Pipeline incidents are more common, more dangerous, and more underreported than you might realize. This articles investigates a critical infrastructure system plagued by daily disasters and raises serious questions about data integrity and public safety. Read on to discover the full extent of the problem.

As of March 10, 2023, 152,796 tons of liquid waste and 2,980 tons of solid waste have been removed from the site of the train derailment in East Palestine, Ohio, to three injection wells and four hazardous waste disposal sites in Ohio, Michigan, Indiana, and Texas.

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/09/DSC_1021_LowRes__1607617394306__w1920-e1663613850641.jpg6671500Ted Auch, PhDhttps://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngTed Auch, PhD2022-09-19 15:08:172022-11-03 11:56:26Desalination: The Chemical Industry’s Demand for Water in Texas

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/11/TAuch_Plastics_Refinery_TankFarm_Terminal-Trafigura_CorpusChristiPolymers_Valero_Citgo_FlintHillsResources-CorpusChristi_TX_LightHawk_Nov2019-feature.jpg6671500Ted Auch, PhDhttps://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngTed Auch, PhD2021-11-05 09:43:472021-11-05 09:47:30Southeastern Texas Petrochemical Industry Needs 318 Billion Gallons of Water, but the US EPA Says Not So Fast

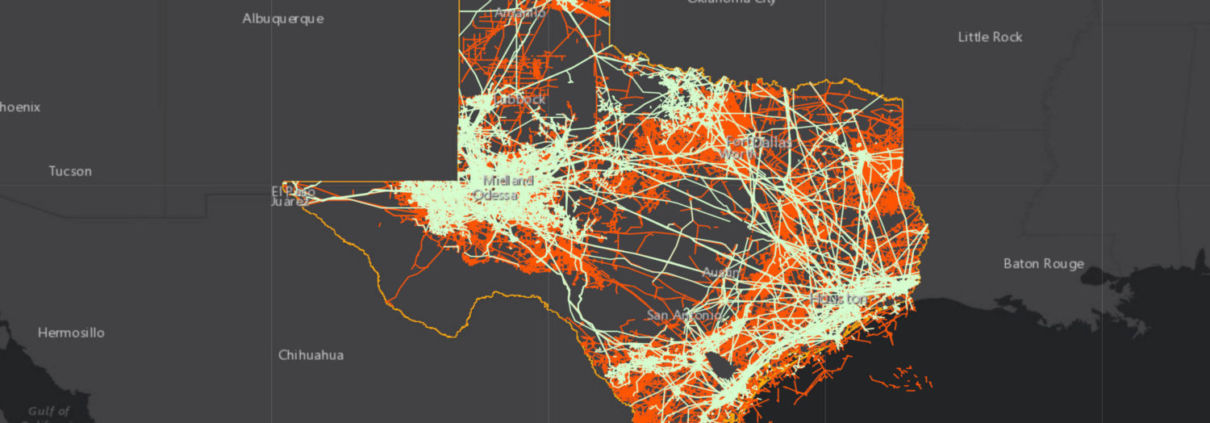

This map illustrates infrastructure networks in Texas and explores how these unseen webs connect us and improve lives, but also carry risks and burdens.

FracTracker Alliance released a new map identifying the locations of over 1,200 oil and gas wells using toxic “forever chemicals” in Arkansas, Louisiana, Oklahoma, New Mexico, Texas, and Wyoming.

A new collaboration between FracTracker Alliance and Algalita is aiming to help middle school and high school students understand the connection between plastics and fracking — and the wide ranging implications for climate change, environmental injustice, and human health.

Most young people today understand that plastics are problematic. But, there is still often a disconnect between the symptom of plastics in our oceans, and the root causes of the problem. Algalita’s mission is to empower a new generation of critical thinkers to shift the broken and unjust systems that are causing the plastic pollution crisis. Algalita’s strategy is creating educational experiences directly with the movement’s diverse leaders, and this new project with FracTracker is a perfect example.

Specifically, Algalita and FracTracker have been working together to add new lessons to Algalita’s brand-new online, gamified, action platform: Wayfinder Society. Through this program, students can guide their own exploration of the complexities of the plastics issue, and can take action at their own pace and scale, by completing lessons and action-items (called Waymarks) based on difficulty, topic, and type of impact.

The first of two FracTracker Waymarks outlines the connection between fracking and plastic production. Students explore a map showing the full plastics production process from fracking pads, to pipelines, to ethane crackers, and packaging factories.

In a second Waymark that builds off of the first, students explore the massive petrochemical buildout on the Gulf Coast and in the Ohio River Valley. The map allows students to analyze the greenhouse gas emissions predicted for this buildout using the data point pop-up boxes. They can also examine the effects of climate change on communities amongst the buildout by viewing the coastal flood zone areas in Texas and Louisiana. Beyond that, students can investigate how facilities are impacting their peers in schools close to massive ethane cracker facilities. Finally, students are introduced to the movement’s #PlasticFreePresident Campaign, giving them a direct action to apply their new knowledge.

Mapping Fracking’s Link to Plastic Production

This StoryMap was created by FracTracker for Wayfinder Society, a program by Algalita. Learn more at Algalita.org. Place your cursor over the image and scroll down to advance the StoryMap and explore a series of maps charting the fracking-for-plastic system. Click on the icon in the bottom left to view the legend. Scroll to the end of the StoryMap to learn more and access the data sources.

Algalita is excited about this partnership for so many reasons. For one, GIS is a critical skill for young people to learn. These two Waymarks pose an accessible and non-intimidating introduction to ArcGIS by using simple maps and StoryMaps like the one above. The maps let students get comfortable with GIS concepts and capabilities like layers, data attribute tables, measuring tools, and filters. Allowing students to explore how plastics are produced through a geographical lens provides a unique visual and interactive experience for them. The goal is for students to be able to connect petrochem buildout, with the plastics, climate and justice issues that they are focusing on — often separately. Our aim is that by putting this part of the story in context of real physical space they will more easily make those connections. We hope these lessons spark some students’ interest in mapping, geography, and GIS, providing a new generation of changemakers with GIS in their toolbox.

On top of that, we are stoked to be building this partnership with FracTracker because the success of our collective movement depends on strong, clear communication and synergies between the nodes of the movement’s network. The FracTracker Waymarks give our Wayfinders direct access to real-time data, visualizations, and expert insights that they can then use to level-up their actions and stories around their activism. And, they connect the dots not just for students, but also for educators and movement partners like us at Algalita — we are all for this powerful lever for change!

Check out Wayfinder Society here. Access the FracTracker Waymarks here and here— but you’ll need to be logged in. If you’re a student, get started by creating a profile, and then start earning Cairns (points)! If you’re an educator, parent or mentor, and interested in exploring the site, email us here for the guest login.

By Anika Ballent, Education Director, Algalita

Algalita empowers a new generation of critical thinkers who will shift the broken and unjust systems that are causing the plastic pollution crisis. We do this by offering educational experiences created directly with the movement’s diverse leaders.

Anika has been working in the movement against plastic pollution for ten years, studying microplastics in benthic and freshwater environments. She brings together her science background and creativity to educate young changemakers through hands-on experiences in schools, Algalita’s International Youth Summit, and online programs.

All other data points were mapped by FracTracker Alliance referencing various online sources. While this map is based on actual infrastructure, it is intended as a model of the fracking-for-plastic lifecycle and certain steps may vary in real life.

It’s been a little over a year since I visited the Texas Gulf Coast to document the oil, gas, and petrochemical landscape with our partners at LightHawk and Scott Humphries, an amazing pilot and Houston native.

Much has happened since then – in regard to and because of – the Gulf Coast’s petrochemical industry.

The fossil fuel landscape along the Gulf Coast is broad, and its impact is heavy.

The area has seen a massive build out over the last five years. New plastics and steel manufacturing facilities and pipelines from the Permian Basin that transport crude to ever-expanding tank farms and marine terminals – all with the blessings of local economic development groups and local government, despite known present and potential hazards.

As these developments continue, communities and workers pay the price. An incident in early December, 2020 left workers injured after a condensate fire at a Citgo tank farm in Corpus Christi. Before that, a pipeline explosion on August 20th in the Corpus Christi Ship Channel resulted in four deaths, with only two of those bodies recovered.

Channels of Life, below, is a short video looking at what is already on the ground, and what is on the horizon. Whether you are pleasure-boating in the channels or driving down the highway, you only see the edge of industrial sprawl that already exists. The depth of the incursion is not visible from the ground. Further down in an interactive Story Map, we give you a rare look from above, while pinpointing various incidents and facilities of concern. Partnering with LightHawk, we flew from Port Aransas, up the La Quinta Channel to the Nueces Delta, and ending at Refinery Row, giving you a bird’s-eye view of the sprawling fossil fuel landscape.

How much more industrial saturation can the Coastal Bend’s public health and ecosystem withstand before it is all sacrificed?

Is it destined to become a sacrifice zone for increasing corporate wealth and prestige?

In many parts of Texas – as well as in Louisiana and New Mexico – oil, gas, and petrochemical facilities abut schools, backyards, and playgrounds. The Gulf Coast contains 95% of the country’s ethylene capacity and roughly half of the country’s petroleum refining and natural gas processing capacity. This development has propelled a new wave of petroleum and petrochemical infrastructure in recent years. There are 129 planned or recently completed petrochemical facilities in TX and LA alone.

This buildout has enormous consequences for the country’s greenhouse gas emissions, including intensifying climate change; increasing production of (often radioactive) waste and the need for its disposal; and discharging dangerous pollution into frontline communities where health has already been compromised by industry activities.

As the sacrifice builds and the losses mount, economic development corporations advertise the area as prime real estate for more facilities and infrastructure – even as markets steadily move away from fossil fuels. Exports are a tenuous lifeline for an industry drowning in an oversupply of oil and gas, but advocates like the Port of Corpus Christi Authority insist on proposing, financing, and constructing new crude oil and liquefied natural gas (LNG) export terminals along the Gulf Coast, including the BlueWater and GulfLink terminals.

Even with access to global markets, the outlook for this Gulf Coast petrochemical expansion doesn’t look great. Countries that planned to import the US’ fossil fuels are withdrawing interest, citing climate concerns. Major projects are being abandoned, like the petrochemical facility Project Falcon that SABIC had planned to build near Aransas Pass. Frontline communities that have suffered devastating health impacts from the industry for too long are calling out environmental racism and causing major delays for new facilities.

