A total of 498 operators were identified that manage at least one unplugged well; 261 of them (52%) did not report oil production volumes in 2022.

Key Findings

Less than 3% of operators (14) produced an average of 10 or more barrels per day (BOE/D), per well. Those 14 operators manage just 43 oil wells in total.

Statewide daily average per-well production volumes were 3.3 BOE/D, which is enough to fill the fuel tank of only 10 Toyota Camrys.

None of the state’s top 20 producers are producing more than 10 BOE/D per well, while the majority produce 3 BOE/D or less.

Chevron U.S.A. Inc. currently operates 26,243 unplugged wells, the most of any California operator, while 8,886 are currently idle.

In 2022, Chevron only produced an average of about 3.1 BOE/D per well for their entire portfolio of unplugged wells.

According to the calculated average daily per-well production index, Aera Energy LLC, California’s largest oil producer which was just divested by ExxonMobil and Shell, ranked 68th, indicating low average per well production volumes compared to their currently unplugged well portfolio.

Chevron ranked 78th indicating very low average daily per-well production volumes, particularly when compared to their currently unplugged well portfolio.

California Resources Corporation LLC ranked 88th, while its subsidiaries ranked 15th (Thums Long Beach), 28th (Tidelands), and 77th (CRC Elk Hills).

Overview

This report focuses on the productivity of California’s remaining oil reserves ranks California operators based on average daily per-well production volumes, an industry index that measures the health of oil and gas extraction operations. The results show that while there are a handful of oil and gas operators that continue to produce profitable volumes of oil, the majority of California operators, including the state’s oil and gas major corporations, Chevron, Aera Energy, and California Resources Corporation, are producing very low average volumes of oil per well.

While Chevron and other multinational oil and gas majors operating in California are reporting record profits, they have ignored the obligations to plug and remediate their backlog of idle wells in the state. Shell and Exxon, previous owners of the largest California operator Aera Energy divested entirely from California without plugging over 9,000 idle wells (nearly 40% of their total portfolio of unplugged wells). In total there are over 101,000 unplugged wells in the state. About 62,000 of those wells are active, and another 40,000 are idle, no longer operational.

This report shows that, while California operators maintain high counts of unplugged wells, average daily per-well production volumes are well below marginal levels. Previous research has shown that these marginal levels are not likely enough to even cover well plugging and reclamation costs. Additionally, consistent declines in per-well production volumes were documented for the majority of California operators over multiple years. When these operators divest from California or choose bankruptcy rather than covering these debts, California taxpayers will be left responsible for the plugging and clean up costs. California’s current system of idle well management has not been effective, and is in desperate need of immediate revision.

Industry Index Indicates Need to Plug Wells Now

Production from California oil reserves has been on the decline for the last four decades, and current production figures show that the operators in the state are likely nearing the end of their ability to profitably extract oil. While operators such as Chevron U.S.A. Inc are blaming California regulatory policies for major profit write downs, the data shows that it is more likely that these operators depleted their California reserves to the point that remaining rates of production will no longer be profitable. If California operators are not required to increase their rates of well plugging, California taxpayers are at a greater risk of covering the growing costs when the current operators divest or turn to bankruptcy. While California does have a joint and several liability law for oil and gas operations, allowing the state to sue previous operators for clean-up costs, creating a responsible regulatory framework to prevent operators from orphaning wells will reduce the need for California to pursue reimbursements via drawn-out litigative actions. Furthermore attempts to collect costs from bankrupt LLC’s have come up substantially short; the California oil and gas operator Chevron U.S.A. Inc. is itself a subsidiary of parent company Chevron Corp..

As the ultimate debt holder for the contingent liabilities of California’s oil and gas well portfolio, the state of California must protect the economic interests of Californians and take responsibility for requiring California operators to plug all non-producing wells. Table 1 below shows counts of unplugged wells and breaks down the total count by operational statuses for the 20 California operators with the highest counts. In total there are over 135,000 plugged and about 101,000 unplugged (61,000 operational and 40,000 idle) wells in California. While the immediate concerns for financial solvency are focused on plugging the backlog of idle wells in the state, it is important to acknowledge that each plugged well will require maintenance and monitoring in perpetuity, plus replugging operations in the future, at a managerial cost that will continue to grow at a compounded inflation rate.

Note the high counts of idle wells managed by each operator. Aera has the highest count, with over 9,000, and Chevron has the second highest count, with just under 9,000. One third of their unplugged wells are idle and should be plugged immediately. Over half of California Resources Corp.’s operational wells are idle. This is a result of irresponsible management by state regulators and a favorable regulatory landscape that has failed to prioritize debt management and environmental reclamation. Other oil and gas states such as North Dakota require operators to plug wells within one year of ending production, in order to prevent the buildup of such economic risk and environmental degradation. Without such protections and forward looking regulatory policies, California taxpayers will actually be left to pay for the billions of dollars of cleanup.

Average Daily Per-Well Production Index

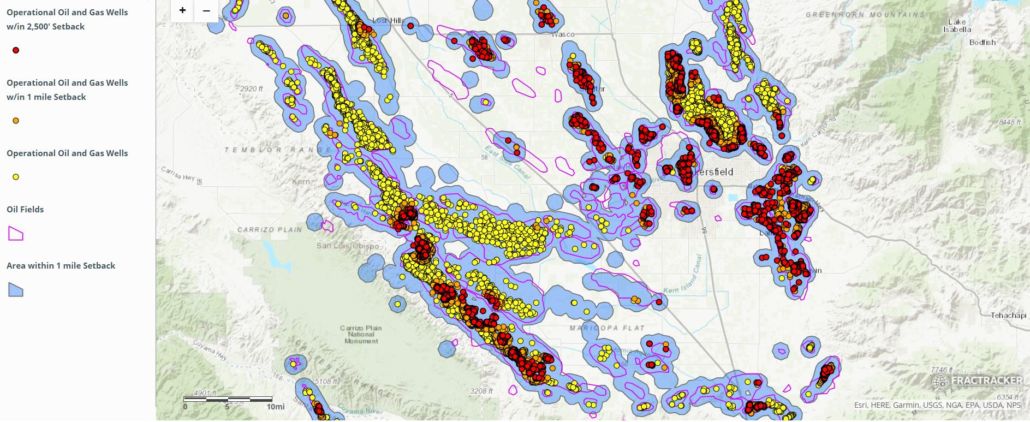

This new analysis by FracTracker Alliance uses California oil and gas production data published by the California Department of Geological Energy Management (CalGEM) to rank California operators based on the productive health of their operations. The tables below compare California oil and gas operators based on the calculated index, average daily per-well production (BOE/D). This index is used within the regulatory and investment sectors of the oil and gas industry to assess the health and profitability of extraction operations. The index was calculated for each California operator by dividing the total barrels per day (BOE/D) produced by the operator (calculated from annual production records), by the year-end count of unplugged wells owned by each operator.

