Industry Targets Peaceful Protest via “Critical Infrastructure” Legislation

By Ted Auch, PhD, Great Lakes Program Coordinator and Shannon Smith, Manager of Communications & Development

The oil and gas industry continues to use rhetoric focusing on national security and energy independence in order to advocate for legislation to criminalize climate activists. Backlash against protestors and environmental stewards has only increased since the onset of COVID-19, suggesting that industry proponents are exploiting this public health crisis to further their own dangerous and controversial policies.[1]

Industry actors contributing to the wave of anti-protest bills include American Petroleum Institute (API), IHS Markit, The American Fuel & Petrochemical Manufacturers (AFPM), and most effectively, the American Legislative Exchange Council (ALEC), by way of its primary financial backer, Koch Industries (Fang, 2014, Shelor, 2017).

ALEC is the source of the model legislation “Critical Infrastructure Protection Act” of 2017, intended to make it a felony to “impede,” “inhibit,” “impair,” or “interrupt” critical infrastructure operation and/or construction. Close approximations – if not exact replicas – of this legislative template have been passed in 11 hydrocarbon rich and/or pathway states, and 8 more are being debated in 4 additional states.

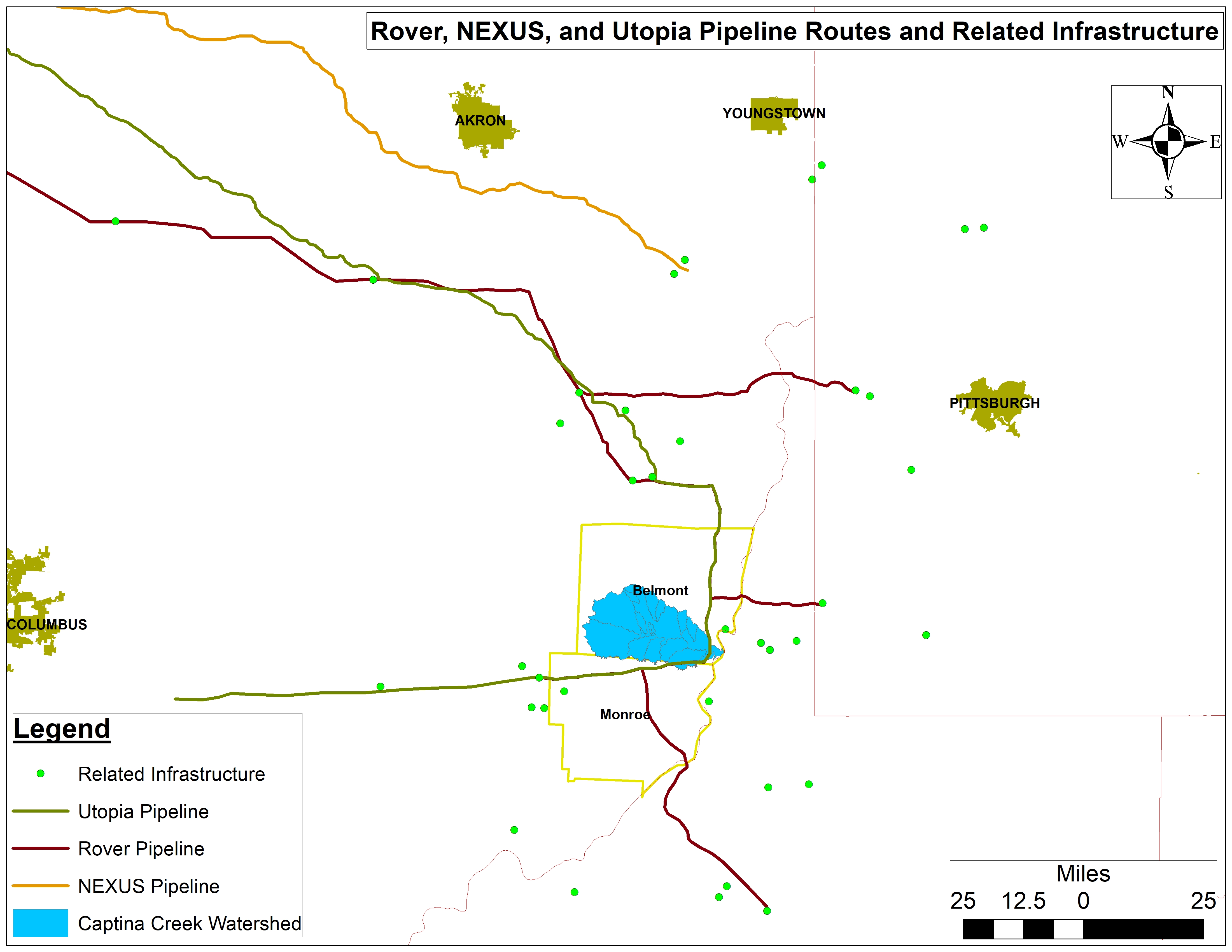

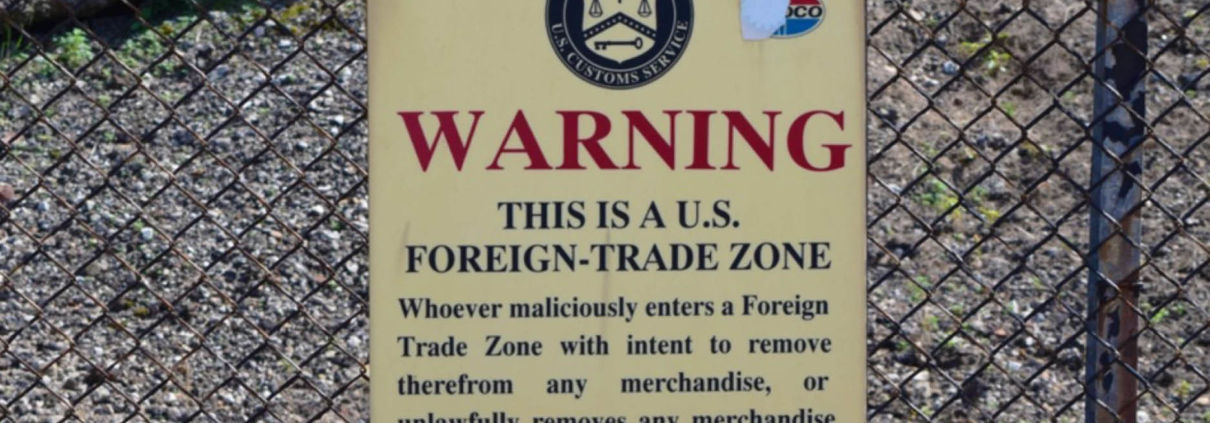

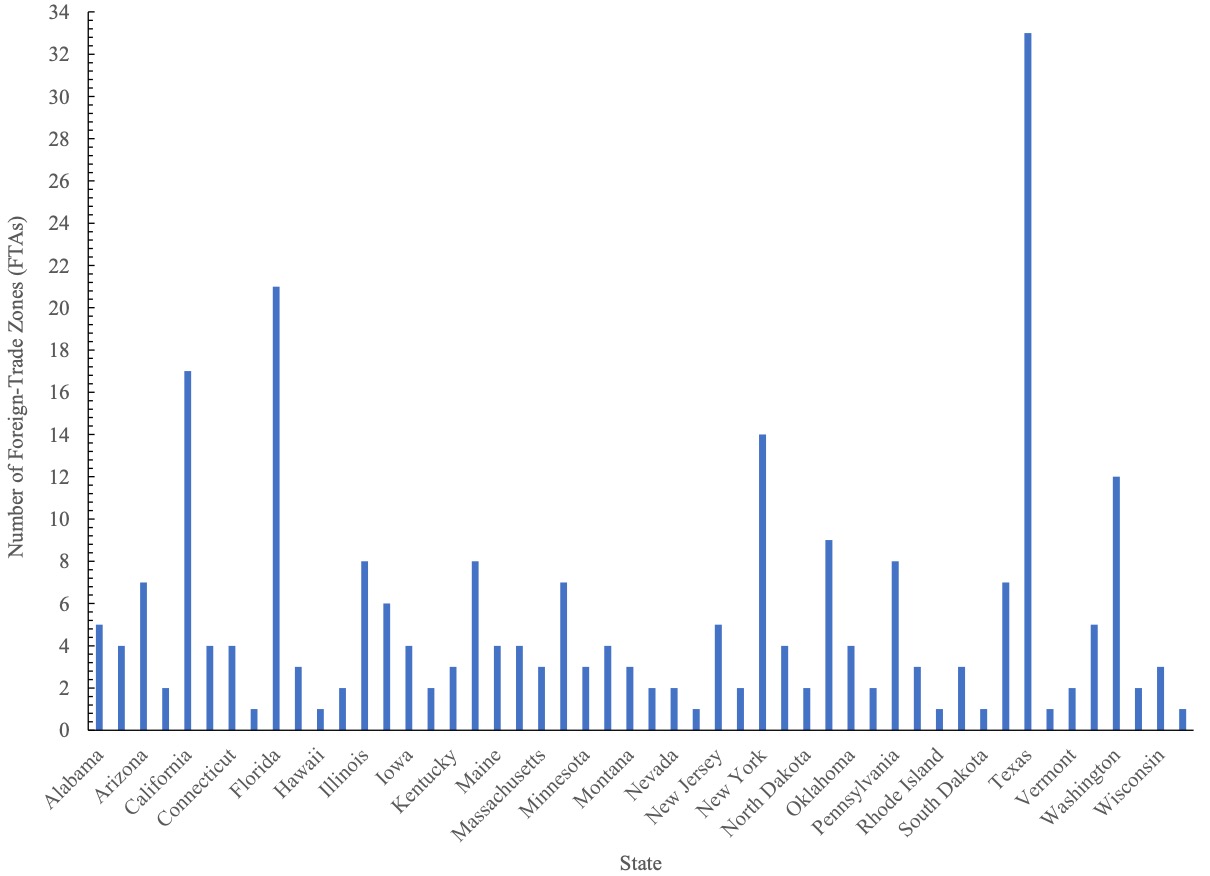

The “critical infrastructure” designation in ALEC’s “Critical Infrastructure Protection Act” is extremely broad, including over 70 pieces of infrastructure, from wastewater treatment and well pads, to ports and pipelines. However, along with the 259 Foreign Trade Zones (FTZ) (Figures 1 and 4) supervised by US Customs and Border Protection (CBP), security is of such importance because over 50% of this infrastructure is related to oil and gas. According to our analysis, there are more than 8,000 unique pieces of infrastructure that fall under this designation, with over 10% in the Marcellus/Utica states of Ohio, West Virginia, and Pennsylvania. See Figure 1 for the number of FTZ per state.

