VIEW MAP & DATA

Overview

In December 2019, Plains All-American and Valero pipeline companies announced plans to build the 49-mile Byhalia Pipeline through southwestern Tennessee and northwestern Mississippi. The proposed Byhalia Connection Pipeline is a 24-inch, high pressure (1500 psi) conduit, conveying crude oil coming Oklahoma, bound for the Gulf coast. The pipeline, which is designed to carry up to 420,000 barrels of oil a day, provides a link between the Diamond Pipeline to the west and the Capline Pipeline to the east. Construction is planned to begin in early 2021, and be completed by year’s end. Plains All-American insists that all safety precautions are being considered, but the outcry among residents and environmental advocates has been considerable.

Many factors—environmental, geological, social, and economic—have emerged as reasons that this pipeline should not move ahead. And industry most certainly didn’t count on pushback from the local community. Residents, allies, and the media have risen up to challenge the project. In this article, we’ll take a look at the story from various perspectives, augmented by FracTracker’s mapping insights.

UPDATE: On Friday, July 2, 2021, Plains All American announced that it would be abandoning its plans to build the controversial Byhalia Connection Pipeline. As one activist involved in the fight proudly stated, “We’ve shown them that we aren’t the path of least resistance. We are the path of resilience.” Read more about this momentous victory for the people of South Memphis here.

Contents

Environmental and hydrological

Human health

Geological

Demographics and disaster preparedness

Economics and land ownership

Pipeline Incidents

Where From Here?

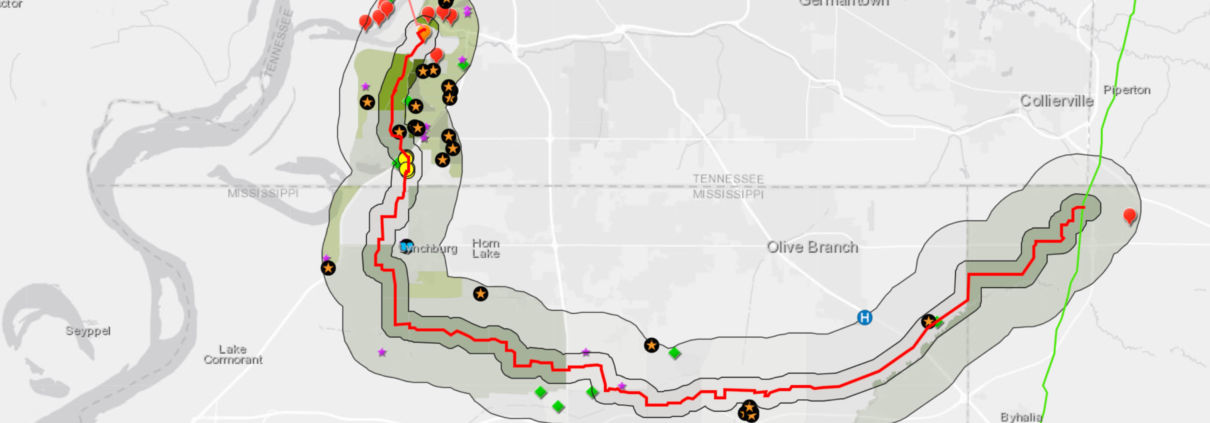

Byhalia Connection Pipeline

This interactive map looks at the various risks associated with the proposed Byhalia Connection Pipeline. The map contains all of the data layers related to the topics in this article. Scroll down in this article to find interactive maps separated out by topic. All data sources are listed in the “Details” section of the maps, as well as at the end of this article. Items will activate in this map dependent on the level of zoom in or out.

View Full Screen | Updated March, 2021

Environmental and hydrological

The 49-mile route of the proposed Byhalia Connection Pipeline passes through a patchwork of rural, suburban, and urban landscapes. Along the route, the pipeline would cross seven named waterways — Johnson Creek, Hurricane Creek, Bean Patch Creek, Camp Creek, Short Brook, Camp Creek Canal, and Coldwater Creek — and also pass immediately adjacently to a nearly 5-mile-long wetlands complex that surrounds the Coldwater River. But the natural environment is home to many more waterways than those that have official names on topographic maps. According to FracTracker’s inspection of National Wetlands Inventory data collected by the United States Fish and Wildlife Service, the proposed pipeline crosses or touches 62 streams in 102 separate locations, 25 forested wetlands, an emergent wetland, 17 ponds, and one lake.