(Average BOE/D Per−Well Production) = ([Total Annual Production (BOE)/365 days] / [Count of unplugged wells])

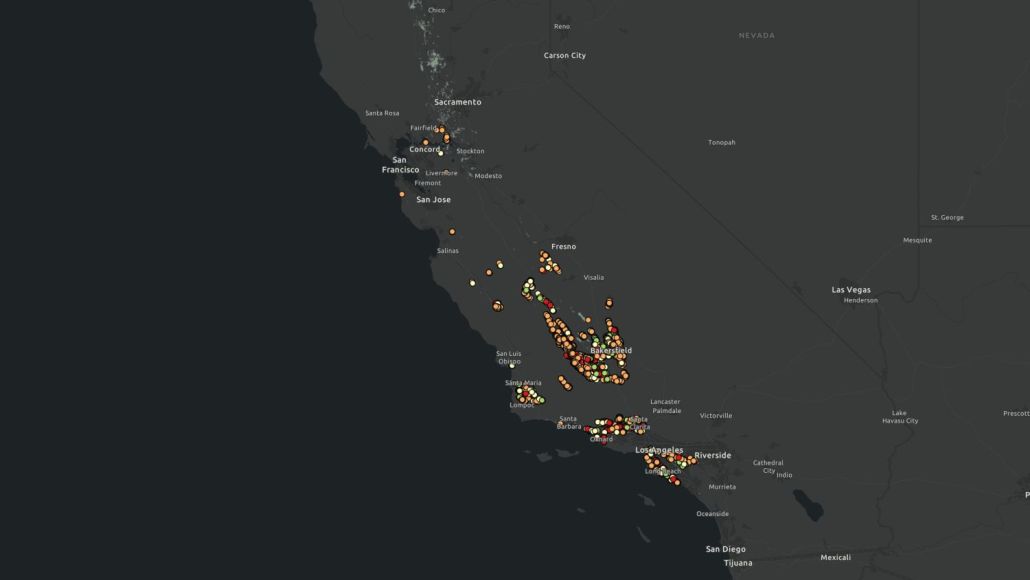

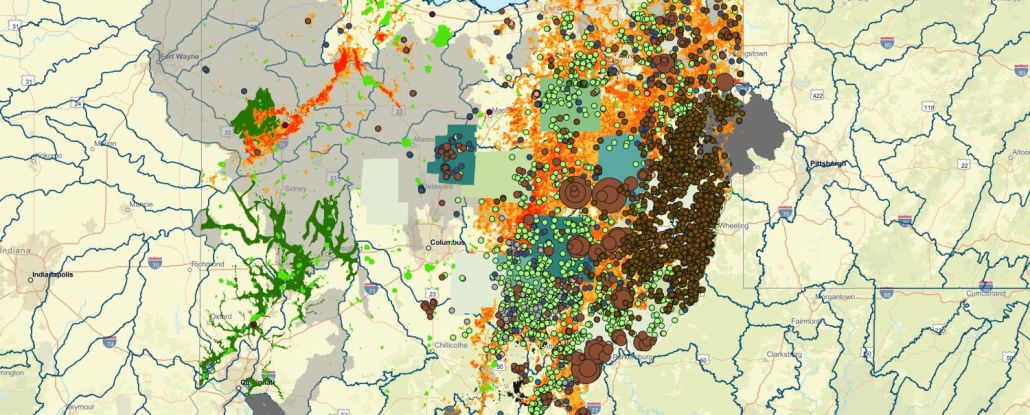

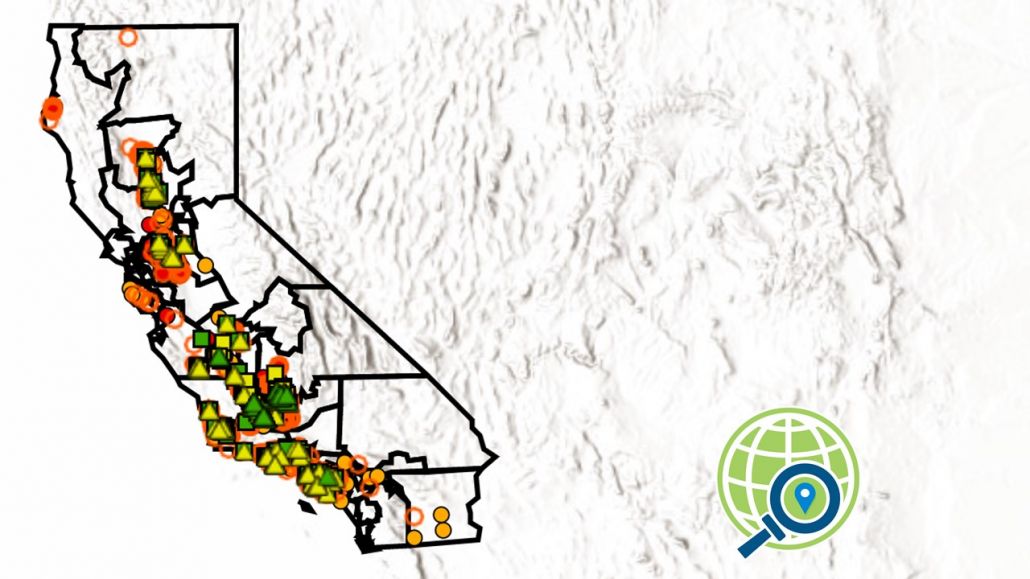

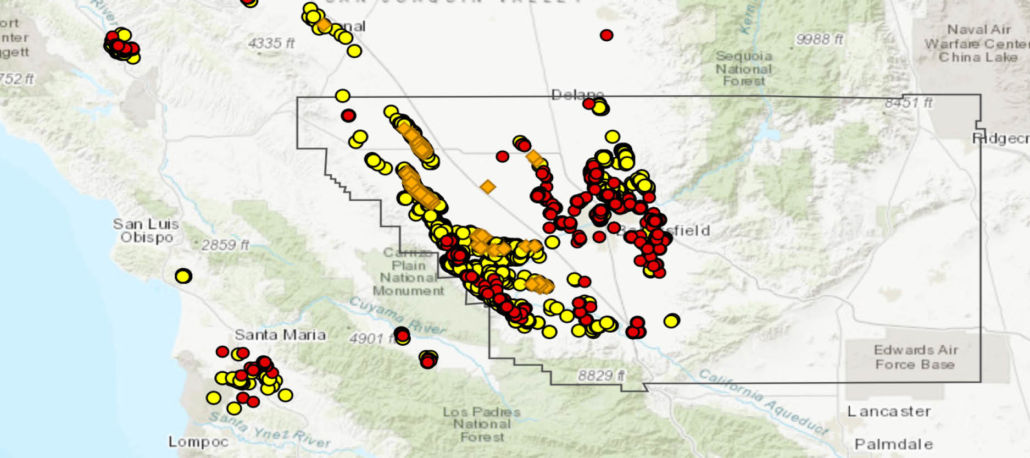

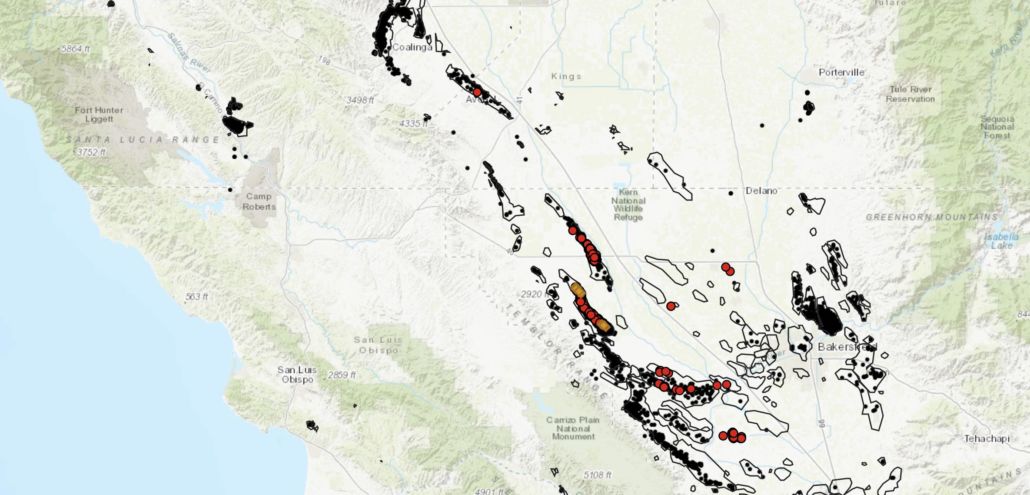

This analysis was conducted for the years 2019-2022 using California Department of Geological Energy Management (CalGEM) public data. Data for 2023 was not yet available in a complete and vetted dataset. The analysis was conducted using the programming language Python (V3.9.12). The Python code and datasets can be found in the Appendix (FracTracker data repository), which includes the full dataset that the following tables are derived from. The tables below summarize the results for the year 2022. The map below also shows summed production data for all unplugged wells for the year 2022. A darker color represents higher annual production volumes from that unplugged well. The ranks of the 20 largest California operators are shown below in Table 2.

California Daily Oil Production 2022

This interactive map looks at 2022 oil production volumes from California’s operational (Active, Idle, and New) oil and gas wells.

View the map “Details” tab below in the top right corner to learn more and access the data, or click on the map to explore the dynamic version of this data. Data sources are also listed at the end of this article. In order to turn layers on and off in the map, use the Layers dropdown menu. This tool is only available in Full Screen view. Items will activate in this map dependent on the level of zoom in or out.

View Full Size Map | Updated 1/29/2024 | Map Tutorial

California’s Oil Majors

While Chevron was the second largest oil producer in the state, Chevron also operated the most unplugged wells of any California operator in 2022, with 26,502 unplugged wells. The most up to date data (1/20/24) puts their unplugged well count at 26,244. While the operator has claimed to have plugged over 2,200 wells over the course of the last year,state records do not support this claim. CalGEM does not keep track of well plugging counts, and the existing CalGEM data shows this to not be likely.

Chevron only produced a daily per-well average of about 3 BOE/D for their entire portfolio of unplugged wells in California, ranking them 78th among the 261 California operators that reported production in 2022 (77th percentile). Compared to other California oil and gas majors, Chevron’s 2022 daily per-well production averages were about 15% below that of Aera Energy (Rank 68th; 82nd percentile), when Shell and Exxon sold Aera to divest from