Regarding FTZ, the US Department of Homeland Security doesn’t attempt to hide their genuine nature, boldly proclaiming them “… the United States’ version of what are known internationally as free-trade zones … to serve adequately ‘the public interest’.” If there remains any confusion as to who these zones are geared toward, the US Department of Commerce’s International Administration (ITA) makes the link between FTZ and the fossil fuel industry explicit in its FTZ FAQ page, stating “The largest industry currently using zone procedures is the petroleum refining industry.” (Figure 2)

Figure 1. Number of Foreign-Trade Zones (FTZ) by state as of June 2020.

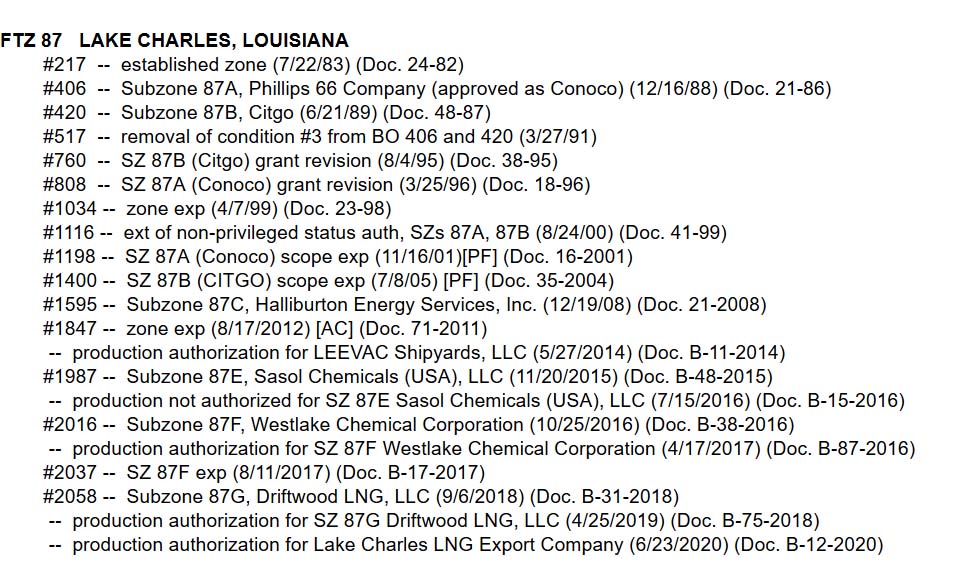

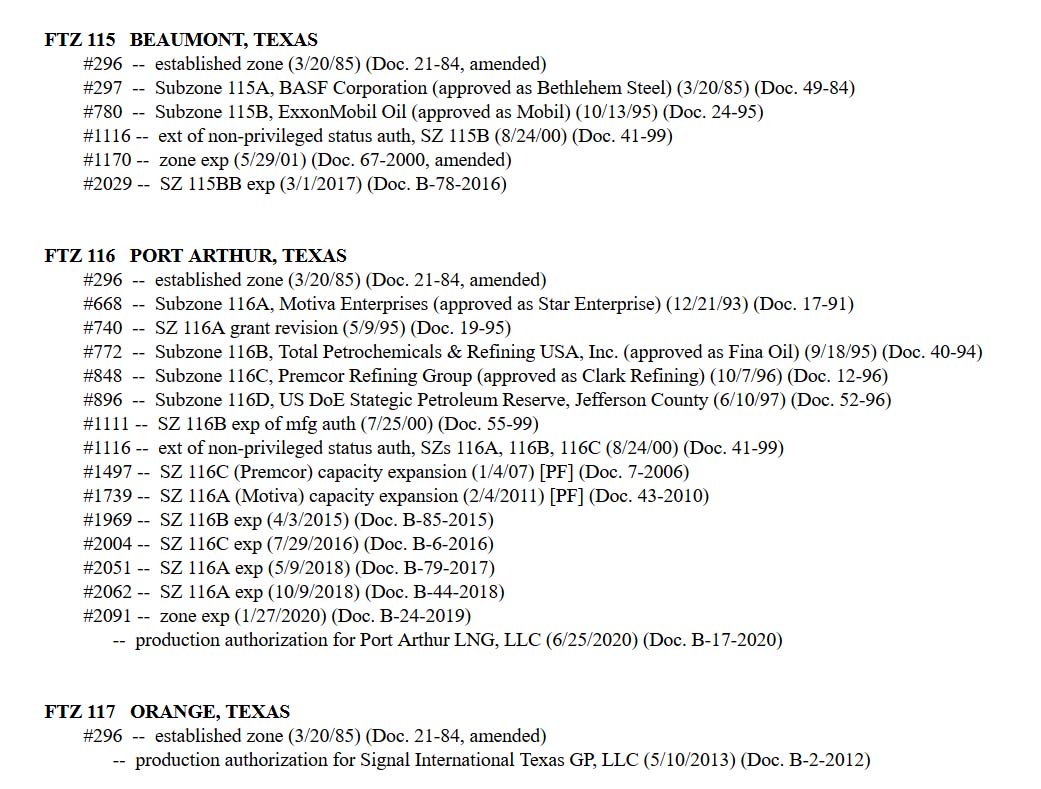

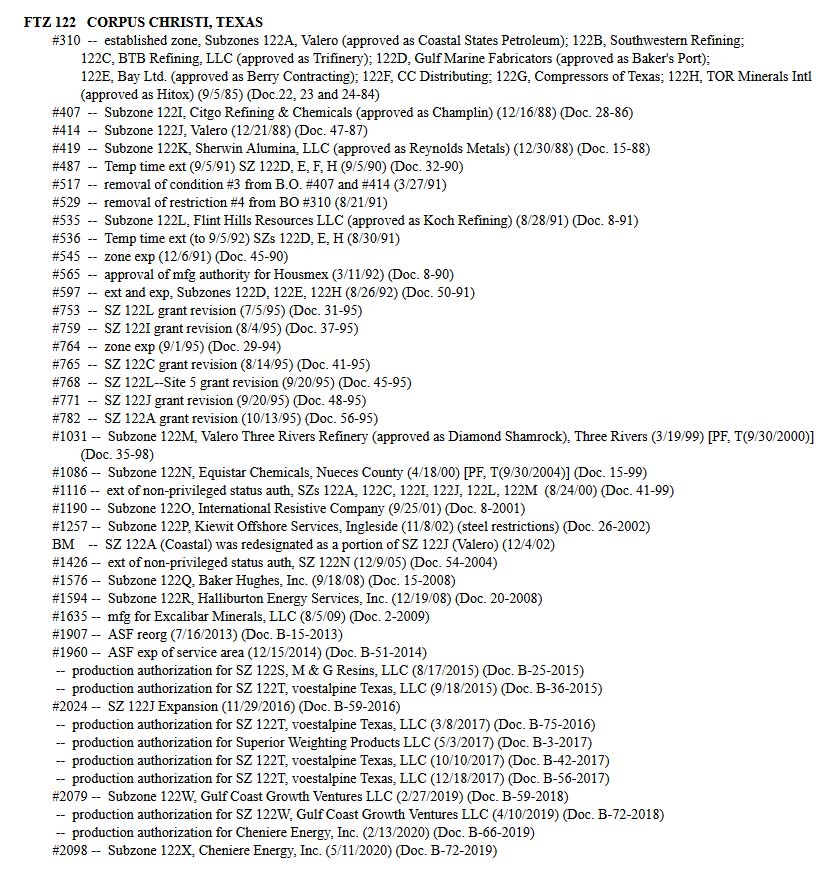

Figure 2. Foreign-Trade Zone (FTZ) Board of Actions in Zones 87 in Lake Charles, LA, 115-117 in and around Port Arthur, TX, and 122 in Corpus Christi, TX. (click on the images to enlarge)

Foreign-Trade Zone (FTZ) Board of Actions in Zone 87 in Lake Charles, Louisiana

Foreign-Trade Zone (FTZ) Board of Actions in Zones 115-117 in and around Port Arthur, Texas

Foreign-Trade Zone (FTZ) Board of Actions in Zone 122 in Corpus Christi, Texas

Much of the oil, gas, and petrochemical industries’ efforts stem from the mass resistance to the Dakota Access Pipeline (DAPL). Native American tribes and environmental groups spent months protesting the environmentally risky $3.78 billion dollar project, which began production in June 2017, after Donald Trump signed an executive order to expedite construction during his first week in office. The Standing Rock Sioux tribe also sued the US government in a campaign effort to protect their tribal lands. The world watched as Energy Transfer Partners (ETP), the company building the pipeline, destroyed Native artifacts and sacred sites, and as police deployed tear gas and sprayed protesters with water in temperatures below freezing.

ETP’s bottom line and reputation were damaged during the fight against DAPL. Besides increasingly militarized law enforcement, the oil and gas industry has retaliated by criminalizing similar types of protests against fossil fuel infrastructure. However, the tireless work of Native Americans and environmental advocates has resulted in a recent victory in March 2020, when a federal judge ordered a halt to the pipeline’s production and an extensive new environmental review of DAPL.

Just days ago, on July 6, 2020, a federal judge ruled that DAPL must shut down until further environmental review can assess potential hazards to the landscape and water quality of the Tribe’s water source. This is certainly a victory for the Standing Rock Sioux Tribe and other environmental defenders, but the decision is subject to appeal.