These Texan sites are further captured in the Story Map below, as are the footprints of countless other existing and proposed petrochemical infrastructure sites, from the frac sand mines south of San Antonio down into Corpus Christi Bay, the mushrooming industry along the La Quinta Channel, up the Gulf Coast to Freeport, and finally along the always hectic Houston Ship Channel that empties out into Galveston Bay.

Left to Right: Corpus Christi native and Coastal Alliance to Protect Our Environment (CAPE) member Dewey Magee, FracTracker Alliance’s Ted Auch, and LightHawk pilot Scott Humphries stand outside Scott’s Beechcraft Bonanza A-36 at McCampbell-Porter Airport in Aransas Pass, TX, November 11th, 2019. Photo by Errol Summerlin

The View of Corpus Christi’s Petrochemical Corridor along La Quinta Channel and Tule Lake Shipping Channel from 200’ above McCampbell-Porter Airport in Aransas Pass, TX, November 11th, 2019. Photo by Ted Auch, FracTracker Alliance

I reached out to pilot and native Houstonian Scott Humphries for his thoughts on what he expected and what he gleaned from our flight. He wrote the following:

Question #1: What about our proposed flight interested you as a Texan and/or Houstonian – or just more generally – what interested you about this mission?

I’ve always tried to be environmentally conscious, and always try to have, “think globally, act locally” rummaging around in my head, but this mission (and affiliating with LightHawk generally) presented an opportunity for me to try to (hopefully) have a little more impact than just personally recycling, outlawing Styrofoam cups at our office, etc. Separately, as a longtime Houstonian, I’ve always been proud to live and work in what many refer to as the “Energy Capital of the World.” This mission seemed a useful way to do some small part to help make sure that title continues to be held responsibly.

Question #2: After conducting the flights, or as they were happening, did you learn anything, or have any thoughts that surprised you or realizations about anything particular?

I have flown along the Gulf Coast (including to/from Houston/Corpus Christi) many, many times, and if you’d asked me before this mission, I would have said, ‘Sure, there’s a decent amount of industry along that part of the coast.’ What surprised me while we were flying was two things: (1) there’s not just a decent amount of industry along that part of the coast; rather, along that route, even flying low, you’re rarely – if ever – out of sight of a significant facility of some kind, and (2) the size of the facilities – in other circumstances I’d have been flying much higher and wouldn’t get a good sense of the size of the pads. Flying as we were at just over 1000′, it was striking how massive the various plants were, both in Corpus Christi Bay and along the coast.

Another perspective on this flight and the area we flew over comes from Kevin Sims, Aransas Bay Birding Charters Operator whose Whooping Crane and Pink Spoonbill photos we feature in the story map below. Kevin has been plying the waters in and around Aransas Wildlife Refuge since 1972, and when I contacted him about using some of his photos, he told me the following:

“We need the desalination plants, but the planned discharge points are going to cripple our ecology and the business that rely on it for tourism. They could’ve discharged offshore, but instead they are discharging into the bay, and if it gets too salty the crab populations will plummet, and everything around here depends on crabs and shrimp. If we have a constant influx of brine it could really cripple us. I went to a fantastic meeting from Texas A&M, and their science told them that if red fish larvae migrated into the [Aransas Pass] shipping channel and hit a wall of salty water, they wouldn’t go further, and their population would crash. But despite these facts, they’ve chosen to discharge into the La Quinta Channel, and that is bad news! They were having fairly regular meetings on all of these proposals prior to COVID, but once COVID hit, they went all remote, and less people knew when the meetings were, and the meeting details weren’t widely disseminated … So, the next thing we knew, everything was passed, and they’re gonna [sic] go ahead and do [all of] it.

My perspective comes from a lifetime of fishing and observing the Whooping Crane, and watching them progress from 157 eighteen years ago, to 507 at the present time. Well, I feel this will threaten an endangered species that they’ve been trying to bring back from the brink of extinction since the 1940s. I can remember my dad showing me the cranes in the mid-70s, and there were only 52-55. All of the projects you are mapping have the potential to decimate all the progress made, not to mention money spent on Whooping Crane recovery. From my perspective, it’s a catch-22, ‘cause [sic] the big cities take the water out of the river, and they don’t have the inflows into the bays that they did in the past. We also don’t have the rains that we used to have. The desalination plants would relieve some of that pressure if they would just put that brine offshore. The other species of concern to my industry is the Pink Spoonbills, but the Whooping Crane is the main draw.”

Channels of Life: The Gulf Coast Buildout in TX

A Story Map

This Story Map illustrates the impacts of oil and gas infrastructure from San Antonio down to Corpus Christi, and then up the Gulf Coast to Houston.

The map displays aerial photographs of infrastructure, from frac sand mines and refineries, to chemical plants and offshore drill rig construction sites. This map includes CO2 emissions from oil and gas infrastructure from 2010 – 2018 (weighted by total CO2 during this period in orange), and/or oil refineries and their myriad products (weighted by capacity in black [barrels/day oil equivalents]).

The Story Map also presents detailed information and locations for proposed petrochemical infrastructure in the Corpus Christi Bay region, courtesy of Errol Summerlin and our partners at Coastal Alliance to Protect Our Environment (CAPE). These proposals include dredging projects needed to accommodate more traffic from larger tanker ships, as well as desalination facilities that would collectively intake 758 million gallons of Corpus Christi Bay water each day, and discharge 507 million gallons of brine per day, with an average of 95 and 64 million gallons of desalinated water produced daily, respectively.

The perforated yellow line is the flight path we took with our LightHawk partners. When the viewer scrolls into any given region, they will see SkyTruth incident alerts within five miles of our flight path. The two examples cited at the beginning of this article are just a couple of the nearly 760 such incidents in just the Corpus Christi Shipping Channel since 2011, according to data provided by SkyTruth.

The most recent data in this map is Whooping Crane locations and number counts in TX as of November 2020, courtesy of The Cornell Lab of Ornithology’s eBird data portal. This data speaks to the concerns of Mr. Sims and many of his colleagues who rely on the Whooping Crane’s attraction to birders internationally, and it also highlights that the projects photographed and in the works across Corpus Christi Bay will not just negatively affect the human communities, but will have far reaching impacts on the ecosystems of the western Gulf, and the industries that have relied on these ecosystems for all manner of ecosystems services.

Decades of oil and gas development have created a dependency on extractive industries, which has in turn hindered community health and stability.

The Port of Corpus Christi’s controversial dock expansion and Harbor Bridge replacement project at the southern end of Refinery Row has taken over community land and eclipsed their fight to protect their neighborhoods and their public health. Even after an environmental review, the preferred route cuts through these neighborhoods that are surrounded by industry, interstates, and waste treatment facilities – isolated from other residences, and subjected to heavy pollution, noise, and constant hazard.

But with interest and investments declining in the fossil fuel industry and overproduction keeping prices low, the future of the Gulf Coast, its people, environment, and industrial landscape is uncertain – but resistance to extractive industry is strong.

Several activists and environmental coalitions are fighting this project and the industrial onslaught for the health of their communities. For more information on how to support their vision, visit our friends at Coastal Alliance to Protect our Environment (CAPE) and Texas Environmental Justice Advocacy Services (TEJAS).

Thank You

This video, Story Map and article were produced with much gratitude and appreciation for our partners at LightHawk, as well as the support and resources of Scott Humphries, Kevin Sims, and Errol Summerlin.

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2020/12/TAuch_Infrastructure-Refinery-BritishPetroleum-TexasCity_TX_LightHawk_Nov2019-Feature-scaled.jpg6671500Ted Auch, PhDhttps://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngTed Auch, PhD2020-12-23 16:23:392021-04-15 14:16:01Channels of Life: The Gulf Coast Buildout in Texas

By Ted Auch, PhD, Great Lakes Program Coordinator and Shannon Smith, Manager of Communications & Development

The oil and gas industry continues to use rhetoric focusing on national security and energy independence in order to advocate for legislation to criminalize climate activists. Backlash against protestors and environmental stewards has only increased since the onset of COVID-19, suggesting that industry proponents are exploiting this public health crisis to further their own dangerous and controversial policies.[1]

Industry actors contributing to the wave of anti-protest bills include American Petroleum Institute (API), IHS Markit, The American Fuel & Petrochemical Manufacturers (AFPM), and most effectively, the American Legislative Exchange Council (ALEC), by way of its primary financial backer, Koch Industries (Fang, 2014, Shelor, 2017).

ALEC is the source of the model legislation “Critical Infrastructure Protection Act” of 2017, intended to make it a felony to “impede,” “inhibit,” “impair,” or “interrupt” critical infrastructure operation and/or construction. Close approximations – if not exact replicas – of this legislative template have been passed in 11 hydrocarbon rich and/or pathway states, and 8 more are being debated in 4 additional states.