California oil and gas operations. Half of domestic oil and gas production between 2012 and 2022 came from wells that produced between 100 and 3,200 barrels per day, according to the Energy Information Administration. An onshore well that produces between 1,000 and 3,000 barrels of oil a day is considered a good production range. Almost all of of California’s oil wells produce marginal levels, much lower than even the cut-off for stripper wells, of 15 BOE/D.

Additional data on Chevron’s recent investments and divestments show that Chevron’s California operations are performing at comparatively poor levels as compared to their operations in other states. Prime examples are the case of Chevron acquiring Denver-Julesburg based operator Noble Energy in 2020 for $13 billion, which has a per-well oil production average volume of 36 BOE/D, and alternatively the case of Chevron’s recent divestment of oil wells in the Piceance Basin to Scout Energy, which at the time were producing a per-well oil production average volume of 14 BOE/D.

The analysis was completed for not just 2022, but the entire four year period 2019-2022, the results of which can be found in the Appendix (FracTracker Data Repository). The data shows consistent production declines in per-well production volumes for the majority of California oil majors over the course of this four year period, which continues the trend of decline since peak oil, four decades ago. The data shows that in 2022, average statewide daily per-well production equaled 3.3 BOE/D, while 88% of California operators with unplugged wells produced less than an average 4 BOE/D per well. Of note 2 BOE/D is considered a hard line in the industry for an oil well to just cover operational costs. Oil prices would have to remain over $130 per barrel for a well producing 4 BOE/D to cover just its own plugging and reclamation costs, whereas the average price for oil since 2019 has been about half that amount ($68 per barrel).

Conclusions

According to California state regulators there are over 101,000 unplugged wells in the state. About 62,000 of those wells are operational, and another 40,000 are idle (over 5,000 likely orphaned), no longer operational. While idle wells should be plugged immediately to reduce current environmental health risks, California oil companies and regulators have ignored this obligation. The current system in California is failing to manage California’s backlog of idle wells. Regulators and policy-makers must create a system for managing the retirement of producing wells that requires strict plugging deadlines, such as regulations that have been instituted in North Dakota, West Virginia and other states.