Since the DAPL conflict began, the industry has been hastily coordinating state-level legislation in anticipation of resistance to other notable national gas transmission pipelines, more locally concerning projects like Class II Oil and Gas Waste Injection Wells, and miles of gas gathering pipelines that transport increasing streams of waste – as well as oil and gas – to coastal processing sites.

The following “critical infrastructure” bills have already been enacted:

| STATE | BILL | TITLE | DATE PASSED | |

| West Virginia | HB 4615 | NEW PENALTIES FOR PROTESTS NEAR GAS AND OIL PIPELINES | 3/25/20 | |

| South Dakota | SB 151 | NEW PENALTIES FOR PROTESTS NEAR PIPELINES AND OTHER INFRASTRUCTURE | 3/18/20 | |

| Kentucky | HB 44 | NEW PENALTIES FOR PROTESTS NEAR PIPELINES AND OTHER INFRASTRUCTURE | 3/16/20 | |

| Wisconsin | AB 426 | NEW PENALTIES FOR PROTESTS NEAR GAS AND OIL PIPELINES | 11/21/19 | |

| Missouri | HB 355 | NEW PENALTIES FOR PROTESTS NEAR GAS AND OIL PIPELINES | 7/11/19 | |

| Texas | HB 3557 | NEW CRIMINAL AND CIVIL PENALTIES FOR PROTESTS AROUND CRITICAL INFRASTRUCTURE | 6/14/19 | |

| Tennessee | SB 264 | NEW PENALTIES FOR PROTESTS NEAR GAS AND OIL PIPELINES | 5/10/19 | |

| Indiana | SB 471 | NEW PENALTIES FOR PROTESTS NEAR CRITICAL INFRASTRUCTURE | 5/6/19 | |

| North Dakota | HB 2044 | HEIGHTENED PENALTIES FOR PROTESTS NEAR CRITICAL INFRASTRUCTURE | 4/10/19 | |

| Louisiana | HB 727 | HEIGHTENED PENALTIES FOR PROTESTING NEAR A PIPELINE | 5/30/18 | |

| Oklahoma | HB 1123 | NEW PENALTIES FOR PROTESTS NEAR CRITICAL INFRASTRUCTURE | 5/3/17 | |

There are an additional eight bills proposed and under consideration in these six states:

| STATE | PENDING | TITLE | DATE PROPOSED |

| Louisiana | HB 197 | NEW PENALTIES FOR PROTESTS NEAR CRITICAL INFRASTRUCTURE | 2/24/20 |

| Minnesota | HF 3668 | NEW PENALTIES FOR PROTESTS NEAR GAS AND OIL PIPELINES | 2/24/20 |

| Mississippi | HB 1243 | NEW PENALTIES FOR PROTESTS NEAR CRITICAL INFRASTRUCTURE | 2/19/20 |

| Alabama | SB 45 | NEW PENALTIES FOR PROTESTS NEAR GAS AND OIL PIPELINES | 2/4/20 |

| Minnesota | HF 2966 | NEW PENALTIES FOR PROTESTS NEAR OIL AND GAS PIPELINES | 1/31/20 |

| Minnesota | SF 2011 | NEW PENALTIES FOR PROTESTS NEAR GAS AND OIL PIPELINES | 3/4/19 |

| Ohio | SB 33 | NEW PENALTIES FOR PROTESTS NEAR CRITICAL INFRASTRUCTURE | 2/12/19 |

| Illinois | HB 1633 | NEW PENALTIES FOR PROTESTS NEAR CRITICAL INFRASTRUCTURE | 1/31/19 |

Desperate Backlash Against Peaceful Protest

Activists and organizations like the American Civil Liberties Union (ACLU) are framing their opposition to such legislation as an attempt to stave off the worst Orwellian instincts of our elected officials, whether they are in Columbus or Mar-a-Lago. On the other hand, industry and prosecutors are framing these protests as terroristic acts that threaten national security, which is why sentencing comes with a felony conviction and up to ten years in prison. The view of the FBI’s deputy assistant director and top official in charge of domestic terrorism John Lewis is that, “In recent years, the Animal Liberation Front and the Earth Liberation Front have become the most active, criminal extremist elements in the United States … the FBI’s investigation of animal rights extremists and ecoterrorism matters is our highest domestic terrorism investigative priority.”

It shocked many when last week, two protesters in the petrochemical-laden “Cancer Alley” region of Louisiana were arrested and charged under the state’s felony “terrorist” law. Their crime? Placing boxes of nurdles – plastic pellets that are the building blocks of many single-use plastic products – on the doorsteps of fossil fuel lobbyists’ homes. To make matters more ridiculous, the nurdles were illegally dumped by the petrochemical company Formosa Plastics.[2] This is outrageous indeed, but is the sort of legally-sanctioned oppression that fossil fuel industry lobbyists have been successfully advocating for years.