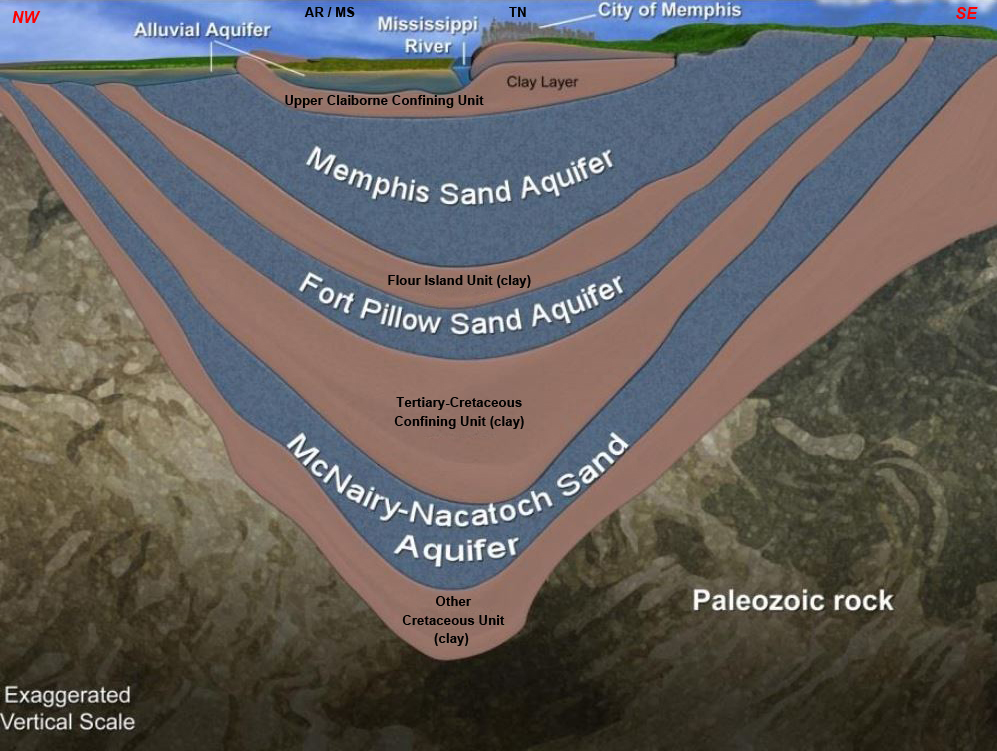

Close to the City of Memphis, 0.8 miles of the pipeline would run directly through the Davis Wellfield Wellhead Protection Zone. The proposed pipeline is located over the extraordinary Memphis Sands Aquifer, which provides potable water for more than 400,000 people. Memphis Light, Gas and Water (MLGW) Company pumps water from over 175 artesian wells in Shelby County, Tennessee, alone—right in the path of the pipeline route. The aquifer itself is a sensitive resource, already under demand by the human population of the area, as well as many industries such as breweries and as a supply of cooling water for a nearby power plant.

Memphis Sands Aquifer is part of the larger Middle Claiborne Aquifer, a groundwater and geological unit in the lower Mississippi drainage. Technically speaking, the Memphis Sands portion of the aquifer is located in Tennessee, but is continuous with the Sparta Sands Aquifer, located in Mississippi. In the eastern portion of the Byhalia Connection’s proposed route, wetlands along Coldwater River are directly part of the recharge zone of this aquifer.

Byhalia hydrologic components

To learn more about the hydrologic features that may be impacted by the proposed Byhalia Connection Pipeline, explore our interactive map. When this map is viewed full-size, you can choose to view additional layers from the drop-down Layers menu.