Furthermore, there is a great deal of evidence to show that the remaining operational oil and gas wells in the state will not produce enough oil to cover the costs of plugging, reclamation, and remediation. This new data analysis, combined with the previous analyses by FracTracker showing increasing divestment by larger California oil and gas operators and Carbon Tracker’s “There Will be Blood” report, show that California oil and gas extraction is at the tail end or already beyond the limits of profitability for the majority of operators. Adding additional pressure to the balance sheet of Chevron and other majors is the fact that depleted offshore reserves in additional geographies are also requiring these multinational companies to spend capital on remediation, while onshore remediation obligations grow. While development of unconventional oil and gas reserves has lengthened the lifespan of hydrocarbon companies, additional impending plugging, reclamation, and remediation debts will be increasingly coming to term, leading to additional future financial losses. California must be prepared.

References & Where to Learn More

Topics in This Article:

Join the Conversation

Stay Informed

Support Our Work

FracTracker Alliance helps communicate the risks of oil and gas and petrochemical development to advance just energy alternatives that protect public health, natural resources, and the climate.

By contributing to FracTracker, you are helping to make tangible changes, such as decreasing the number of oil and gas wells in the US, protecting the public from toxic and radioactive chemicals, and stopping petrochemical expansion into vulnerable communities.

Your donations help fund the sourcing and analysis of new data so that we can keep you informed and continually update our resources.

Please donate to FracTracker today as a way to advocate for clean water, clean air, and healthy communities.

What You Should Read Next

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/03/Web-Elements-Map-thumbnails-28.png

500

750

Shannon Smith

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Shannon Smith2026-06-12 15:27:012026-06-12 15:41:18PA DEP Approves Unusual “Mineral Brine” Well in Erie County, Raising Concerns About New Regulatory Loophole

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/03/Web-Elements-Map-thumbnails-28.png

500

750

Shannon Smith

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Shannon Smith2026-06-12 15:27:012026-06-12 15:41:18PA DEP Approves Unusual “Mineral Brine” Well in Erie County, Raising Concerns About New Regulatory Loophole https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/05/Untitled-design.jpg

844

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2026-04-30 17:32:352026-05-28 13:40:18From Coal Plant to AI Campus: FracTracker Documents Construction at Homer City

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/05/Untitled-design.jpg

844

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2026-04-30 17:32:352026-05-28 13:40:18From Coal Plant to AI Campus: FracTracker Documents Construction at Homer City https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/05/3.jpg

628

1200

Gwen Klenke

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Gwen Klenke2026-04-29 16:16:562026-05-08 11:24:12An update on Southwest Detroit Industrial Impacts: The Zug Island Ruling

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/05/3.jpg

628

1200

Gwen Klenke

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Gwen Klenke2026-04-29 16:16:562026-05-08 11:24:12An update on Southwest Detroit Industrial Impacts: The Zug Island Ruling https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/03/Shell-Polymers-Data-Tool-Graphics.png

628

1200

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2026-03-26 15:42:172026-04-03 10:35:54FracTracker’s New Data Tool Visualizes Shell’s Pollution, Violations, and Malfunctions Ahead of Permit Public Hearing

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/03/Shell-Polymers-Data-Tool-Graphics.png

628

1200

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2026-03-26 15:42:172026-04-03 10:35:54FracTracker’s New Data Tool Visualizes Shell’s Pollution, Violations, and Malfunctions Ahead of Permit Public Hearing https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/01/Howell-Township-Win-Article-Graphics.jpg

628

1200

Gwen Klenke

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Gwen Klenke2026-01-14 18:33:052026-05-06 18:11:32Howell Township Data Center Win: $1B Project Withdrawn After Community Meeting on Energy and Infrastructure Impacts

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/01/Howell-Township-Win-Article-Graphics.jpg

628

1200

Gwen Klenke

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Gwen Klenke2026-01-14 18:33:052026-05-06 18:11:32Howell Township Data Center Win: $1B Project Withdrawn After Community Meeting on Energy and Infrastructure Impacts https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/06/SShamer_Infrastructure-pipeline-rightofway-ColumbiaLineMB-BaltimoreCounty-MD-May2016.jpg

266

400

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-09-03 16:14:462025-09-30 10:26:57Comment Opposing the Southeast Supply Enhancement Project (SSEP) – Clean Water Act Section 404 Permit Application (SAW-2024-01961)

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/06/SShamer_Infrastructure-pipeline-rightofway-ColumbiaLineMB-BaltimoreCounty-MD-May2016.jpg

266

400

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-09-03 16:14:462025-09-30 10:26:57Comment Opposing the Southeast Supply Enhancement Project (SSEP) – Clean Water Act Section 404 Permit Application (SAW-2024-01961) https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/07/California-oil-fields-feature.jpg

667

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2025-08-26 17:36:222025-08-27 21:56:28California’s New Oil Wells Average 13.5 Barrels/Day — Far Below State Projections

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/07/California-oil-fields-feature.jpg

667

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2025-08-26 17:36:222025-08-27 21:56:28California’s New Oil Wells Average 13.5 Barrels/Day — Far Below State Projections Photo by David Becker

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/08/david-becker-crs2vlkSe98-unsplash.jpg

996

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-08-22 11:22:272025-08-26 15:47:09FracTracker Launches Oil, Gas, and Petrochemical Data Portals

Photo by David Becker

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/08/david-becker-crs2vlkSe98-unsplash.jpg

996

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-08-22 11:22:272025-08-26 15:47:09FracTracker Launches Oil, Gas, and Petrochemical Data Portals https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2013/12/Colorado.jpg

642

1144

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-07-22 10:42:552025-07-23 11:06:23Colorado Operators Increase Chemical Disclosures After Public Pressure, but Major Gaps Remain

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2013/12/Colorado.jpg

642

1144

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-07-22 10:42:552025-07-23 11:06:23Colorado Operators Increase Chemical Disclosures After Public Pressure, but Major Gaps Remain https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/07/Missouri-Oil-and-Gas-Wells-2025.jpg

921

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2025-07-21 19:15:592025-07-22 10:08:23Evaluation of Federal Requirements for Plugging Orphaned Oil and Gas Wells: A Missouri Case Study

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/07/Missouri-Oil-and-Gas-Wells-2025.jpg

921

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2025-07-21 19:15:592025-07-22 10:08:23Evaluation of Federal Requirements for Plugging Orphaned Oil and Gas Wells: A Missouri Case Study https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2019/03/IdleWellsHathaway_resize.jpg