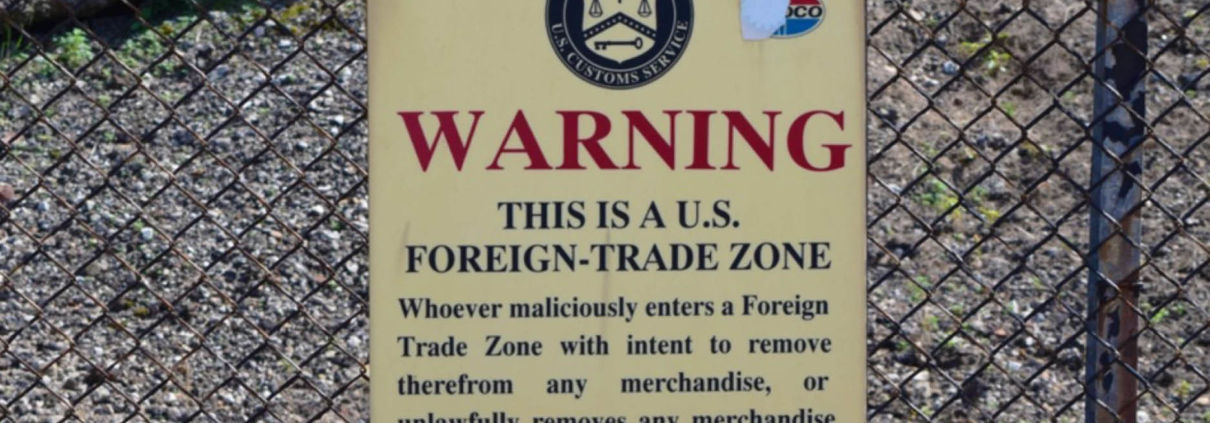

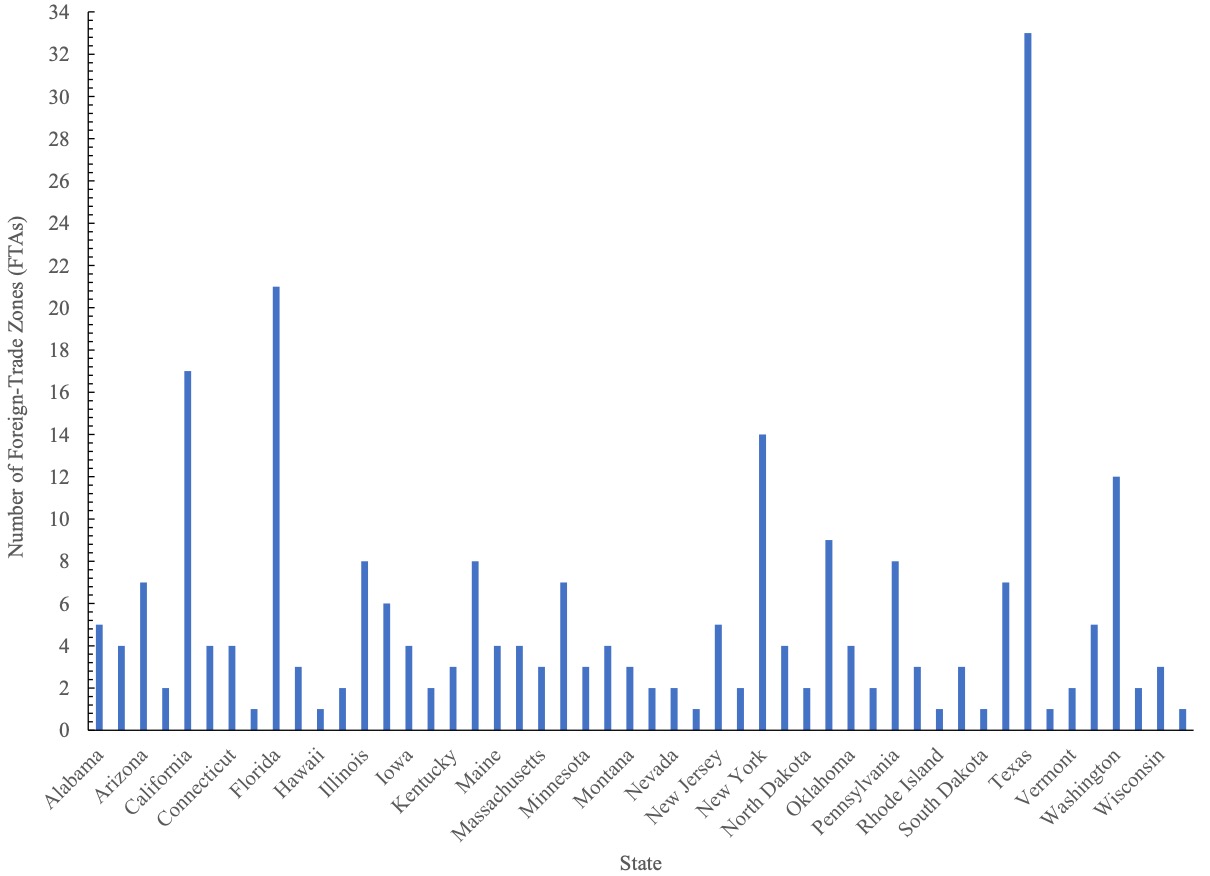

The “critical infrastructure” designation in ALEC’s “Critical Infrastructure Protection Act” is extremely broad, including over 70 pieces of infrastructure, from wastewater treatment and well pads, to ports and pipelines. However, along with the 259 Foreign Trade Zones (FTZ) (Figures 1 and 4) supervised by US Customs and Border Protection (CBP), security is of such importance because over 50% of this infrastructure is related to oil and gas. According to our analysis, there are more than 8,000 unique pieces of infrastructure that fall under this designation, with over 10% in the Marcellus/Utica states of Ohio, West Virginia, and Pennsylvania. See Figure 1 for the number of FTZ per state.

Regarding FTZ, the US Department of Homeland Security doesn’t attempt to hide their genuine nature, boldly proclaiming them “… the United States’ version of what are known internationally as free-trade zones … to serve adequately ‘the public interest’.” If there remains any confusion as to who these zones are geared toward, the US Department of Commerce’s International Administration (ITA) makes the link between FTZ and the fossil fuel industry explicit in its FTZ FAQ page, stating “The largest industry currently using zone procedures is the petroleum refining industry.” (Figure 2)

Figure 1. Number of Foreign-Trade Zones (FTZ) by state as of June 2020.

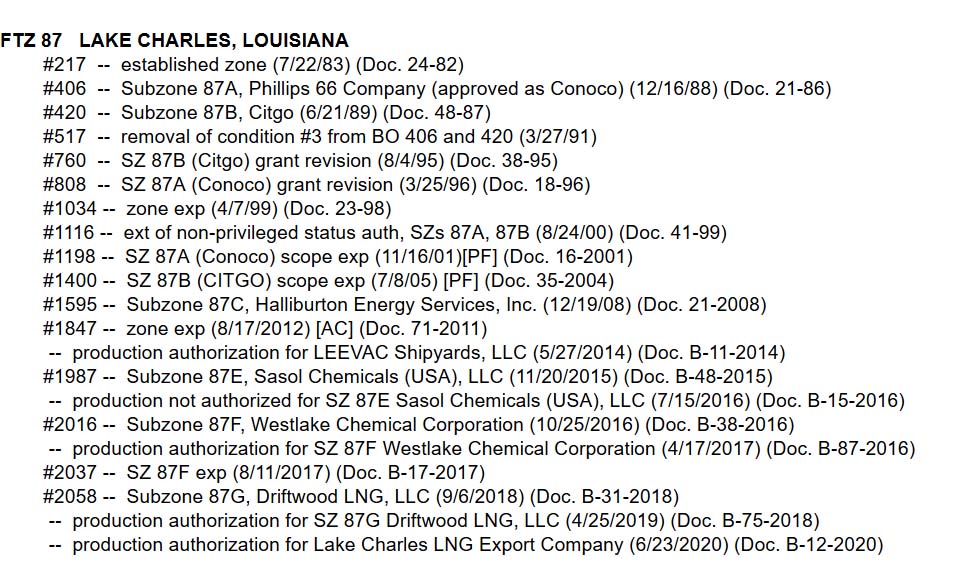

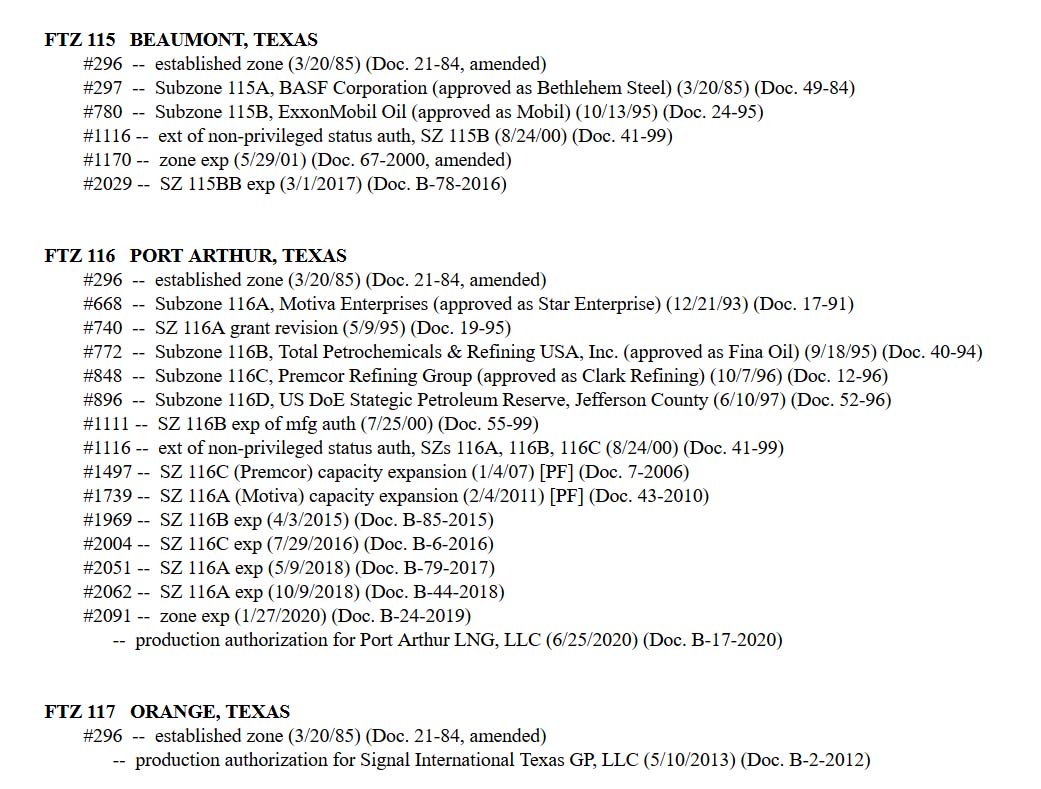

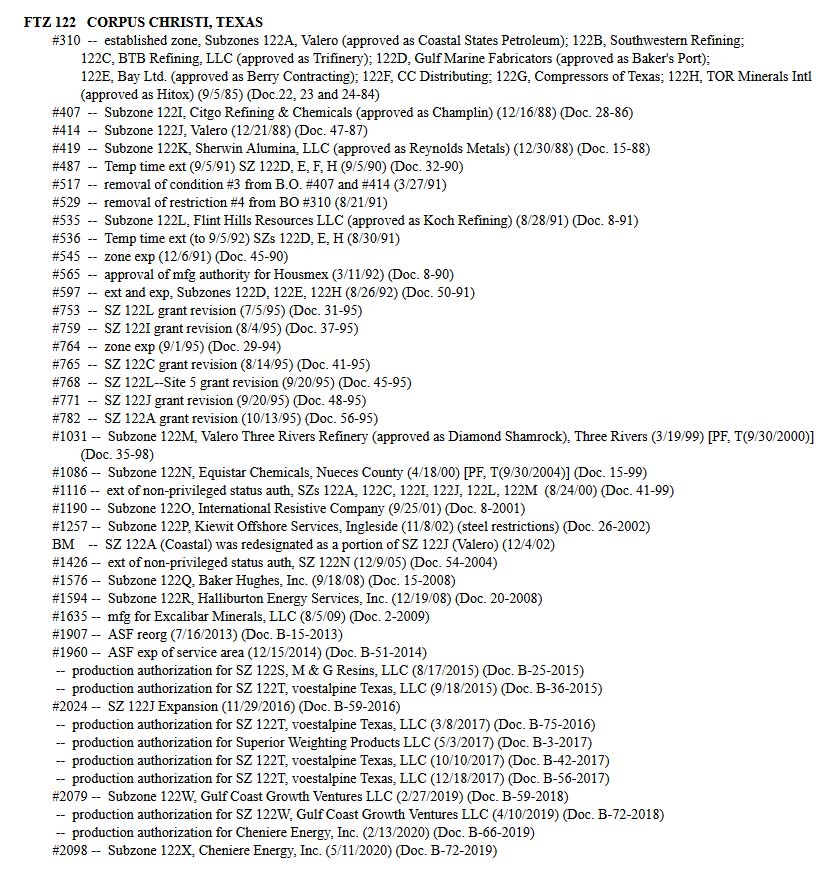

Figure 2. Foreign-Trade Zone (FTZ) Board of Actions in Zones 87 in Lake Charles, LA, 115-117 in and around Port Arthur, TX, and 122 in Corpus Christi, TX. (click on the images to enlarge)