View Full Screen | Last updated March 2021

The Memphis Sands Aquifer lies 350 to 1000 feet under Memphis (see Figure 1), and spans an area of 7500 square miles, roughly the size of Lake Ontario. “It’s one of the best (aquifers) in the world in terms of thickness, aerial content, quality of water”, according to Roy Van Arsdale, Professor of Geology at University of Memphis. Under Shelby County alone — where Memphis is located — the aquifer contains approximately 58 trillion gallons of clean water. Over time, the aquifer has seen threats from overpumping, as the population of Memphis grew. In addition, industrial pollution has turned up in some samples, including cancer-causing benzene. Policy protections on the aquifer have been lacking, although there is increasingly vocal public awareness about the need for more comprehensive groundwater resource protection in the area.

Figure 1. Cross-section of aquifers under Memphis, TN. Graphic modified from here.

Although water withdrawals from the aquifer have declined significantly since 2000 due, in part, to more water-efficient household appliances that reduce demand in comparison with older models, the MLGW pumped 126 million gallons a day from the aquifer in 2015. Consequently, the level of the aquifer has been rising in recent years, as the rate of recharge has exceeded use.

The courts have suggested that the water in the aquifer is an intrastate resource, and that therefore, Mississippi cannot have sole governance over the extraction of the water within its state boundaries. Instead, usage should be through “equitable apportionment.” Further arguments are still pending, as of late 2020. In short, as Figure 1 shows, withdrawal and recharge of the aquifer do not respect state boundaries.

The details of water law, and who can tap into these, and other deep, ancient aquifers, are complex questions in which agriculture, ecology, geology, and technology bump up against each other. All of these interests, not to mention human health, could be heavily impacted by a crude oil pipeline rupture or other accident that resulted in contamination of this groundwater resource.

Human health

Crude oil spills release a panoply of volatile organic compounds into the air and water that are extremely harmful to human and environmental health. These include benzene, ethylbenzene, toluene, and xylene. Polycyclic aromatic hydrocarbons (PAHs), such as carcinogenic benzo[a]pyrene, are also released. In addition, if the oil combusts, hydrogen sulfide gas, as well as heavy metals, including nickel, mercury, and cadmium, will become airborne.

Figure 2. Observed/documented oil spill-induced acute and chronic human health effects. Source: Guidance for the Environmental Public Health Management of Crude Oil Incidents, Health Canada (2018).

The take-away is that crude oil spills from pipelines are not uncommon, result in environmental damage, impacts on the health and safety of workers and nearby residents. Most importantly, despite monitoring and inspections, pipelines fail. A partial list of pipeline failures is shown in the sidebar.

Within the 2-mile buffer of the pipeline, there are 20 facilities that the United States Environmental Protection Agency (US EPA) lists in its Toxic Release Inventory (TRI), including several chemical plants associated with hydrocarbon extraction. Carcinogens such as polycyclic aromatic compounds, benzene, styrene, dioxins, and naphthalene are just a few of the compounds produced by facilities owned by Valero Energy Corporation, Drexel Chemical Company, and other companies within the 2-mile buffer zone of the pipeline, which compound the risks to the populations there. In addition, while the TRI lists exposure to toluene and xylene from these facilities, neither are categorized by EPA’s TRI database as a carcinogen due to a lack of data; however, their deleterious impacts on the central nervous system are undeniable, and well- documented (see examples here and here).

Byhalia civic and industrial facilities

View Full Screen | Updated March, 2021

In this interactive map, you can see sites in the proposed Byhalia Connection route that are listed in the TRI, as well as civic facilities like schools, daycare centers, and health care facilities. When this map is viewed full-size, you can choose to view additional layers from the drop-down Layers menu.