400

900

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-07-03 13:40:552025-07-03 15:42:15Methane Matters, but Make Polluters Pay: FracTracker’s Response to Carl Pope

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2019/03/IdleWellsHathaway_resize.jpg

400

900

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-07-03 13:40:552025-07-03 15:42:15Methane Matters, but Make Polluters Pay: FracTracker’s Response to Carl Pope https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/11/Fhn3YgeXkAI0QiX.jpg

675

1200

Katie Jones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Katie Jones2025-07-03 13:22:502026-01-14 17:55:32Shell Polymers Monaca: 17.9 Billion Pounds of Emissions and Repeated Violations in Pennsylvania

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/11/Fhn3YgeXkAI0QiX.jpg

675

1200

Katie Jones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Katie Jones2025-07-03 13:22:502026-01-14 17:55:32Shell Polymers Monaca: 17.9 Billion Pounds of Emissions and Repeated Violations in Pennsylvania https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2016/07/DSC_0266_LowRes.jpg

3000

4496

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-06-30 14:48:532025-07-03 13:47:59Plum Borough Rejects Fracking Waste Injection Well After Public Pushback

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2016/07/DSC_0266_LowRes.jpg

3000

4496

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-06-30 14:48:532025-07-03 13:47:59Plum Borough Rejects Fracking Waste Injection Well After Public Pushback https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/05/51382261216_f8af819a45_o.jpg

1125

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2025-05-31 12:00:592026-03-13 12:05:07Power Plant Locations and Unemployment Rates

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/05/51382261216_f8af819a45_o.jpg

1125

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2025-05-31 12:00:592026-03-13 12:05:07Power Plant Locations and Unemployment Rates https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/04/49770601811_6cc7e18996_k.jpg

716

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2025-04-07 15:42:272025-04-07 15:42:27Pipeline Incidents Are a Daily Occurrence

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/04/49770601811_6cc7e18996_k.jpg

716

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2025-04-07 15:42:272025-04-07 15:42:27Pipeline Incidents Are a Daily Occurrence https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/02/Los-Angeles-skyline-feature-scaled.jpg

667

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2025-03-27 15:37:102025-04-01 12:55:42Environmental Justice Analysis of Oil Extraction in Los Angeles Communities

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/02/Los-Angeles-skyline-feature-scaled.jpg

667

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2025-03-27 15:37:102025-04-01 12:55:42Environmental Justice Analysis of Oil Extraction in Los Angeles Communities https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/03/3_TAuch_Infrastructure-FrackPad-SouthwestPA_April2019.jpg

830

1500

Katie Jones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Katie Jones2025-03-26 14:05:222025-04-01 12:29:01How Increased Protective Buffer Zones Could Help Protect 3.6 million Pennsylvanians

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/03/3_TAuch_Infrastructure-FrackPad-SouthwestPA_April2019.jpg

830

1500

Katie Jones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Katie Jones2025-03-26 14:05:222025-04-01 12:29:01How Increased Protective Buffer Zones Could Help Protect 3.6 million Pennsylvanians https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/02/49727923413_5d7b7335a0_k.jpg

621

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2025-01-31 14:52:292025-02-03 15:59:13Regulatory Gaps and Resistance: The Battle Over Fracking in Southern Illinois

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/02/49727923413_5d7b7335a0_k.jpg

621

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2025-01-31 14:52:292025-02-03 15:59:13Regulatory Gaps and Resistance: The Battle Over Fracking in Southern Illinois https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/02/1400669_062416-kabc-cuffe-erskine1-imgcrtr.jpg

720

1280

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-01-31 12:07:132025-02-06 14:11:38Can California Energy Policy Move Past its Contradictions?

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/02/1400669_062416-kabc-cuffe-erskine1-imgcrtr.jpg

720

1280

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-01-31 12:07:132025-02-06 14:11:38Can California Energy Policy Move Past its Contradictions? FracTracker Alliance, 2024

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/03/ODNR-Oil-and-Gas-Incidents-2018-2023.jpg

844

1500

Gwen Klenke

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Gwen Klenke2025-01-06 11:47:452025-01-06 14:49:36Data Gaps: A Critical Examination of Oil and Gas Well Incidents in Ohio

FracTracker Alliance, 2024

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/03/ODNR-Oil-and-Gas-Incidents-2018-2023.jpg

844

1500

Gwen Klenke

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Gwen Klenke2025-01-06 11:47:452025-01-06 14:49:36Data Gaps: A Critical Examination of Oil and Gas Well Incidents in Ohio Great Plains Action Society

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/10/No-CO2-Ppelines-Sioux-City.jpg

672

1012

Gwen Klenke

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Gwen Klenke2024-10-22 11:55:082024-10-25 12:10:00Indigenous Communities’ Fight Against CO2 Pipelines in the Great Plains

Great Plains Action Society

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/10/No-CO2-Ppelines-Sioux-City.jpg

672

1012

Gwen Klenke

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Gwen Klenke2024-10-22 11:55:082024-10-25 12:10:00Indigenous Communities’ Fight Against CO2 Pipelines in the Great Plains https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/08/Midas6M_RecvFacil_042024_Header.jpg

891

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2024-08-01 20:41:312024-08-02 17:55:17Pennsylvania Oil and Gas Industry Trends: Drilled Wells, Violations, Production, and Waste

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/08/Midas6M_RecvFacil_042024_Header.jpg

891

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2024-08-01 20:41:312024-08-02 17:55:17Pennsylvania Oil and Gas Industry Trends: Drilled Wells, Violations, Production, and Waste https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/06/Hydrogen-molecule-feature.jpg

844

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2024-06-05 17:41:582024-06-06 09:18:40A Closer Look at Risks of the Appalachian Hydrogen Hub

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/06/Hydrogen-molecule-feature.jpg

844

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2024-06-05 17:41:582024-06-06 09:18:40A Closer Look at Risks of the Appalachian Hydrogen Hub FracTracker Alliance, 2024

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/06/Falcon-Pipeline-Violations-2024.jpg

844

1500

Katie Jones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Katie Jones2024-06-05 10:35:022024-06-05 11:36:30Falcon Pipeline Criminal Charges Explained

FracTracker Alliance, 2024

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/06/Falcon-Pipeline-Violations-2024.jpg

844

1500

Katie Jones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Katie Jones2024-06-05 10:35:022024-06-05 11:36:30Falcon Pipeline Criminal Charges Explained https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2016/10/Nix-Pix-050.jpg

3088

4629

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2024-06-04 16:34:592025-05-02 14:53:36The Importance of Surveying Rural Landowners in North Dakota on Fracking