Foreign-Trade Zone (FTZ) Board of Actions in Zone 87 in Lake Charles, Louisiana

Foreign-Trade Zone (FTZ) Board of Actions in Zones 115-117 in and around Port Arthur, Texas

Foreign-Trade Zone (FTZ) Board of Actions in Zone 122 in Corpus Christi, Texas

Much of the oil, gas, and petrochemical industries’ efforts stem from the mass resistance to the Dakota Access Pipeline (DAPL). Native American tribes and environmental groups spent months protesting the environmentally risky $3.78 billion dollar project, which began production in June 2017, after Donald Trump signed an executive order to expedite construction during his first week in office. The Standing Rock Sioux tribe also sued the US government in a campaign effort to protect their tribal lands. The world watched as Energy Transfer Partners (ETP), the company building the pipeline, destroyed Native artifacts and sacred sites, and as police deployed tear gas and sprayed protesters with water in temperatures below freezing.

ETP’s bottom line and reputation were damaged during the fight against DAPL. Besides increasingly militarized law enforcement, the oil and gas industry has retaliated by criminalizing similar types of protests against fossil fuel infrastructure. However, the tireless work of Native Americans and environmental advocates has resulted in a recent victory in March 2020, when a federal judge ordered a halt to the pipeline’s production and an extensive new environmental review of DAPL.

Just days ago, on July 6, 2020, a federal judge ruled that DAPL must shut down until further environmental review can assess potential hazards to the landscape and water quality of the Tribe’s water source. This is certainly a victory for the Standing Rock Sioux Tribe and other environmental defenders, but the decision is subject to appeal.

Since the DAPL conflict began, the industry has been hastily coordinating state-level legislation in anticipation of resistance to other notable national gas transmission pipelines, more locally concerning projects like Class II Oil and Gas Waste Injection Wells, and miles of gas gathering pipelines that transport increasing streams of waste – as well as oil and gas – to coastal processing sites.

The following “critical infrastructure” bills have already been enacted:

STATE

BILL

TITLE

DATE PASSED

West Virginia

HB 4615

NEW PENALTIES FOR PROTESTS NEAR GAS AND OIL PIPELINES

3/25/20

South Dakota

SB 151

NEW PENALTIES FOR PROTESTS NEAR PIPELINES AND OTHER INFRASTRUCTURE

3/18/20

Kentucky

HB 44

NEW PENALTIES FOR PROTESTS NEAR PIPELINES AND OTHER INFRASTRUCTURE

3/16/20

Wisconsin

AB 426

NEW PENALTIES FOR PROTESTS NEAR GAS AND OIL PIPELINES

11/21/19

Missouri

HB 355

NEW PENALTIES FOR PROTESTS NEAR GAS AND OIL PIPELINES

7/11/19

Texas

HB 3557

NEW CRIMINAL AND CIVIL PENALTIES FOR PROTESTS AROUND CRITICAL INFRASTRUCTURE

6/14/19

Tennessee

SB 264

NEW PENALTIES FOR PROTESTS NEAR GAS AND OIL PIPELINES

5/10/19

Indiana

SB 471

NEW PENALTIES FOR PROTESTS NEAR CRITICAL INFRASTRUCTURE

5/6/19

North Dakota

HB 2044

HEIGHTENED PENALTIES FOR PROTESTS NEAR CRITICAL INFRASTRUCTURE

4/10/19

Louisiana

HB 727

HEIGHTENED PENALTIES FOR PROTESTING NEAR A PIPELINE

5/30/18

Oklahoma

HB 1123

NEW PENALTIES FOR PROTESTS NEAR CRITICAL INFRASTRUCTURE

5/3/17

There are an additional eight bills proposed and under consideration in these six states:

STATE

PENDING

TITLE

DATE PROPOSED

Louisiana

HB 197

NEW PENALTIES FOR PROTESTS NEAR CRITICAL INFRASTRUCTURE

2/24/20

Minnesota

HF 3668

NEW PENALTIES FOR PROTESTS NEAR GAS AND OIL PIPELINES

2/24/20

Mississippi

HB 1243

NEW PENALTIES FOR PROTESTS NEAR CRITICAL INFRASTRUCTURE

2/19/20

Alabama

SB 45

NEW PENALTIES FOR PROTESTS NEAR GAS AND OIL PIPELINES

2/4/20

Minnesota

HF 2966

NEW PENALTIES FOR PROTESTS NEAR OIL AND GAS PIPELINES

1/31/20

Minnesota

SF 2011

NEW PENALTIES FOR PROTESTS NEAR GAS AND OIL PIPELINES

3/4/19

Ohio

SB 33

NEW PENALTIES FOR PROTESTS NEAR CRITICAL INFRASTRUCTURE

2/12/19

Illinois

HB 1633

NEW PENALTIES FOR PROTESTS NEAR CRITICAL INFRASTRUCTURE

1/31/19

Desperate Backlash Against Peaceful Protest

Activists and organizations like the American Civil Liberties Union (ACLU) are framing their opposition to such legislation as an attempt to stave off the worst Orwellian instincts of our elected officials, whether they are in Columbus or Mar-a-Lago. On the other hand, industry and prosecutors are framing these protests as terroristic acts that threaten national security, which is why sentencing comes with a felony conviction and up to ten years in prison. The view of the FBI’s deputy assistant director and top official in charge of domestic terrorism John Lewis is that, “In recent years, the Animal Liberation Front and the Earth Liberation Front have become the most active, criminal extremist elements in the United States … the FBI’s investigation of animal rights extremists and ecoterrorism matters is our highest domestic terrorism investigative priority.”

It shocked many when last week, two protesters in the petrochemical-laden “Cancer Alley” region of Louisiana were arrested and charged under the state’s felony “terrorist” law. Their crime? Placing boxes of nurdles – plastic pellets that are the building blocks of many single-use plastic products – on the doorsteps of fossil fuel lobbyists’ homes. To make matters more ridiculous, the nurdles were illegally dumped by the petrochemical company Formosa Plastics.[2] This is outrageous indeed, but is the sort of legally-sanctioned oppression that fossil fuel industry lobbyists have been successfully advocating for years.

American Fuel & Petrochemical Manufacturers (AFPM) stated in a letter of support for ALEC’s legislative efforts:

“In recent years, there has been a growing and disturbing trend of individuals and organizations attempting to disrupt the operation of critical infrastructure in the energy, manufacturing, telecommunications, and transportation industries. Energy infrastructure is often targeted by environmental activists to raise awareness of climate change and other perceived environmental challenges. These activities, however, expose individuals, communities, and the environment to unacceptable levels of risk, and can cause millions of dollars in damage … As the private sector continues to expand and maintain the infrastructure necessary to safely and reliably deliver energy and other services to hundreds of millions of Americans, policymakers should continue to consider how they can help discourage acts of sabotage … Finally, it will also hold organizations both criminally and vicariously liable for conspiring with individuals who willfully trespass or damage critical infrastructure sites.”

Those organizations deemed ‘criminally and vicariously liable’ would in some states face fines an order of magnitude greater than the actual individual, which would cripple margin-thin environmental groups around the country, and could amount to $100,000 to $1,000,000. The AFPM’s senior vice president for federal and regulatory affairs Derrick Morgan referred to these vicarious organizations as “inspiring … organizations who have ill intent, want to encourage folks to damage property and endanger lives …”

One of the most disturbing aspects of this legislation is that it could, according to the testimony and additional concerns of ACLU of Ohio’s Chief Lobbyist Gary Daniels, equate “‘impeding’ and ‘inhibiting’ the ‘operations’ of a critical infrastructure site” with acts as innocuous as Letters to the Editor, labor strikes or protests, attending and submitting testimony at hearings, or simply voicing your concern or objections to the validity of industry claims and its proposals with emails, faxes, phone calls, or a peaceful protest outside critical infrastructure that raises the concern of site security. Mr. Daniels noted in his additional written testimony that the latter, “may prove inconvenient to the site’s staff, under SB 250 they would be an F3 [Third Degree Felony], and that is without someone even stepping foot on or near the property, as physical presence is not required to be guilty of criminal mischief, as found in/defined in Sec. 2907.07(A)(7) of the bill.”

Figure 3. A rally held by the Louisiana-based nonprofit RISE St. James.

This connection, when enshrined into law, will have a chilling effect on freedom of speech and assembly, and will stop protests or thoughtful lines of questioning before they even start. As the Ohio Valley Environmental Coalition (OVEC) put it in their request for residents to ask the governor to veto the now-enacted HB 4615, such a bill is unnecessary, duplicative, deceitful, un-American, unconstitutional, and “will further crowd our jails and prisons.”