Geological

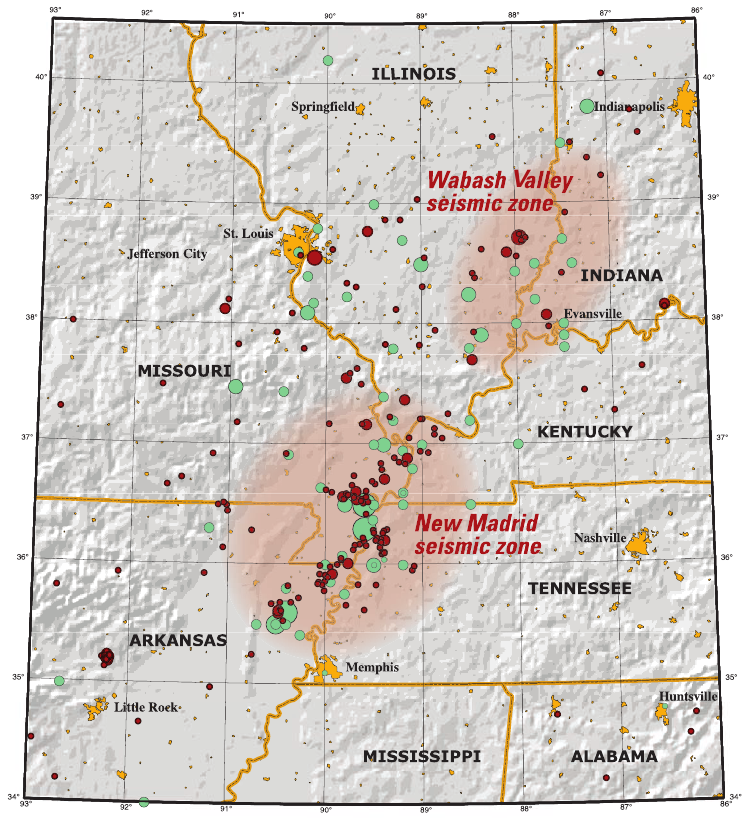

The most active seismic fault line in the eastern United States — the New Madrid Fault — is located about 40 miles from one end of the proposed pipeline (see Figure 2). The last major earthquakes along this fault line occurred in 1811 and 1812. Although the current Richter scale was not in use at that time, first quake in mid-December 1811 was estimated to have had a magnitude of between 7.2 and 8.2, and was followed by an aftershock of about 7.4. In January and February of 1812, there were additional earthquakes of this magnitude. Obviously, at this time in history, there was relatively sparse population in the area, and little infrastructure. Were such a quake to occur today, the outcomes would be catastrophic.

Figure 3: New Madrid Seismic Zone. Source: United States Geological Survey

According to a Wikipedia entry, “[i]n October 2009, a team composed of University of Illinois and Virginia Tech researchers headed by Amr S. Elnashai, funded by the Federal Emergency Management Agency, considered a scenario where all three segments of the New Madrid fault ruptured simultaneously with a total earthquake magnitude of 7.7. The report found that there would be significant damage in the eight states studied – Alabama, Arkansas, Illinois, Indiana, Kentucky, Mississippi, Missouri, and Tennessee – with the probability of additional damage in states farther from the New Madrid Seismic Zone. Tennessee, Arkansas, and Missouri would be most severely impacted, and the cities of Memphis, Tennessee, and St. Louis, Missouri, would be severely damaged. The report estimated 86,000 casualties, including 3,500 fatalities, 715,000 damaged buildings, and 7.2 million people displaced, with two million of those seeking shelter, primarily due to the lack of utility services. Direct economic losses, according to the report, would be at least $300 billion.” Source: University of Illinois report]

Another article on the New Madrid fault added that “….the US Geological Survey and the University of Memphis Center for Earthquake Research estimate there’s a 7 to 10 percent chance of a major quake — one with a magnitude between 7.5 and 8.0 — occurring in the region in the next 50 years….’ The scope is about as big as you could possibly have,’ said Jonathon Monken, director of the Illinois Emergency Management Agency and chairman of the Central U.S. Earthquake Consortium… ‘Putting it in a purely financial context, Hurricane Katrina was a $106 billion disaster. We estimate this would be a $300 billion disaster, the worst in the history of the United States.’”

Earthquake damage to pipelines can occur from movement on the fault itself, soil liquefaction, uplift, and landslides, resulting in potentially catastrophic situations. Engineering solutions to minimize or prevent seismic damage to pipelines do exist. These solutions must be part of the overall pipeline design, however. For example, the Trans-Alaska oil pipeline was constructed with considerations for earthquake impacts in mind. For more information, read about the solution that was implemented there.