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2016/10/Nix-Pix-050.jpg

3088

4629

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2024-06-04 16:34:592025-05-02 14:53:36The Importance of Surveying Rural Landowners in North Dakota on Fracking https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2016/04/Mount-Carbon-WV-Large.jpg

1429

1888

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2024-06-04 14:18:082024-06-04 16:39:12Exploring the Fallout of Precision Scheduled Rail: A Rail Worker’s Perspective on Precision Scheduled Rail

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2016/04/Mount-Carbon-WV-Large.jpg

1429

1888

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2024-06-04 14:18:082024-06-04 16:39:12Exploring the Fallout of Precision Scheduled Rail: A Rail Worker’s Perspective on Precision Scheduled Rail https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2019/12/Drilling-rig-in-Washington-County-Pennsylvania.jpg

573

2000

Katie Jones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Katie Jones2024-05-02 15:54:282025-05-21 12:33:41Not-So-Radical Transparency: An Ineffective and Unnecessary Partnership Between Pennsylvania Governor Shapiro and the Gas Company CNX

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2019/03/IdleWellsHathaway_resize.jpg

400

900

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2024-05-02 10:32:552024-05-02 12:43:28California Must Improve Management of Idle Wells

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2019/12/Drilling-rig-in-Washington-County-Pennsylvania.jpg

573

2000

Katie Jones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Katie Jones2024-05-02 15:54:282025-05-21 12:33:41Not-So-Radical Transparency: An Ineffective and Unnecessary Partnership Between Pennsylvania Governor Shapiro and the Gas Company CNX

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2019/03/IdleWellsHathaway_resize.jpg

400

900

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2024-05-02 10:32:552024-05-02 12:43:28California Must Improve Management of Idle Wells https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/10/gilooly-farmer-pa-2013.jpg

823

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2024-04-26 11:34:082024-04-29 09:39:15Holes in FracFocus

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/10/gilooly-farmer-pa-2013.jpg

823

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2024-04-26 11:34:082024-04-29 09:39:15Holes in FracFocus FracTracker Alliance, 2024

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/03/WV-PFAS-Map.jpeg

763

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2024-03-29 15:06:512024-03-29 15:42:29Mapping PFAS Chemicals Used in Fracking Operations in West Virginia

FracTracker Alliance, 2024

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/03/WV-PFAS-Map.jpeg

763

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2024-03-29 15:06:512024-03-29 15:42:29Mapping PFAS Chemicals Used in Fracking Operations in West Virginia https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2020/04/California-well-pad.jpg

666

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2024-03-07 17:01:582024-03-12 09:55:39Chevron’s $2.3 Billion Asset Adjustment Raises Questions Amidst Regulatory Changes in California

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2020/04/California-well-pad.jpg

666

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2024-03-07 17:01:582024-03-12 09:55:39Chevron’s $2.3 Billion Asset Adjustment Raises Questions Amidst Regulatory Changes in California Ross incinerator in Eaton Township. Photo by Ted Auch, FracTracker Alliance, 2023

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/02/52748252528_19364d2943_k.jpg

918

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2024-02-07 21:56:582024-02-09 13:47:09Stop Toxic Threat: A Heavy Industrial Zoning Battle

Ross incinerator in Eaton Township. Photo by Ted Auch, FracTracker Alliance, 2023

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/02/52748252528_19364d2943_k.jpg

918

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2024-02-07 21:56:582024-02-09 13:47:09Stop Toxic Threat: A Heavy Industrial Zoning Battle Ross Environmental Hazardous Waste Incinerator in Eaton Township, Ohio. Ted Auch, FracTracker Alliance, 2023

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/02/52747231757_2834f8bd30_k.jpg

1124

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2024-02-01 22:00:352024-02-09 13:45:10East Palestine Warning: The Growing Threat From Hazardous Waste Storage

Ross Environmental Hazardous Waste Incinerator in Eaton Township, Ohio. Ted Auch, FracTracker Alliance, 2023

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/02/52747231757_2834f8bd30_k.jpg

1124

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2024-02-01 22:00:352024-02-09 13:45:10East Palestine Warning: The Growing Threat From Hazardous Waste Storage FracTracker Alliance, 2024

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/01/California-Daily-Oil-Production-2024.jpg

844

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2024-01-30 05:00:012024-02-05 13:46:42Index of Oil and Gas Operator Health in California Shows Risks to State Economy and Taxpayers

FracTracker Alliance, 2024

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/01/California-Daily-Oil-Production-2024.jpg

844

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2024-01-30 05:00:012024-02-05 13:46:42Index of Oil and Gas Operator Health in California Shows Risks to State Economy and Taxpayers The cottage along Slope Creek, months after being vacated due to health concerns caused by nearby oil and gas operations. Photo courtesy of Chloe Mankin

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/01/slopecreek2018.jpg

845

1500

Chloe Mankin

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Chloe Mankin2024-01-12 12:51:302024-01-12 16:32:21Calling for Change: Life on the Fracking Frontlines

The cottage along Slope Creek, months after being vacated due to health concerns caused by nearby oil and gas operations. Photo courtesy of Chloe Mankin

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/01/slopecreek2018.jpg

845

1500

Chloe Mankin

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Chloe Mankin2024-01-12 12:51:302024-01-12 16:32:21Calling for Change: Life on the Fracking Frontlines https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/12/Figure-6-Rail-Population.jpg

801

1498

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2023-12-14 16:26:372023-12-15 11:47:53On the Wrong Track: Risks to Residents of the Upper Ohio River Valley From Railroad Incidents

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/12/Figure-6-Rail-Population.jpg

801

1498

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2023-12-14 16:26:372023-12-15 11:47:53On the Wrong Track: Risks to Residents of the Upper Ohio River Valley From Railroad Incidents Matt Kelso, FracTracker Alliance, 2023

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/11/DSCN1328.jpg

1125

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2023-11-16 13:25:082025-03-06 15:39:23Digital Atlas: Exploring Nature and Industry in the Raccoon Creek Watershed

Matt Kelso, FracTracker Alliance, 2023

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/11/DSCN1328.jpg

1125

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2023-11-16 13:25:082025-03-06 15:39:23Digital Atlas: Exploring Nature and Industry in the Raccoon Creek Watershed https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/10/RusticRidge_102023.jpg

1119

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2023-11-09 19:01:252025-08-12 13:45:14Why Do Houses Keep Exploding in One Pennsylvania Suburb?