To combat such industry-friendly legislation that erodes local government control in Ohio, lawmakers like State Senator Nikki Antonio are introducing resolutions like SR 221, which would, “abolish corporate personhood and money-as-speech doctrine” made law by the Supreme Court of the United States’ rulings in Citizens United v. FEC and Buckley v. Valeo. After all, the overarching impact of ALEC’s efforts and those described below furthers privatized, short-term profit and socialized, long-term costs, and amplifies the incredibly corrosive Citizen’s United decision a little over a decade ago.

Further Criminalization of Protest, Protections for Law Enforcement

Simultaneously, there is an effort to criminalize protest activities through “riot boosting acts,” increased civil liability and decreased police liability, trespassing penalties, and new sanctions for protestors who conceal their identities (by wearing a face mask, for example).

The following bills have already been enacted:

STATE

BILL

TITLE

DATE PASSED

South Dakota

SB 189

EXPANDED CIVIL LIABILITY FOR PROTESTERS AND PROTEST FUNDERS

3/27/19

West Virginia

HB 4618

ELIMINATING POLICE LIABILITY FOR DEATHS WHILE DISPERSING RIOTS AND UNLAWFUL ASSEMBLIES

3/10/18

North Dakota

HB 1426

HEIGHTENED PENALTIES FOR RIOT OFFENCES

2/23/17

North Dakota

HB 1293

EXPANDED SCOPE OF CRIMINAL TRESPASS

2/23/17

North Dakota

HB 1304

NEW PENALTIES FOR PROTESTERS WHO CONCEAL THEIR IDENTITY

2/23/17

In addition, the following bills have been proposed and are under consideration:

STATE

PENDING

TITLE

DATE PROPOSED

Rhode Island

H 7543

NEW PENALTIES FOR PROTESTERS WHO CONCEAL THEIR IDENTITY

2/12/20

Oregon

HB 4126

HARSH PENALTIES FOR PROTESTERS WHO CONCEAL THEIR IDENTITY

1/28/20

Tennessee

SB 1750

NEW PENALTIES FOR PROTESTERS WHO CONCEAL THEIR IDENTITY

1/21/20

Ohio

HB 362

NEW PENALTIES FOR PROTESTERS WHO CONCEAL THEIR IDENTITY

10/8/19

Pennsylvania

SB 887

NEW PENALTIES FOR PROTESTS NEAR “CRITICAL INFRASTRUCTURE”

10/7/19

Massachusetts

HB 1588

PROHIBITION ON MASKED DEMONSTRATIONS

1/17/19

All the while, the Bundy clan of Utah pillage – and at times – hold our public lands hostage, and white male Michiganders enter the state capital in Lansing armed for Armageddon, because they feel that COVID-19 is a hoax. We imagine that it isn’t these types of folks that West Virginia State Representatives John Shott and Roger Hanshaw had in mind when they wrote and eventually successfully passed HB 4618, which eliminated police liability for deaths while dispersing riots and unlawful assemblies.

Contrarily, South Dakota’s SB 189, or “Riot Boosting Act,” was blocked by the likes of US District Judge Lawrence L. Piersol, who wrote:

“Imagine that if these riot boosting statutes were applied to the protests that took place in Birmingham, Alabama, what might be the result? … Dr. King and the Southern Christian Leadership Conference could have been liable under an identical riot boosting law.”

FracTracker collaborated with Crude Accountability on a report documenting increasing reprisals against environmental activists in the US and Eurasia. Read the Report.

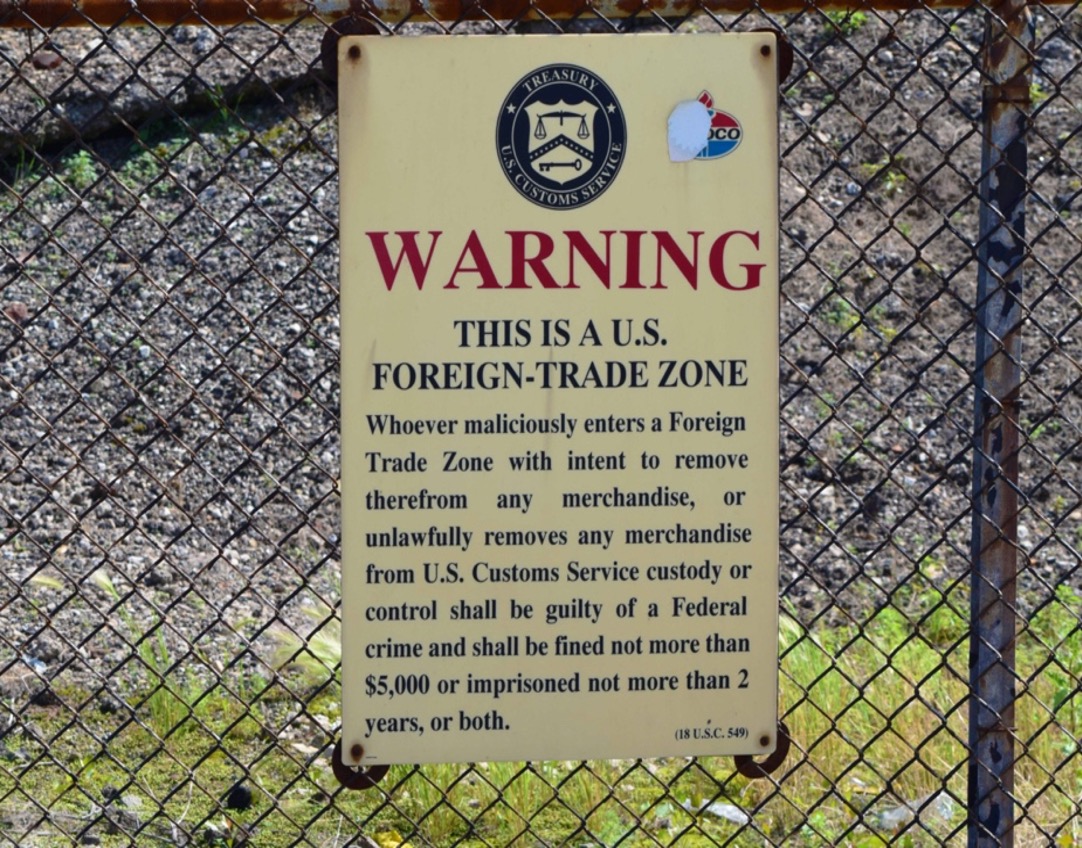

Figure 4. Photo of US Treasury Department signage outlining the warning associated with BP’s Whiting, IN, oil refinery designated a Foreign Trade Zone (FTZ). Photo by Ted Auch July 15th, 2015

In all fairness to Mr. Emanuel, he was referring to the Obama administration’s support for the post-2008 bipartisan Wall Street bailout. However, it is critical that we acknowledge the push for critical infrastructure legislation has been most assuredly bipartisan, with Democratic Governors in Kentucky, Louisiana, and Wisconsin signing into law their versions on March 16th of this year, in May of 2018, and in November of 2019, respectively.

Related Legislation in Need of Immediate Attention

In Columbus, Ohio, there are several pieces of legislation being pushed in concert with ALEC-led efforts. These include the recently submitted HB 362, that would “create the crime of masked intimidation.” Phil Plummer and George F. Lang sponsor the bill, with the latter being the same official who introduced HB 625, a decidedly anti-local control bill that would preempt communities from banning plastic bags. Most of the general public and some of the country’s largest supermarket chains have identified plastic bag bans as a logical next step as they wrestle with their role in the now universally understood crimes plastics have foisted on our oceans and shores. As Cleveland Scene’s Sam Allard wrote, “bill mills” and their willing collaborators in states like Ohio cause such geographies to march “boldly, with sigils flying in the opposite direction” of progress, and a more renewable and diversified energy future.

With respect to Plummer and Lang’s HB 362, two things must be pointed out:

1) It is eerily similar to North Dakota’s HB 1304 that created new penalties for protestors who conceal their identity, and

So, when elected officials as far away as Columbus copy and paste legislation passed in the aftermath of the DAPL resistance efforts, it is clear the message they are conveying, and the audience(s) they are trying to intimidate.

Plummer and Lang’s HB 362 would add a section to the state’s “Offenses Against the Public Peace,” Chapter 2917, that would in part read:

No person shall wear a mask or disguise in order to purposely do any of the following:

(A) Obstruct the execution of the law;

(B) Intimidate, hinder, or interrupt a person in the performance of the person’s legal duty; or

(C) Prevent a person from exercising the rights granted to them by the Constitution or the laws of this state.

Whoever violates this proposed section is guilty of masked intimidation. Masked intimidation is a first degree misdemeanor. It was critical for the DAPL protestors to protect their faces during tear gas and pepper spray barrages, from county sheriffs and private security contractors alike.

At the present moment, masks are one of the few things standing between COVID-19 and even more death. Given these realities, it is stunning that our elected officials have the time and/or interest in pushing bills such as HB 362 under the thin veil of law and order.

But judging by what one West Virginia resident and former oil and gas industry draftsman,[3] wrote to us recently, elected officials do not really have much to lose, given how little most people think of them:

“Honestly, it doesn’t seem to matter what we do. The only success most of us have had is in possibly slowing the process down and adding to the cost that the companies incur. But then again, the increase in costs probably just gets passed down to the consumers. One of the biggest drawbacks in my County is that most, if not all, of the elected officials are pro drilling. Many of them have profited from it.”

The oil, gas, and petrochemical industries are revealing their weakness by scrambling to pass repressive legislation to counteract activists. But social movements around the world are determined to address interrelated social and environmental issues before climate chaos renders our planet unlivable, particularly for those at the bottom of the socioeconomic ladder. We hope that by shining a light on these bills, more people will become outraged enough to join the fight against antidemocratic legislation.

This is Part I of a two-part series on concerning legislation related to the oil, gas, and petrochemical industries. Part II focuses on bills that would weaken environmental regulations in Ohio, Michigan, and South Dakota.

By Ted Auch, PhD, Great Lakes Program Coordinator and Shannon Smith, Manager of Communications & Development

[1] See Naomi Klein’s concept of the Shock Doctrine for similar trends.

[2] The community-based environmental organization RISE St. James has been working tirelessly to prevent Formosa Plastics from building one of the largest petrochemical complexes in the US in their Parish. Sharon Lavigne is a leading member of RISE St. James, and is an honored recipient of the 2019 Community Sentinel Award for Environmental Stewardship. Read more on Sharon’s work with RISE St. James here.

[3] This individual lives in Central West Virginia, and formerly monitored Oil & Gas company assets in primarily WV, PA, NY, VA, MD & OH, as well as the Gulf Coast. Towards the end of this individual’s career, they provided mapping support for the smart pigging program, call before you dig, and the pipeline integrity program.