Byhalia geological context

This map shows the New Madrid seismic zone in the context of the proposed Byhalia Connection Pipeline. When this map is viewed full-size, you can choose to view additional layers from the drop-down Layers menu.

View Full Screen | Updated March 2021

Demographics and disaster preparedness

As eloquently reported in a series of articles in mlk50.com, the siting of the Byhalia Connection Pipeline is not only an issue environmental tied with the natural environment. This is very much an issue of environmental justice, as well. Many of the census blocks along the proposed, preferred route of the pipeline, are 99% Black. Boxtown, a community in southwest Memphis is one of places, and already has a long history of impacts by environmental contamination from the dozens of industries that operate there. Toxic waste from coal power plants includes heavy metals and radioactive materials.

The pipeline route from Memphis to its terminus in Mississippi takes a circuitous route, avoiding wealthier parts of the city and its suburbs, but goes directly through low-income areas, some of which are inhabited by a nearly 100% Black population.

FracTracker looked at US Census data along the pipeline route, and calculated a half-mile (minimum recommended) and two-mile buffer zone from the pipeline right-of-way to consider populations that might be impacted in the case of an accident.

Byhalia route demographics

Explore the the demographics along the proposed Byhalia Connection Pipeline route. When this map is viewed full-size, you can choose to view additional layers from the drop-down Layers menu, such as the non-white population ration along the proposed pipeline route.

View Full Screen | Updated March 2021

There are 15,000 people living in the immediate evacuation zone of a half mile from the pipeline. In some parts of South Memphis, within this half-mile evacuation zone, population density is above 4,000 people per square mile, and the Black population approaches 100%. Within a two mile distance, the number climbs to over 76,000. Depending on the direction of the wind, a crude oil-induced fire could spew dangerous levels of volatile organic compounds through the air towards these populations. The disproportional risks to minority and low-income populations make the location of this pipeline — undeniably — an issue of environmental justice.

| Demographic |

Within ½ mile of Byhalia Connection Pipeline |

Within 2 miles of Byhalia Connection Pipeline |

| Total population |

15,041 |

76,016 |

| Non-white population |

7204 (48%, although some parts of South Memphis are 99+%) |

27,548 (36%, although some parts of South Memphis are 99+%) |

| Low income population |

4272 (28%, although some parts of South Memphis are 90+%) |

43,486(57%, although some parts of South Memphis are 90+%) |

Table 1: Population demographics along the proposed Byhalia Connection pipeline corridor.

Key civic facilities are also located within the half-mile evacuation zone of the pipeline. Were a disaster to occur, would the schools, childcare centers and medical facilities be able to successfully usher their residents and students to safety? Would they have had regular safety trainings to prepare them for this possibility?

| Facility |

Within ½ mile of pipeline |

Within 2 miles of pipeline |

| Child care |

4 (one within 800 feet) |

30 |

| Public school |

2 (one within 800 feet) |

26 |

| EMS |

2 |

11 |

| Hospital |

0 |

1 |

| Private school |

0 |

1 |

Table 2: Facilities along the proposed Byhalia Connection pipeline corridor (also shown in the interactive map here).

Al Gore calls proposed Byhalia Connection pipeline ‘reckless, racist rip-off’ at rally

Former Vice President Al Gore voiced his opposition to the Byhalia Connection and put Memphis elected officials on notice during a rally against the pipeline on March 14, 2021.

Source: Article in commercialappeal.com

“Why is it that 64% of the polluting facilities of these pipeline communities are located in or adjacent to Black communities? Why is it that the cancer rate in SW Memphis four times higher than the national average? Why is it that Black children suffer from asthma three times more than white children? Why is it that the death rate from asthma for Black children is ten times higher than for white children?” – Former Vice President Al Gore

And two days later, on March 16th, the Memphis City Council unanimously approved a resolution that opposes the Byhalia Connection Pipeline project.