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/10/RusticRidge_102023.jpg

1119

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2023-11-09 19:01:252025-08-12 13:45:14Why Do Houses Keep Exploding in One Pennsylvania Suburb? https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/10/Wells-Within-3200-Feet-of-Schools-Childcare-CA.jpg

595

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-10-04 16:38:472023-10-04 21:19:54Oil and Gas Activity Within California Public Health Protection Zones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/10/Wells-Within-3200-Feet-of-Schools-Childcare-CA.jpg

595

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-10-04 16:38:472023-10-04 21:19:54Oil and Gas Activity Within California Public Health Protection Zones https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/05/Colorado-Water-Use-5.2.23.jpg

589

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-05-02 12:33:532026-04-23 15:43:28Evaluation of the Capacity for Water Recycling for Colorado Oil and Gas Extraction Operations

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/05/Colorado-Water-Use-5.2.23.jpg

589

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-05-02 12:33:532026-04-23 15:43:28Evaluation of the Capacity for Water Recycling for Colorado Oil and Gas Extraction Operations Sarah Carballo, FracTracker Alliance, 2022

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/04/DSC_0855.jpg

1001

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2023-04-27 13:46:002023-04-27 14:18:17Evidence Shows Oil and Gas Companies Use PFAS in New Mexico Wells

Sarah Carballo, FracTracker Alliance, 2022

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/04/DSC_0855.jpg

1001

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2023-04-27 13:46:002023-04-27 14:18:17Evidence Shows Oil and Gas Companies Use PFAS in New Mexico Wells https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/04/Rework-Permits-Feature-Image.png

506

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-04-14 11:36:392023-04-28 16:05:23CalGEM Permit Review Q1 2023: Well Rework Permits Increase by 76% in California

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/04/Rework-Permits-Feature-Image.png

506

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-04-14 11:36:392023-04-28 16:05:23CalGEM Permit Review Q1 2023: Well Rework Permits Increase by 76% in California Ted Auch, FracTracker Alliance, 2022

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/02/DSC_1026_LowRes.jpg

1000

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2023-02-01 15:36:182023-02-01 17:01:372022 Pipeline Incidents Update: Is Pipeline Safety Achievable?

Ted Auch, FracTracker Alliance, 2022

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/02/DSC_1026_LowRes.jpg

1000

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2023-02-01 15:36:182023-02-01 17:01:372022 Pipeline Incidents Update: Is Pipeline Safety Achievable? https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2020/09/Methane_Air_WaterQualityConcerns-1.jpg

534

800

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2023-01-31 15:01:342023-02-27 16:43:15Testimony On EPA’s Proposed Methane Pollution Standards for the Oil and Gas Industry

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2020/09/Methane_Air_WaterQualityConcerns-1.jpg

534

800

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2023-01-31 15:01:342023-02-27 16:43:15Testimony On EPA’s Proposed Methane Pollution Standards for the Oil and Gas Industry https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/01/California-Rework-Permits-2023.jpg

541

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-01-24 09:01:352023-01-24 13:21:55Assessment of Rework Permits on Oil Production from Operational Wells Within the 3,200-Foot Public Health Protection Zone

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/01/California-Rework-Permits-2023.jpg

541

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-01-24 09:01:352023-01-24 13:21:55Assessment of Rework Permits on Oil Production from Operational Wells Within the 3,200-Foot Public Health Protection Zone https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/01/CalGEM-Q4-2022-Permit-Review.jpg

570

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-01-18 18:01:532023-01-18 18:03:23CalGEM Permit Review Q4 2022: Oil Permit Approvals Show Steep Rise Within Protective Buffer Zones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/01/CalGEM-Q4-2022-Permit-Review.jpg

570

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-01-18 18:01:532023-01-18 18:03:23CalGEM Permit Review Q4 2022: Oil Permit Approvals Show Steep Rise Within Protective Buffer Zones https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/03/TAuch_Transportation-RoverPipeline_Construction-EnergyTransferPartners-Woodsfield_OH_May2017.jpg

576

1500

Karen Edelstein

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Karen Edelstein2022-11-30 17:50:122024-01-22 16:03:23A Contentious Landscape of Pipeline Build-outs in the Eastern US

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/03/TAuch_Transportation-RoverPipeline_Construction-EnergyTransferPartners-Woodsfield_OH_May2017.jpg

576

1500

Karen Edelstein

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Karen Edelstein2022-11-30 17:50:122024-01-22 16:03:23A Contentious Landscape of Pipeline Build-outs in the Eastern US https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/11/Rager-Mountain-Feature.jpg

636

1500

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2022-11-30 14:12:222023-02-03 13:50:48Major Gas Leak Reveals Risks of Aging Gas Storage Wells in Pennsylvania

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/11/Rager-Mountain-Feature.jpg

636

1500

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2022-11-30 14:12:222023-02-03 13:50:48Major Gas Leak Reveals Risks of Aging Gas Storage Wells in Pennsylvania https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/11/DSC_1359_HighRes.jpg

1000

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2022-11-23 15:15:112025-03-06 15:40:10Coursing Through Gasland: A Digital Atlas Exploring Natural Gas Development in the Towanda Creek Watershed

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/11/Fhn3YgeXkAI0QiX.jpg

675

1200

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2022-11-17 16:43:392022-11-18 13:41:39Falcon Pipeline Online, Begins Operations Following Violations of Clean Streams Law

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/11/DSC_1359_HighRes.jpg

1000

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2022-11-23 15:15:112025-03-06 15:40:10Coursing Through Gasland: A Digital Atlas Exploring Natural Gas Development in the Towanda Creek Watershed

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/11/Fhn3YgeXkAI0QiX.jpg

675

1200

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2022-11-17 16:43:392022-11-18 13:41:39Falcon Pipeline Online, Begins Operations Following Violations of Clean Streams Law https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/10/Columbus-Source-Water.jpg

605

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-10-31 21:39:022022-11-29 14:24:38Synopsis: Risks to the Greater Columbus Water Supply from Oil and Gas Production

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/10/Columbus-Source-Water.jpg

605

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-10-31 21:39:022022-11-29 14:24:38Synopsis: Risks to the Greater Columbus Water Supply from Oil and Gas Production https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/09/DSC_1021_LowRes__1607617394306__w1920-e1663613850641.jpg

667

1500

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2022-09-19 15:08:172022-11-03 11:56:26Desalination: The Chemical Industry’s Demand for Water in Texas

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/09/DSC_1021_LowRes__1607617394306__w1920-e1663613850641.jpg