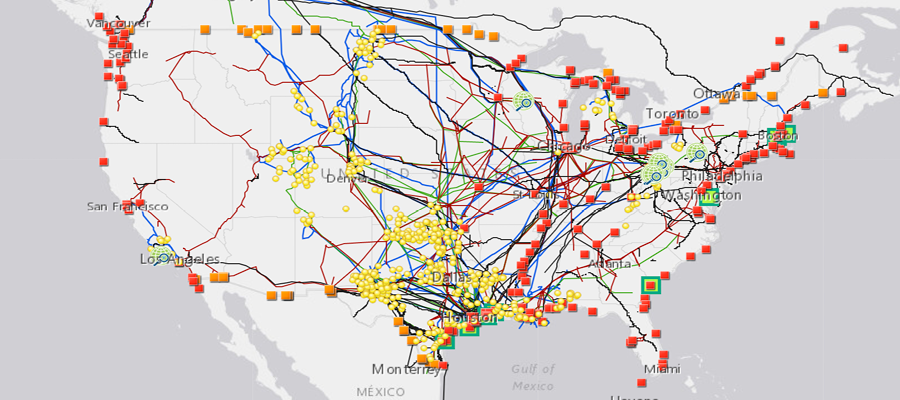

FracTracker Alliance has released a new national map, filled with energy and petrochemical data. Explore the map, continue reading to learn more, and see how your state measures up!

This map has been updated since this blog post was originally published, and therefore statistics and figures below may no longer correspond with the map

The items on the map (followed by facility count in parenthesis) include:

For oil and gas wells, view FracTracker’s state maps.

Transportation & Storage

Natural gas compressor stations (1,367) – Facilities built along a pipeline route that pressurize natural gas to keep it flowing through the pipeline.

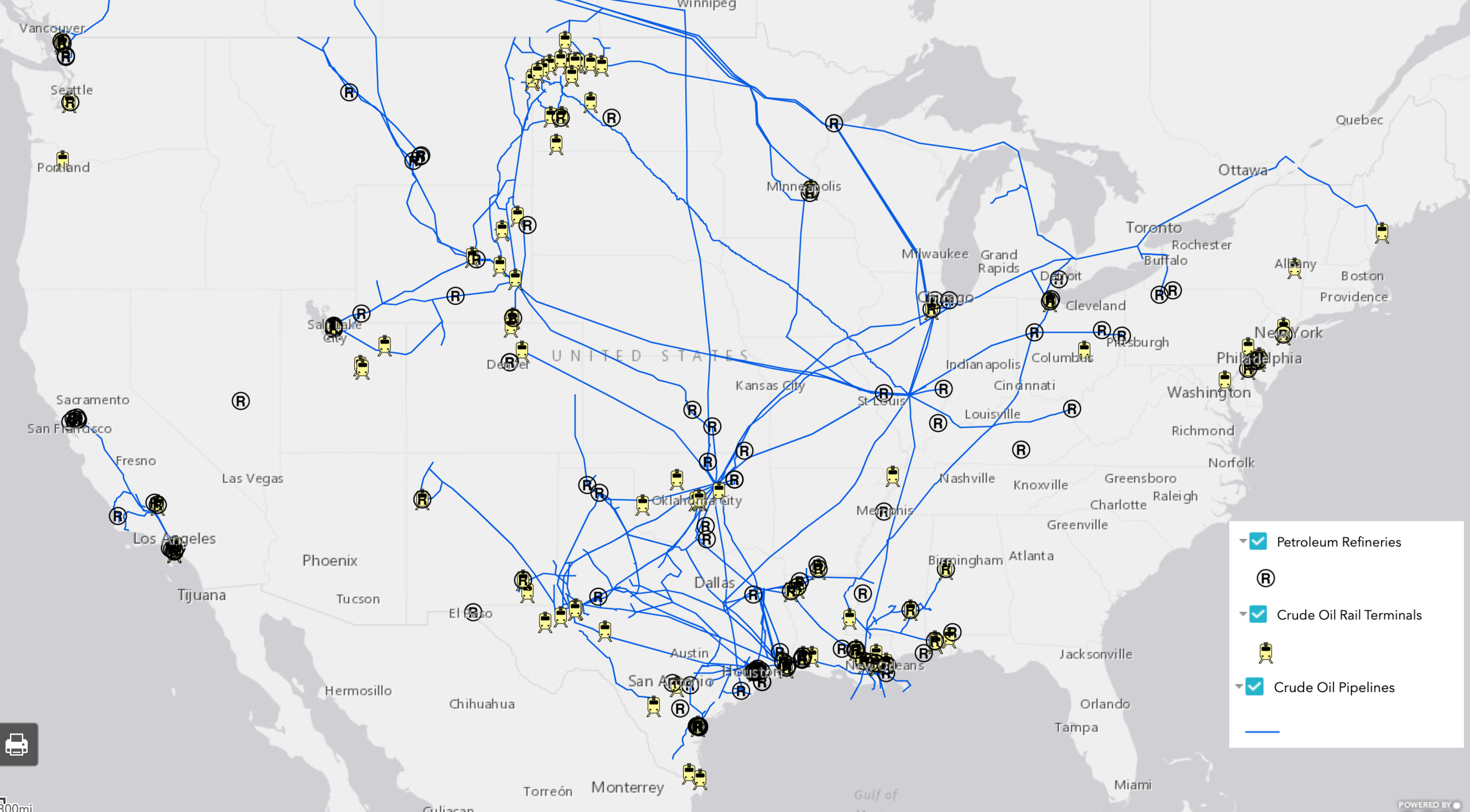

Crude oil rail terminals (94) – Rail terminals that load and unload crude oil (liquid hydrocarbons that have yet to be processed into higher-value petroleum products).

Liquefied natural gas import/export terminals (8) – Facilities that can a) liquefy natural gas so it can be exported as LNG (liquefied natural gas) and/or b) re-gasify LNG so it can be used as natural gas. Natural gas is transported in a liquid state because it takes up less space as a liquid than as a gas.

Natural Gas Underground Storage (486) – Locations where natural gas is stored underground in aquifers, depleted gas fields, and salt formations.

Petroleum Product Terminals (1,484) – Terminals with a storage capacity of 50,000 barrels or more and/or the ability to receive volumes from tanker, barge, or pipeline. Petroleum products include products “produced from the processing of crude oil and other liquids at petroleum refineries, from extraction of liquid hydrocarbons at natural gas processing plants, and from production of finished petroleum products at blending facilities.”

Petroleum Ports (242) – A port that can import and/or export 200,000 or more short tons of petroleum products a year.

Natural gas import/export pipeline facility (54) – A facility where natural gas crosses the border of the continental United States.

Pipelines

Crude oil pipelines – major crude oil pipelines, including interstate truck lines and selected intrastate lines, but not including gathering lines.

Natural gas liquid pipelines – Also referred to as hydrocarbon gas liquid pipelines, they carry the heavier components of the natural gas stream which are liquid under intense pressure and extreme cold, but gas in normal conditions.

Natural gas pipelines– Interstate and intrastate natural gas pipelines. Due to the immensity of this pipeline network and lack of available data, this pipeline layer in particular varies in degree of accuracy.

Petroleum Product Pipelines – Major petroleum product pipelines.

Recent Pipeline Projects – Pipeline projects that have been announced since 2017. This includes projects in various stages, including under construction, complete, planned or canceled. Click on the pipeline for the status.

Processing & Downstream

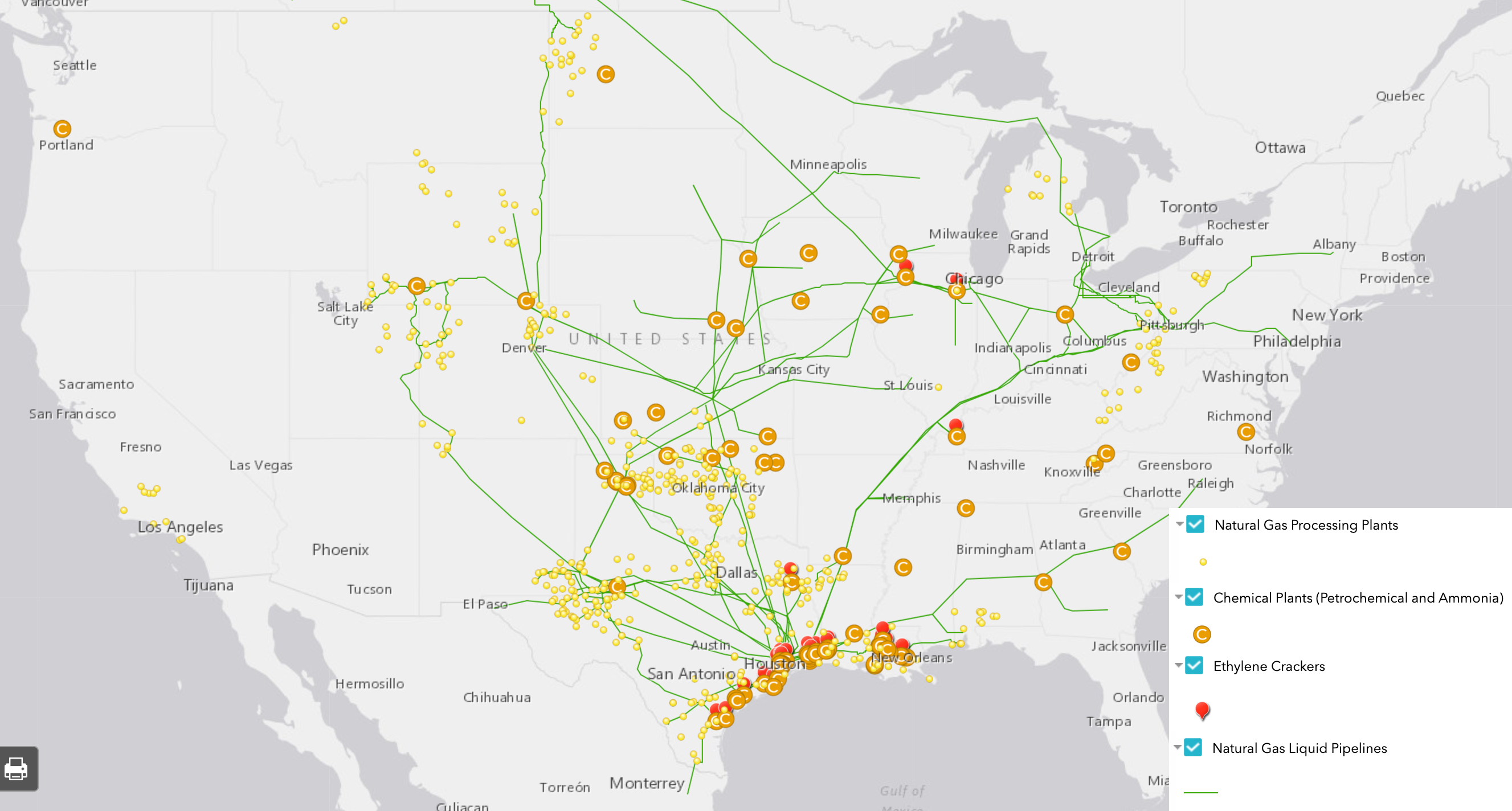

Natural Gas Processing Plants (478) – Plants that separate impurities and components of the natural gas stream.