American Fuel & Petrochemical Manufacturers (AFPM) stated in a letter of support for ALEC’s legislative efforts:

“In recent years, there has been a growing and disturbing trend of individuals and organizations attempting to disrupt the operation of critical infrastructure in the energy, manufacturing, telecommunications, and transportation industries. Energy infrastructure is often targeted by environmental activists to raise awareness of climate change and other perceived environmental challenges. These activities, however, expose individuals, communities, and the environment to unacceptable levels of risk, and can cause millions of dollars in damage … As the private sector continues to expand and maintain the infrastructure necessary to safely and reliably deliver energy and other services to hundreds of millions of Americans, policymakers should continue to consider how they can help discourage acts of sabotage … Finally, it will also hold organizations both criminally and vicariously liable for conspiring with individuals who willfully trespass or damage critical infrastructure sites.”

Those organizations deemed ‘criminally and vicariously liable’ would in some states face fines an order of magnitude greater than the actual individual, which would cripple margin-thin environmental groups around the country, and could amount to $100,000 to $1,000,000. The AFPM’s senior vice president for federal and regulatory affairs Derrick Morgan referred to these vicarious organizations as “inspiring … organizations who have ill intent, want to encourage folks to damage property and endanger lives …”

Oklahoma Oil & Gas Association (OKOGA) wrote in a fear-mongering letter to Oklahoma Governor Mary Fallin that such legislation was necessary to “protect all Oklahomans from risk of losing efficient and affordable access to critical services needed to power our daily lives.”

One of the most disturbing aspects of this legislation is that it could, according to the testimony and additional concerns of ACLU of Ohio’s Chief Lobbyist Gary Daniels, equate “‘impeding’ and ‘inhibiting’ the ‘operations’ of a critical infrastructure site” with acts as innocuous as Letters to the Editor, labor strikes or protests, attending and submitting testimony at hearings, or simply voicing your concern or objections to the validity of industry claims and its proposals with emails, faxes, phone calls, or a peaceful protest outside critical infrastructure that raises the concern of site security. Mr. Daniels noted in his additional written testimony that the latter, “may prove inconvenient to the site’s staff, under SB 250 they would be an F3 [Third Degree Felony], and that is without someone even stepping foot on or near the property, as physical presence is not required to be guilty of criminal mischief, as found in/defined in Sec. 2907.07(A)(7) of the bill.”

Figure 3. A rally held by the Louisiana-based nonprofit RISE St. James.

This connection, when enshrined into law, will have a chilling effect on freedom of speech and assembly, and will stop protests or thoughtful lines of questioning before they even start. As the Ohio Valley Environmental Coalition (OVEC) put it in their request for residents to ask the governor to veto the now-enacted HB 4615, such a bill is unnecessary, duplicative, deceitful, un-American, unconstitutional, and “will further crowd our jails and prisons.”

To combat such industry-friendly legislation that erodes local government control in Ohio, lawmakers like State Senator Nikki Antonio are introducing resolutions like SR 221, which would, “abolish corporate personhood and money-as-speech doctrine” made law by the Supreme Court of the United States’ rulings in Citizens United v. FEC and Buckley v. Valeo. After all, the overarching impact of ALEC’s efforts and those described below furthers privatized, short-term profit and socialized, long-term costs, and amplifies the incredibly corrosive Citizen’s United decision a little over a decade ago.

Further Criminalization of Protest, Protections for Law Enforcement

Simultaneously, there is an effort to criminalize protest activities through “riot boosting acts,” increased civil liability and decreased police liability, trespassing penalties, and new sanctions for protestors who conceal their identities (by wearing a face mask, for example).

The following bills have already been enacted:

| STATE | BILL | TITLE | DATE PASSED |

| South Dakota | SB 189 | EXPANDED CIVIL LIABILITY FOR PROTESTERS AND PROTEST FUNDERS | 3/27/19 |

| West Virginia | HB 4618 | ELIMINATING POLICE LIABILITY FOR DEATHS WHILE DISPERSING RIOTS AND UNLAWFUL ASSEMBLIES | 3/10/18 |

| North Dakota | HB 1426 | HEIGHTENED PENALTIES FOR RIOT OFFENCES | 2/23/17 |

| North Dakota | HB 1293 | EXPANDED SCOPE OF CRIMINAL TRESPASS | 2/23/17 |

| North Dakota | HB 1304 | NEW PENALTIES FOR PROTESTERS WHO CONCEAL THEIR IDENTITY | 2/23/17 |

In addition, the following bills have been proposed and are under consideration:

| STATE | PENDING | TITLE | DATE PROPOSED |

| Rhode Island | H 7543 | NEW PENALTIES FOR PROTESTERS WHO CONCEAL THEIR IDENTITY | 2/12/20 |

| Oregon | HB 4126 | HARSH PENALTIES FOR PROTESTERS WHO CONCEAL THEIR IDENTITY | 1/28/20 |

| Tennessee | SB 1750 | NEW PENALTIES FOR PROTESTERS WHO CONCEAL THEIR IDENTITY | 1/21/20 |

| Ohio | HB 362 | NEW PENALTIES FOR PROTESTERS WHO CONCEAL THEIR IDENTITY | 10/8/19 |

| Pennsylvania | SB 887 | NEW PENALTIES FOR PROTESTS NEAR “CRITICAL INFRASTRUCTURE” | 10/7/19 |

| Massachusetts | HB 1588 | PROHIBITION ON MASKED DEMONSTRATIONS | 1/17/19 |

All the while, the Bundy clan of Utah pillage – and at times – hold our public lands hostage, and white male Michiganders enter the state capital in Lansing armed for Armageddon, because they feel that COVID-19 is a hoax. We imagine that it isn’t these types of folks that West Virginia State Representatives John Shott and Roger Hanshaw had in mind when they wrote and eventually successfully passed HB 4618, which eliminated police liability for deaths while dispersing riots and unlawful assemblies.