Economics and land ownership

Approximately 300 property owners adjacent to the pipeline have already accepted monetary compensation to abandon their homes or sell property easements to make way for the pipeline. If a landowner refuses payment offered by the pipeline company for a property easement — often far under market value — the company can take the landowner to court, and seize the property (or portion of it) with no requirement of compensation. Although a majority of property owners accepted the terms of the easements drawn up by Byhalia’s developers, at least 14 did not. When numerous owners refused, nine properties were targeted for taking by eminent domain, and sued by the pipeline company. The Southern Environmental Law Center (SELC) is defending many of these property owners, claiming that the seizures — regardless of whether they are temporary or permanent — do not comply with the criteria of meeting a public good. The oil being transported in the proposed pipeline is entirely bound for export.

“The pipeline company is not created by, affiliated with or owned by the government, and the general public would have no access to the proposed crude oil pipeline… So, there is no ‘public use’ justifying the use of the condemnation power as required by Tennessee law,” said one of SELC’s attorneys. In addition, SELC has cited the illegality of the pipeline route because it runs through the municipal wellfield, and therefore violates permits issued by the Army Corps of Engineers. The Army Corp was still considering this request, as of mid-January 2021.

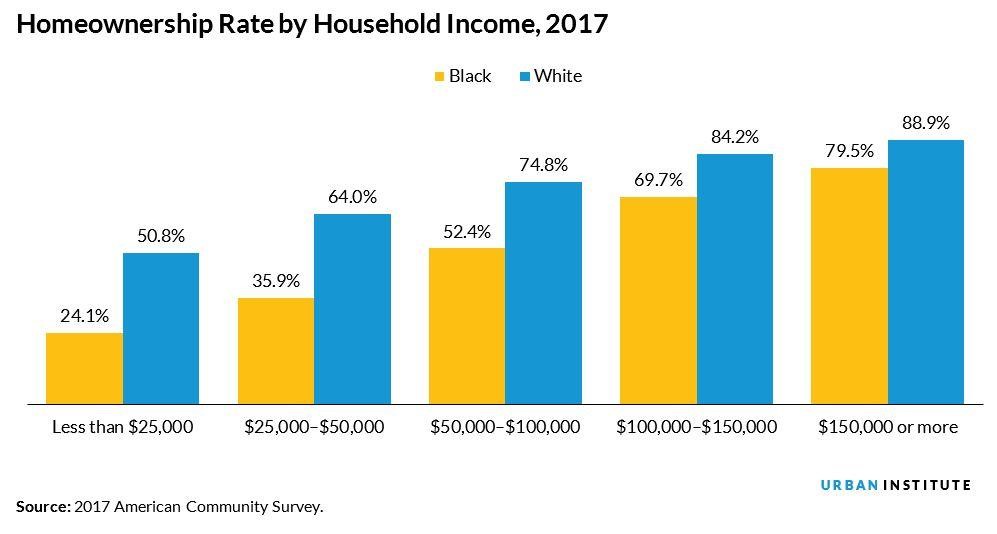

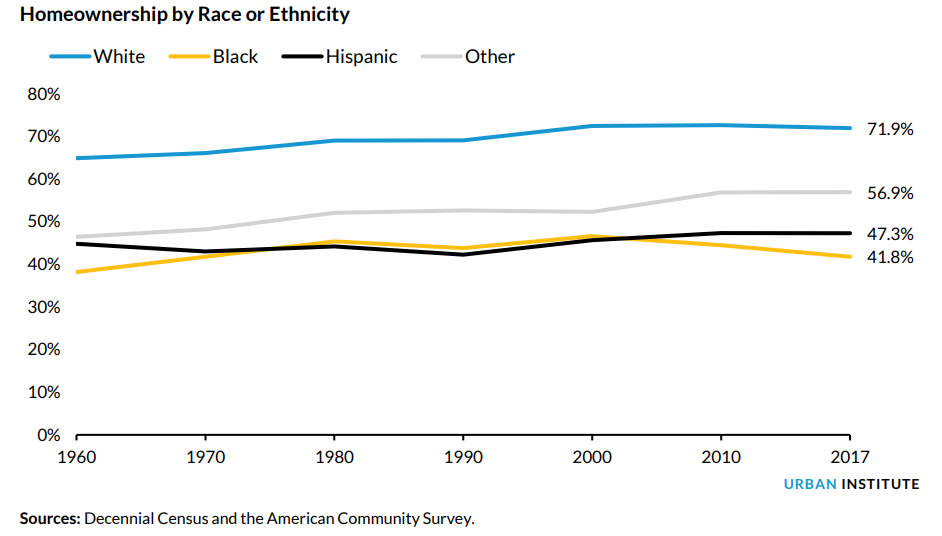

Furthermore, the eminent domain targeting of land owned by Black Americans in the south is a pointed question of racial justice. Historically, black and brown people throughout the United States have had far lower levels of home ownership than whites. This gap is most pronounced in lower income areas.