Chemical plants (36) – Includes two types of chemical plants – petrochemical production and ammonia manufacturing – that report to EPA’s Greenhouse Gas Reporting Program.

Ethylene Crackers (30) – Also referred to as ethane crackers, these petrochemical complexes that converts ethane (a natural gas liquid) into ethylene. Ethylene is used to make products like polyethylene plastic.

Petroleum Refineries (135) – A plant that processes crude oil into products like petroleum naphtha, diesel fuel, and gasoline.

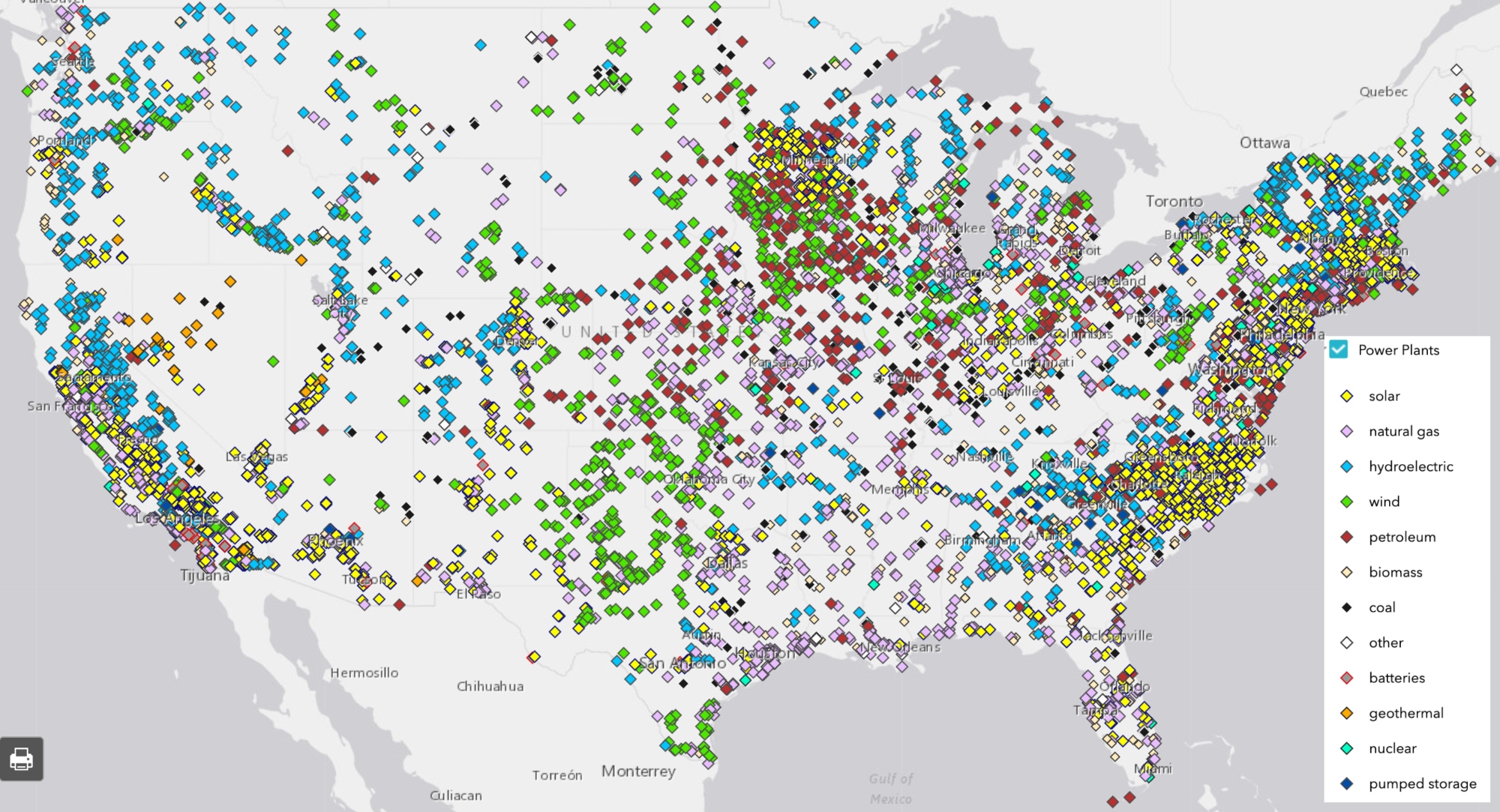

Power Plants (9,414) – Electric generating plants with a capacity of at least one megawatt, sorted by energy source.

Wind Turbines (63,003) – Zoom in on wind power plants to see this legend item appear.

Natural Resources

Shale Plays (45) – Tight oil and gas shale plays, which are formations where oil and gas can be extracted.

Major Rivers

Solar Energy Potential – Potential solar energy generation, in kilowatt-hours per square meter per day – averaged annually.

This map is by no means exhaustive, but is exhausting. It takes a lot of infrastructure to meet the energy demands from industries, transportation, residents, and businesses – and the vast majority of these facilities are powered by fossil fuels. What can we learn about the state of our national energy ecosystem from visualizing this infrastructure? And with increasing urgency to decarbonize within the next one to three decades, how close are we to completely reengineering the way we make energy?

Key Takeaways

Natural gas accounts for 44% of electricity generation in the United States – more than any other source. Despite that, the cost per megawatt hour of electricity for renewable energy power plants is now cheaper than that of natural gas power plants.

The state generating the largest amount of solar energy is California, while wind energy is Texas. The state with the greatest relative solar energy is not technically a state – it’s D.C., where 18% of electricity generation is from solar, closely followed by Nevada at 17%. Iowa leads the country in relative wind energy production, at 45%.

The state generating the most amount of energy from both natural gas and coal is Texas. Relatively, West Virginia has the greatest reliance on coal for electricity (85%), and Rhode Island has the greatest percentage of natural gas (92%).

With 28% of total U.S. energy consumption for transportation, many of the refineries, crude oil and petroleum product pipelines, and terminals on this map are dedicated towards gasoline, diesel, and other fuel production.

Petrochemical production, which is expected to account for over a third of global oil demand growth by 2030, takes the form of chemical plants, ethylene crackers, and natural gas liquid pipelines on this map, largely concentrated in the Gulf Coast.

Electricity generation

The “power plant” legend item on this map contains facilities with an electric generating capacity of at least one megawatt, and includes independent power producers, electric utilities, commercial plants, and industrial plants. What does this data reveal?

In terms of the raw number of power plants – solar plants tops the list, with 2,916 facilities, followed by natural gas at 1,747.

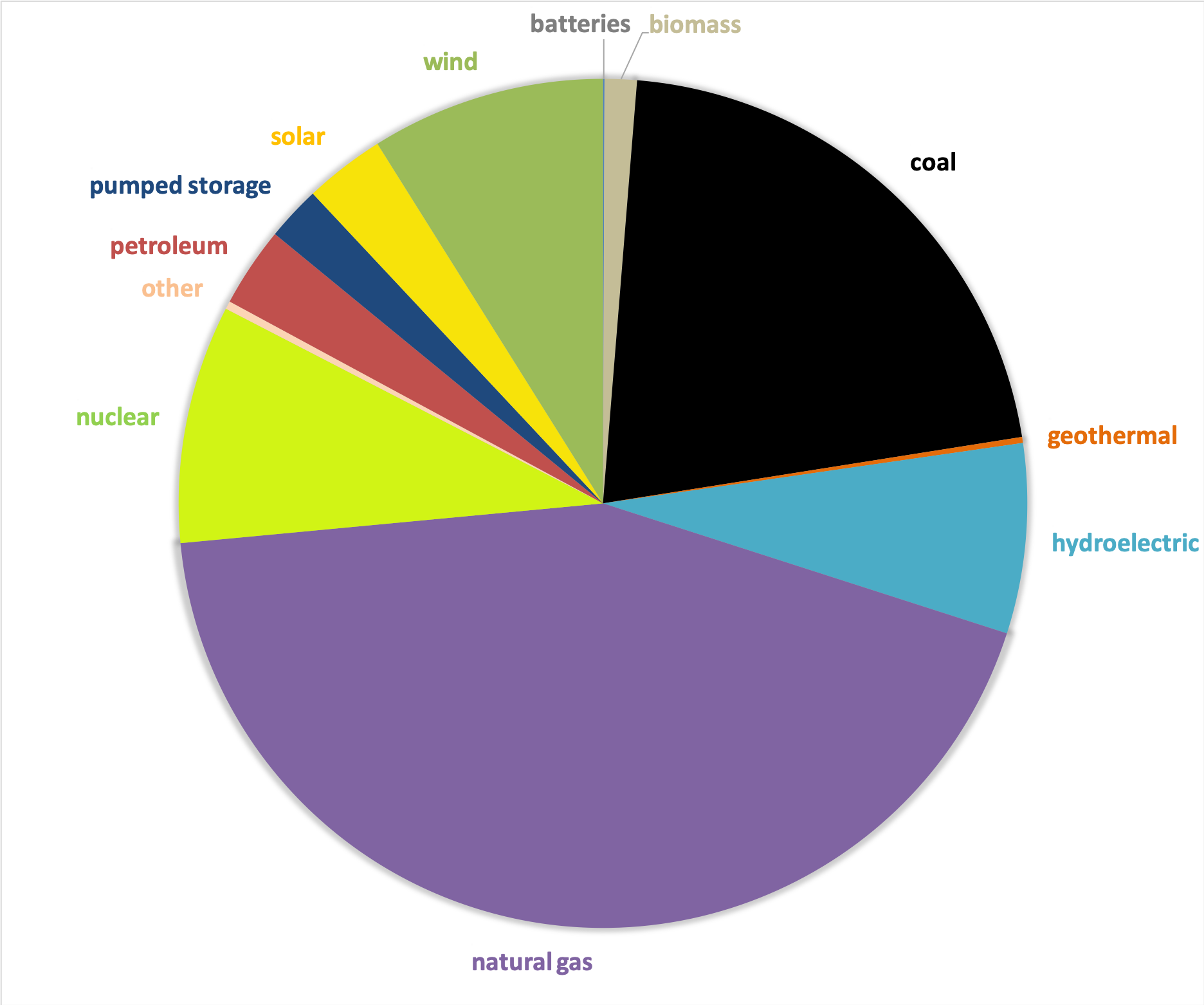

In terms of megawatts of electricity generated, the picture is much different – with natural gas supplying the highest percentage of electricity (44%), much more than the second place source, which is coal at 21%, and far more than solar, which generates only 3% (Figure 1).