Contrarily, South Dakota’s SB 189, or “Riot Boosting Act,” was blocked by the likes of US District Judge Lawrence L. Piersol, who wrote:

“Imagine that if these riot boosting statutes were applied to the protests that took place in Birmingham, Alabama, what might be the result? … Dr. King and the Southern Christian Leadership Conference could have been liable under an identical riot boosting law.”

Dangerous Work

FracTracker collaborated with Crude Accountability on a report documenting increasing reprisals against environmental activists in the US and Eurasia. Read the Report.

A Wave of Anti-Protest Laws in the COVID-19 Era

Despite Judge Piersol’s ruling, South Dakota (SB 151) joined Kentucky (HB 44) and West Virginia (HB 4615) in passing some form of ALEC’s bill since the COVID-19 epidemic took hold of the US. This is classic disaster capitalism. As former Barack Obama Chief of Staff Rahm Emanuel once said, “You never want a serious crisis to go to waste, and what I mean by that is it’s an opportunity to do things you think you could not do before.”

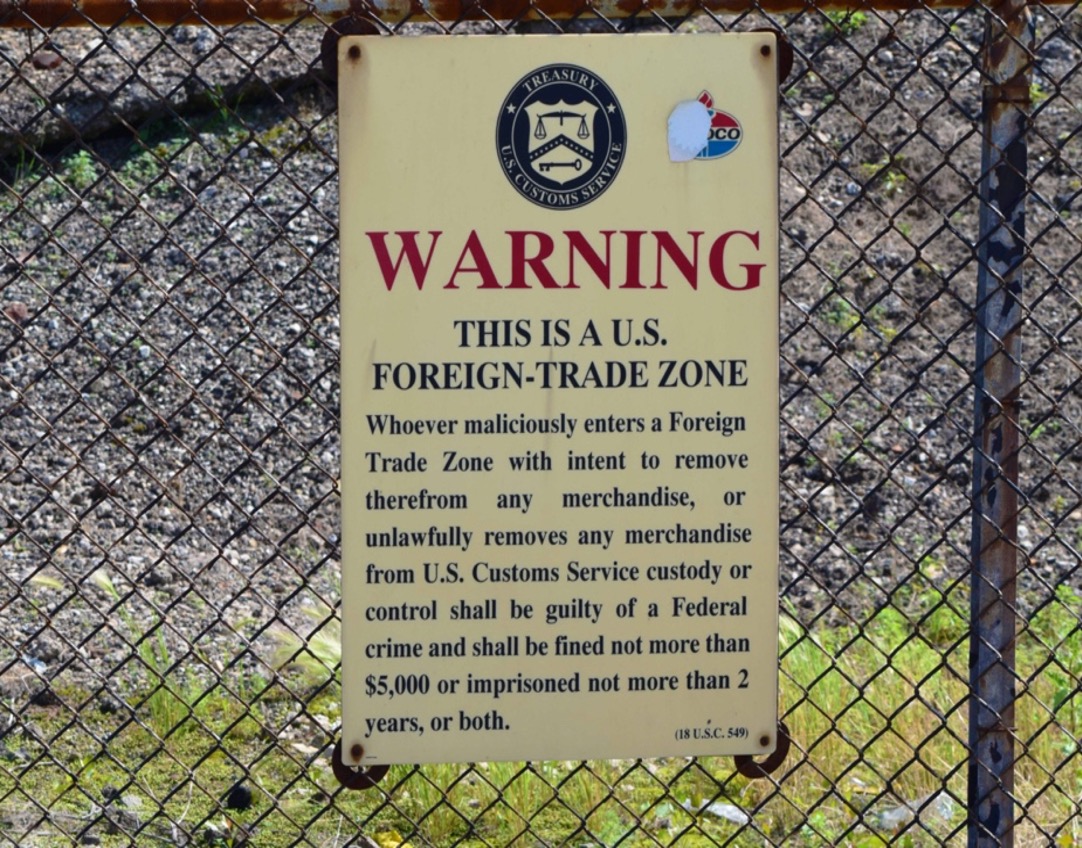

Figure 4. Photo of US Treasury Department signage outlining the warning associated with BP’s Whiting, IN, oil refinery designated a Foreign Trade Zone (FTZ). Photo by Ted Auch July 15th, 2015

In all fairness to Mr. Emanuel, he was referring to the Obama administration’s support for the post-2008 bipartisan Wall Street bailout. However, it is critical that we acknowledge the push for critical infrastructure legislation has been most assuredly bipartisan, with Democratic Governors in Kentucky, Louisiana, and Wisconsin signing into law their versions on March 16th of this year, in May of 2018, and in November of 2019, respectively.

