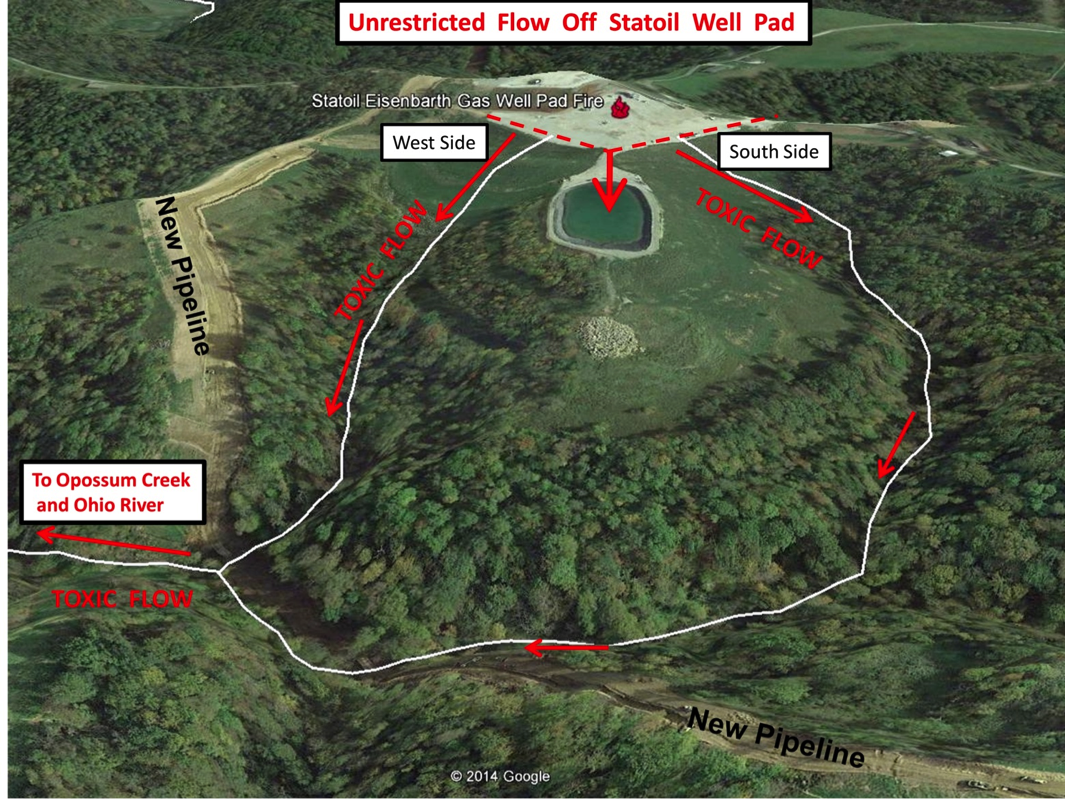

The EPA reports detail the “sheet” flow of unrestricted contaminated liquids off of the well pad during and after the fire. They refer to the west and south sides. The below Google Earth-based map (Fig. 8) shows the approximate flow from the well pad. The two unnamed tributaries join to form Opossum Creek, which then flows into the Ohio River four miles away.

Figure 8. Map showing path of unrestricted flow off of the Statoil well pad due to a lack of berm

After describing some of the known chemicals on the well pad, the EPA report discusses the construction of a new berm, and where the liquid components flowed. Below is a selection of many excerpts strung together, from many days, taken directly from the EPA reports:

…unknown quantities of products on the well pad left the Site and entered an unnamed tributary of Opossum Creek that ultimately discharges to the Ohio River. Runoff left the pad at various locations via sheet flow….Initial inspections in the early hours of June 29, 2014 of Opossum Creek approximately 3.5 miles downstream of the site identified dead fish in the creek…. Equipment was mobilized to begin constructing an earthen berm to contain runoff and to flood the pad to extinguish remaining fires…. Once fires were extinguished, construction of a berm near the pad was begun to contain spilled liquids and future runoff from the well pad… Statoil continued construction of the containment berm currently 80% complete. (6-30-14)… Assessment of chemicals remaining on the well pad was completed. The earthen berm around the pad was completed, (7-2-14)… ODNR Division of Wildlife completed their in stream assessment of the fish kill and reported an estimated 70,000 dead fish from an approximately 5 mile stretch extending from the unnamed tributary just west of the Eisenbarth Well Pad to Opossum Creek just before its confluence with the Ohio River… Fish collection was completed. In total, 11,116 dead fish were collected (20 different species), 3,519 crustaceans, 7 frogs and 20 salamanders.

The overall conclusion is clear. Large quantities of various chemicals, mixed with very large amounts of already contaminated water, when flooding a well pad that had no berms around it, resulted in a significant fish kill over several miles. After the fire Statoil then constructed a berm around the well pad. If there had been a pre-existing berm – just 12 inches high and level – around the well pad, it could have held over 600,000 gallons of runoff. That amount is twice the estimated quantity of water used to fight the fire. (Note: my old 35 HP farm tractor and a single bottom plow can provide a 12-inch high mound of dirt in one pass.)