Figure 1. Electricity generation by source in the United States, 2019. Data from EIA.

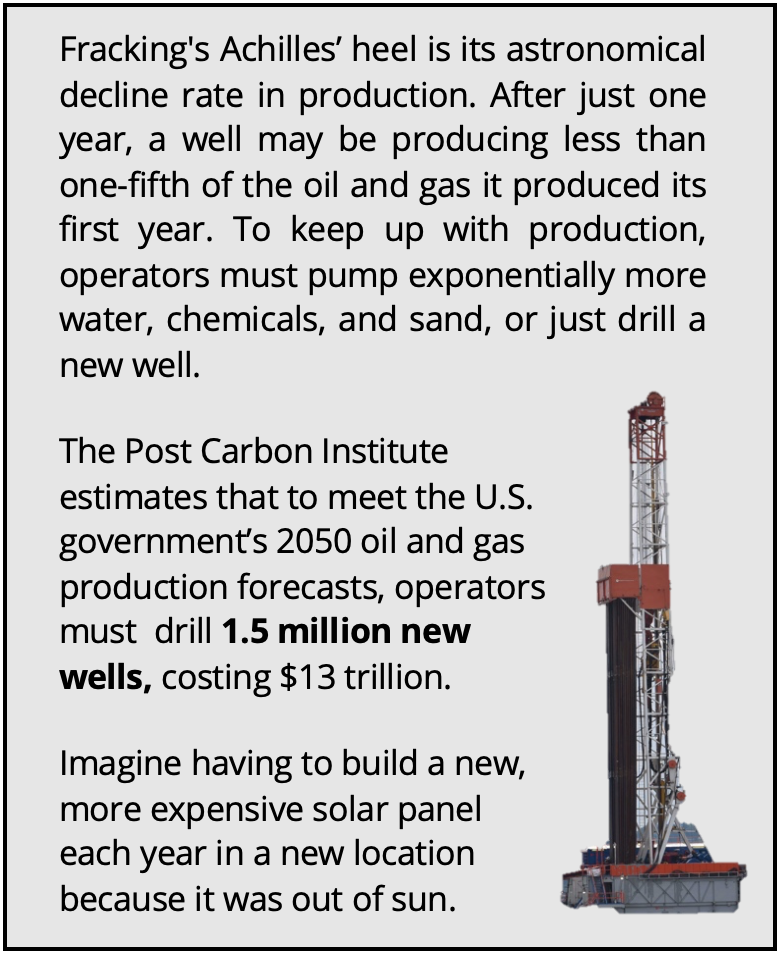

This difference speaks to the decentralized nature of the solar industry, with more facilities producing less energy. At a glance, this may seem less efficient and more costly than the natural gas alternative, which has fewer plants producing more energy. But in reality, each of these natural gas plants depend on thousands of fracked wells – and they’re anything but efficient.

The cost per megawatt hour of electricity for a renewable energy power plants is now cheaper than that of fracked gas power plants. A report by the Rocky Mountain Institute, found “even as clean energy costs continue to fall, utilities and other investors have announced plans for over $70 billion in new gas-fired power plant construction through 2025. RMI research finds that 90% of this proposed capacity is more costly than equivalent [clean energy portfolios, which consist of wind, solar, and energy storage technologies] and, if those plants are built anyway, they would be uneconomic to continue operating in 2035.”

The economics side with renewables – but with solar, wind, geothermal comprising only 12% of the energy pie, and hydropower at 7%, do renewables have the capacity to meet the nation’s energy needs? Yes! Even the Energy Information Administration, a notorious skeptic of renewable energy’s potential, forecasted renewables would beat out natural gas in terms of electricity generation by 2050 in their 2020 Annual Energy Outlook.

This prediction doesn’t take into account any future legislation limiting fossil fuel infrastructure. A ban on fracking or policies under a Green New Deal could push renewables into the lead much sooner than 2050.

In a void of national leadership on the transition to cleaner energy, a few states have bolstered their renewable portfolio.

Figure 2. Electricity generation state-wide by source, 2019. Data from EIA.

One final factor to consider – the pie pieces on these state charts aren’t weighted equally, with some states’ capacity to generate electricity far greater than others. The top five electricity producers are Texas, California, Florida, Pennsylvania, and Illinois.

Transportation

In 2018, approximately 28% of total U.S. energy consumption was for transportation. To understand the scale of infrastructure that serves this sector, it’s helpful to click on the petroleum refineries, crude oil rail terminals, and crude oil pipelines on the map.

Transportation Fuel Infrastructure. Data from EIA.

The majority of gasoline we use in our cars in the US is produced domestically. Crude oil from wells goes to refineries to be processed into products like diesel fuel and gasoline. Gasoline is taken by pipelines, tanker, rail, or barge to storage terminals (add the “petroleum product terminal” and “petroleum product pipelines” legend items), and then by truck to be further processed and delivered to gas stations.

China leads the world in this movement. In 2018, just over half of the world’s electric vehicles sales occurred in China. Analysts predict that the country’s oil demand will peak in the next five years thanks to battery-powered vehicles and high-speed rail.

In the United States, the percentage of electric vehicles on the road is small but growing quickly. Tax credits and incentives will be important for encouraging this transition. Almost half of the country’s electric vehicle sales are in California, where incentives are added to the federal tax credit. California also has a “Zero Emission Vehicle” program, requiring electric vehicles to comprise a certain percentage of sales.

We can’t ignore where electric vehicles are sourcing their power – and for that we must go back up to the electricity generation section. If you’re charging your car in a state powered mainly by fossil fuels (as many are), then the electricity is still tied to fossil fuels.

Petrochemicals

Many of the oil and gas infrastructure on the map doesn’t go towards energy at all, but rather aids in manufacturing petrochemicals – the basis of products like plastic, fertilizer, solvents, detergents, and resins.

Natural gas processing plants separate components of the natural gas stream to extract natural gas liquids like ethane and propane – which are transported through the natural gas liquid pipelines. These natural gas liquids are key building blocks of the petrochemical industry.

Ethane crackers process natural gas liquids into polyethylene – the most common type of plastic.

The chemical plants on this map include petrochemical production plants and ammonia manufacturing. Ammonia, which is used in fertilizer production, is one of the top synthetic chemicals produced in the world, and most of it comes from steam reforming natural gas.

As we discuss ways to decarbonize the country, petrochemicals must be a major focus of our efforts. That’s because petrochemicals are expected to account for over a third of global oil demand growth by 2030 and nearly half of demand growth by 2050 – thanks largely to an increase in plastic production. The International Energy Agency calls petrochemicals a “blind spot” in the global energy debate.

Petrochemical development off the coast of Texas, November 2019. Photo by Ted Auch, aerial support provided by LightHawk.

Investing in plastic manufacturing is the fossil fuel industry’s strategy to remain relevant in a renewable energy world. As such, we can’t break up with fossil fuels without also giving up our reliance on plastic. Legislation like the Break Free From Plastic Pollution Act get to the heart of this issue, by pausing construction of new ethane crackers, ensuring the power of local governments to enact plastic bans, and phasing out certain single-use products.

“The greatest industrial challenge the world has ever faced”

Mapped out, this web of fossil fuel infrastructure seems like a permanent grid locking us into a carbon-intensive future. But even more overwhelming than the ubiquity of fossil fuels in the US is how quickly this infrastructure has all been built. Everything on this map was constructed since Industrial Revolution, and the vast majority in the last century (Figure 3) – an inch on the mile-long timeline of human civilization.

Figure 3. Global Fossil Fuel Consumption. Data from Vaclav Smil (2017)

In fact, over half of the carbon from burning fossil fuels has been released in the last 30 years. As David Wallace Wells writes in The Uninhabitable Earth, “we have done as much damage to the fate of the planet and its ability to sustain human life and civilization since Al Gore published his first book on climate than in all the centuries—all the millennia—that came before.”

What will this map look like in the next 30 years?

A recent report on the global economics of the oil industry states, “To phase out petroleum products (and fossil fuels in general), the entire global industrial ecosystem will need to be reengineered, retooled and fundamentally rebuilt…This will be perhaps the greatest industrial challenge the world has ever faced historically.”

Is it possible to build a decentralized energy grid, generated by a diverse array of renewable, local, natural resources and backed up by battery power? Could all communities have the opportunity to control their energy through member-owned cooperatives instead of profit-thirsty corporations? Could microgrids improve the resiliency of our system in the face of increasingly intense natural disasters and ensure power in remote regions? Could hydrogen provide power for energy-intensive industries like steel and iron production? Could high speed rail, electric vehicles, a robust public transportation network and bike-able cities negate the need for gasoline and diesel? Could traditional methods of farming reduce our dependency on oil and gas-based fertilizers? Could zero waste cities stop our reliance on single-use plastic?

Of course! Technology evolves at lightning speed. Thirty years ago we didn’t know what fracking was and we didn’t have smart phones. The greater challenge lies in breaking the fossil fuel industry’s hold on our political system and convincing our leaders that human health and the environment shouldn’t be externalized costs of economic growth.

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2020/02/National-map-feature-3.png400900Erica Jacksonhttps://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.pngErica Jackson2020-02-28 17:35:142022-05-02 15:21:42National Energy and Petrochemical Map