Figure 5: Homeownership rate in the US, by household income (2017). Source: The Urban Institute.

“The 71.9 percent white homeownership rate in 2017 represented a 0.7 percentage point decline since 2010, and the 41.8 percent black homeownership rate represented a 2.7 percentage point decline during that same period. The 30.1 percentage point gap is wider than it was when race-based discrimination against homebuyers was legal.” The Urban Institute

Figure 6: Homeownership in the US by race or ethnicity. Source: The Urban Institute.

Losing land to eminent domain represents a loss of control for a landowner — white or black. But the loss is especially unjust when a property may have been so hard won, and sometimes the result of a multi-generational lineage of ownership, as is the case for many properties along the Byhalia right-of-way.

Pipeline Incidents

Crude oil spills, 2010-2021

FracTracker has created an interactive map showing the locations of crude oil spills across the United States between 2010 and 2021, using the most up-to-date information from PHMSA, the Pipeline and Hazardous Materials Safety Administration.

View Full Screen | Updated March, 2021

You can also read more about a wider diversity of hazardous liquid materials accidents analyzed by FracTracker in an article from February 2020, entitled “Pipelines Continue to Catch Fire and Explode”.

Case study of a pipeline explosion

A 2020 research paper states, “Modeling and analysis of a catastrophic oil spill and vapor cloud explosion in a confined space upon oil pipeline leaking” provides a stark example of the damage done from the leak and explosion of a crude oil pipeline operating at a third of the pressure proposed for Byhalia.

“It is obvious that the explosion caused big damages to the adjacent buildings, roads, and public structures. Moreover, the explosion, combustion, and the shock wave caused injuries and deaths of workers, pedestrians, and residents. The total affected zone spread nearly 5 km [3.1 miles].”

Note: The oil pipeline shown in Shengzhu, Xu, et al.’s paper in was 28 inches in diameter, and operating at a pressure of between 400 and 660 psi. A vapor cloud from the spill into a municipal drainage area caused this explosion, which killed 62 people and injured 136 in November 2013. The 24-inch, proposed Byhalia pipeline would operate at triple the pressure of the pipeline shown in these photos of its explosion.

(a) bird’s eye view of the location of the explosion point, (b) scene of the oil spill point after explosion, (c) scene of the nearby street, (d) scene of the drainage of the adjacent plant.

Figure 7: Scene of an oil pipeline explosion site in China. (a) bird’s eye view of the location of the explosion point, (b) scene of the oil spill point after explosion, (c) scene of the nearby street, (d) scene of the drainage of the adjacent plant. Image from Shengzhu, Xu, et al.

Guidance in the case of a crude oil incident

Health Canada published the information document Guidance on the Management of Crude Oil Incidents (2018), which details important information about how to deal with crude oil spills. Here are checklists on whether to evacuate or shelter in place and information on determining protective zone distances, particularly downwind of a spill from the 2016 Emergency Response Guidebook.

In case of a large spill: Consider initial downwind evacuation for at least 300 meters (1000 feet).

In case of a fire: If tank, rail car or tank truck is involved in a fire, ISOLATE for 800 meters (1/2 mile) in all directions; also, consider initial evacuation for 800 meters (1/2 mile) in all directions. Source: Petroleum crude oil hazards

Where from here?