According to the International Center for Not-for-Profit Law, 11 states have passed some version of ALEC’s bill, with the first uncoincidentally being a series of three bills signed in February of 2017 by North Dakota Governor Burgum, targeting “Heightened Penalties for Riot Offences” (HB 1426), “Expanded Scope of Criminal Trespass” (HB 1293), and “New Penalties for Protestors Who Conceal Their Identity” (HB 1304), with at least one member of ALEC’s stable of elected officials, Rep. Kim Koppelman, proudly displaying his affiliation in his biography on the North Dakota Legislative Branch’s website. Mr. Koppelman, along with Rep. Todd Porter out of Mandan, also cosponsored two of these bills.

Related Legislation in Need of Immediate Attention

In Columbus, Ohio, there are several pieces of legislation being pushed in concert with ALEC-led efforts. These include the recently submitted HB 362, that would “create the crime of masked intimidation.” Phil Plummer and George F. Lang sponsor the bill, with the latter being the same official who introduced HB 625, a decidedly anti-local control bill that would preempt communities from banning plastic bags. Most of the general public and some of the country’s largest supermarket chains have identified plastic bag bans as a logical next step as they wrestle with their role in the now universally understood crimes plastics have foisted on our oceans and shores. As Cleveland Scene’s Sam Allard wrote, “bill mills” and their willing collaborators in states like Ohio cause such geographies to march “boldly, with sigils flying in the opposite direction” of progress, and a more renewable and diversified energy future.

With respect to Plummer and Lang’s HB 362, two things must be pointed out:

1) It is eerily similar to North Dakota’s HB 1304 that created new penalties for protestors who conceal their identity, and

2) The North Dakota bill was conveniently signed into law by Governor Burgum on February 23rd, 2017, who had set the day prior as the “deadline for the remaining [DAPL] protesters to leave an encampment on federal land near the area of the pipeline company’s construction site.”

So, when elected officials as far away as Columbus copy and paste legislation passed in the aftermath of the DAPL resistance efforts, it is clear the message they are conveying, and the audience(s) they are trying to intimidate.

Plummer and Lang’s HB 362 would add a section to the state’s “Offenses Against the Public Peace,” Chapter 2917, that would in part read:

No person shall wear a mask or disguise in order to purposely do any of the following:

(A) Obstruct the execution of the law;

(B) Intimidate, hinder, or interrupt a person in the performance of the person’s legal duty; or

(C) Prevent a person from exercising the rights granted to them by the Constitution or the laws of this state.

Whoever violates this proposed section is guilty of masked intimidation. Masked intimidation is a first degree misdemeanor. It was critical for the DAPL protestors to protect their faces during tear gas and pepper spray barrages, from county sheriffs and private security contractors alike.

At the present moment, masks are one of the few things standing between COVID-19 and even more death. Given these realities, it is stunning that our elected officials have the time and/or interest in pushing bills such as HB 362 under the thin veil of law and order.

But judging by what one West Virginia resident and former oil and gas industry draftsman,[3] wrote to us recently, elected officials do not really have much to lose, given how little most people think of them:

“Honestly, it doesn’t seem to matter what we do. The only success most of us have had is in possibly slowing the process down and adding to the cost that the companies incur. But then again, the increase in costs probably just gets passed down to the consumers. One of the biggest drawbacks in my County is that most, if not all, of the elected officials are pro drilling. Many of them have profited from it.”

The oil, gas, and petrochemical industries are revealing their weakness by scrambling to pass repressive legislation to counteract activists. But social movements around the world are determined to address interrelated social and environmental issues before climate chaos renders our planet unlivable, particularly for those at the bottom of the socioeconomic ladder. We hope that by shining a light on these bills, more people will become outraged enough to join the fight against antidemocratic legislation.

This is Part I of a two-part series on concerning legislation related to the oil, gas, and petrochemical industries. Part II focuses on bills that would weaken environmental regulations in Ohio, Michigan, and South Dakota.

By Ted Auch, PhD, Great Lakes Program Coordinator and Shannon Smith, Manager of Communications & Development

[1] See Naomi Klein’s concept of the Shock Doctrine for similar trends.

[2] The community-based environmental organization RISE St. James has been working tirelessly to prevent Formosa Plastics from building one of the largest petrochemical complexes in the US in their Parish. Sharon Lavigne is a leading member of RISE St. James, and is an honored recipient of the 2019 Community Sentinel Award for Environmental Stewardship. Read more on Sharon’s work with RISE St. James here.

[3] This individual lives in Central West Virginia, and formerly monitored Oil & Gas company assets in primarily WV, PA, NY, VA, MD & OH, as well as the Gulf Coast. Towards the end of this individual’s career, they provided mapping support for the smart pigging program, call before you dig, and the pipeline integrity program.

Photo by Ted Auch, FracTracker Alliance

Photo by Ted Auch, FracTracker Alliance