The Byhalia Connection Pipeline is receiving considerable scrutiny, both from media sources like the Memphis Daily News and MLK50, as well as advocacy groups including Sierra Club’s Tennessee Chapter, the Southern Environmental Law Center, Memphis Community Against the Pipeline, and Protect Our Aquifer. In a move considered egregious by a vast swath of stakeholders, in early February 2021, the US Army Corps of Engineers approved a Nationwide 12 permit to fast-track the Byhalia project, effectively cutting out public comment from the process, and lightening the environmental review requirements. Because the project touches vulnerabilities in the intersection of environment, economics, health, safety, and social justice, this discussion is not likely to easily recede into the background, despite placating claims by the companies that are poised to profit.

Protests are ongoing, and just recently, on February 22, 2021, United States Congressional Representative Steve Cohen sent a direct appeal to President Biden to revoke a key permit for Byhalia, directly citing the burden the pipeline would impose on long-suffering Black neighborhoods in South Memphis. Simultaneously, the Public Works Department of Memphis is considering a resolution condemning the pipeline, and asking the Memphis Light, Gas, and Water Division to oppose the project.

This story will undoubtedly continue to evolve in the upcoming months.

The Takeaway

Regardless of where a pipeline is sited, there are inevitably risks to the environment, and to human communities living nearby. The proposed Byhalia Connection pipeline project is situated in a particularly problematic intersection where environmental justice, hydrology, geology, and risks to human and environmental health intersect. Without taking all of these factors into consideration, a potentially catastrophic cascade of impacts may ensue. Engagement and resistance to the project by the residents in the area, as well as support by advocacy groups, will hopefully result in comprehensive consideration of all the risks. Time will tell whether the project is modified, or simply defeated.

September 16, 2021 update:

References & Where to Learn More

MLK50.com maintains an archive of excellent reading materials on this controversial project that can be found here.

Topics in this Article

Pipelines | Social | Water

Data Sources in this Article

- Byhalia and Diamond Pipelines

-

Capline Pipeline

-

Coldwater National Wetlands Inventory (2-mile buffer to Byhalia)

-

Horn Lake National Wetlands Inventory (2-mile buffer to Byhalia)

-

Davis Wellhead Water Protection Zone

-

Memphis Sands Aquifer

-

Middle Clairborne Aquifer boundary

-

New Madrid Fault

-

1/2-mile buffer to Byhalia Connection Pipeline

Data layer generated in ArcGIS by FracTracker Alliance.

-

2-mile buffer to Byhalia Connection Pipeline

Data layer generated in ArcGIS by FracTracker Alliance.

-

Properties facing eminent domain

-

Private school within 2 miles of Byhalia route

-

Public school within 2 miles of Byhalia route

-

Hospital within 2 miles of Byhalia route

-

Child care facilities within 2 miles of Byhalia route

-

EMS within 2 miles of Byhalia route

-

Toxics Release Inventory sites within 2 mi of Byhalia route

-

Non-white percentage, 1/2 mile evacuation zone from Byhalia pipeline

Data downloaded 21 April 2020 from

ftp://newftp.epa.gov/EJSCREEN/2019/ by FracTracker Alliance, then reprojected into UTM, clipped, and recalculated 27 January 2021. Data originally posted by US Environmental Protection Agency on 11/8/2019.

-

Non-white percentage, 2-mile buffer to Byhalia pipeline

Data downloaded 21 April 2020 from

ftp://newftp.epa.gov/EJSCREEN/2019/ by FracTracker Alliance, then reprojected into UTM, clipped, and recalculated 27 January 2021. Data originally posted by US Environmental Protection Agency on 11/8/2019.

-

Low income percentage, 1/2 mile evacuation zone from Byhalia pipeline

Data downloaded 21 April 2020 from

ftp://newftp.epa.gov/EJSCREEN/2019/ by FracTracker Alliance, then reprojected into UTM, clipped, and recalculated 27 January 2021. Data originally posted by US Environmental Protection Agency on 11/8/2019.

-

Low income percentage, 2-mile buffer to Byhalia pipeline

Data downloaded 21 April 2020 from

ftp://newftp.epa.gov/EJSCREEN/2019/ by FracTracker Alliance, then reprojected into UTM, clipped, and recalculated 27 January 2021. Data originally posted by US Environmental Protection Agency on 11/8/2019.

-

New Madrid Fault Shake Zone