667

1500

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2022-09-19 15:08:172022-11-03 11:56:26Desalination: The Chemical Industry’s Demand for Water in Texas https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/06/LKrop_infrastructure-offshoredrilling-drillrigs-SantaBarbara-CA_EnvrDefenseCtr_Aug20131-e1663254826557.jpg

178

400

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2022-09-06 13:32:202022-09-15 11:14:03Take Action in Support of No New Leases

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/06/LKrop_infrastructure-offshoredrilling-drillrigs-SantaBarbara-CA_EnvrDefenseCtr_Aug20131-e1663254826557.jpg

178

400

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2022-09-06 13:32:202022-09-15 11:14:03Take Action in Support of No New Leases https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/08/51119572588_132e0366c1_k_1-e1663254774314.jpg

607

1364

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-08-31 14:33:482022-09-15 16:29:45Carbon Capture and Storage: Developments in the Law of Pore Space in North Dakota

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/08/51119572588_132e0366c1_k_1-e1663254774314.jpg

607

1364

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-08-31 14:33:482022-09-15 16:29:45Carbon Capture and Storage: Developments in the Law of Pore Space in North Dakota https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2017/03/DSC_0341_to_0345_LowRes2-e1663254589691.jpg

667

1500

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2022-08-31 12:54:012023-12-07 14:33:18Carbon Capture and Storage: Industry Connections and Community Impacts

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2017/03/DSC_0341_to_0345_LowRes2-e1663254589691.jpg

667

1500

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2022-08-31 12:54:012023-12-07 14:33:18Carbon Capture and Storage: Industry Connections and Community Impacts https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/08/ExxonMobil-LaBarge-CCUS-e1663254477876.jpg

465

1047

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2022-08-31 11:19:122022-09-15 11:08:15Carbon Capture and Storage: Fact or Fiction?

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/08/ExxonMobil-LaBarge-CCUS-e1663254477876.jpg

465

1047

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2022-08-31 11:19:122022-09-15 11:08:15Carbon Capture and Storage: Fact or Fiction? https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/08/MOV_8837_Moment-e1663254387862.jpg

284

640

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-08-22 09:52:582026-04-28 14:45:28FracTracker Finds Widespread Hydrocarbon Emissions from Active & Idle Oil and Gas Wells and Infrastructure in California

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/08/MOV_8837_Moment-e1663254387862.jpg

284

640

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-08-22 09:52:582026-04-28 14:45:28FracTracker Finds Widespread Hydrocarbon Emissions from Active & Idle Oil and Gas Wells and Infrastructure in California https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/07/kyle-ferrar-e1663254307641.jpg

636

1430

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-07-29 19:04:322022-09-15 11:05:17California Regulators Approve More Oil Well Permits Amid a Crisis of Leaking Oil Wells that Should be Plugged

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/07/kyle-ferrar-e1663254307641.jpg

636

1430

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-07-29 19:04:322022-09-15 11:05:17California Regulators Approve More Oil Well Permits Amid a Crisis of Leaking Oil Wells that Should be Plugged https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/06/CCSHFeatureImage.jpg

667

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-06-23 15:29:312022-06-30 12:30:43An Insider Take on the Appalachian Hydrogen & CCUS Conference

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/06/CCSHFeatureImage.jpg

667

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-06-23 15:29:312022-06-30 12:30:43An Insider Take on the Appalachian Hydrogen & CCUS Conference https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/06/TAuch_Infrastructure-OilRefinery_DowntownToledo-ToledoOil-LucasCounty-OH_Lighthawk_Sept2021.jpg

667

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2022-06-21 15:46:522024-06-18 10:53:27Does Hydrogen Have a Role in our Energy Future?

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/06/TAuch_Infrastructure-OilRefinery_DowntownToledo-ToledoOil-LucasCounty-OH_Lighthawk_Sept2021.jpg

667

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2022-06-21 15:46:522024-06-18 10:53:27Does Hydrogen Have a Role in our Energy Future? https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/05/Brine-spreading-map-feature-1.jpg

667

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-05-13 16:19:112022-08-10 15:43:05Oil and Gas Brine in Ohio

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/05/Brine-spreading-map-feature-1.jpg

667

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-05-13 16:19:112022-08-10 15:43:05Oil and Gas Brine in Ohio https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/05/DustingHighVolDirtyFilter-feature.jpg

667

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-05-03 09:37:492022-05-03 09:37:49PA Environment Digest Blog: Conventional Oil & Gas Drillers Dispose Of Drill Cuttings By ‘Dusting’

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/05/DustingHighVolDirtyFilter-feature.jpg

667

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-05-03 09:37:492022-05-03 09:37:49PA Environment Digest Blog: Conventional Oil & Gas Drillers Dispose Of Drill Cuttings By ‘Dusting’ https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/04/TAuch_Cultural-Harvey_FamilyFarm_NEXUS_Pipeline-DTEEnergy_Enbridge-ChippewaLake_MedinaCounty_OH_May20183-feature.jpg

667

1500

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2022-04-28 14:12:552022-04-28 14:12:55Real Talk on Pipelines

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/04/TAuch_Cultural-Harvey_FamilyFarm_NEXUS_Pipeline-DTEEnergy_Enbridge-ChippewaLake_MedinaCounty_OH_May20183-feature.jpg

667

1500

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2022-04-28 14:12:552022-04-28 14:12:55Real Talk on Pipelines https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/04/TAuch_Infrastructure-Compressor_Cryogenic_Complex-MarkWest_EnergyTransfer-WashingtonCounty-PA_Sept2021-feature.jpg

667

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2022-04-28 13:37:312023-03-09 14:03:402021 Production from Pennsylvania’s Oil and Gas Wells

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/04/TAuch_Infrastructure-Compressor_Cryogenic_Complex-MarkWest_EnergyTransfer-WashingtonCounty-PA_Sept2021-feature.jpg

667

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2022-04-28 13:37:312023-03-09 14:03:402021 Production from Pennsylvania’s Oil and Gas Wells https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/04/Russia-Ukraine-Energy-feature.jpg

667

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2022-04-20 13:25:452022-04-20 17:23:17Mapping Energy Systems Impacted by the Russia-Ukraine War

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/04/Russia-Ukraine-Energy-feature.jpg

667

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2022-04-20 13:25:452022-04-20 17:23:17Mapping Energy Systems Impacted by the Russia-Ukraine War https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/04/IMG_5940-1.jpg

1125

1500

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2022-04-11 16:48:092022-04-20 13:23:14Dimock residents working to protect water from a new threat: fracking waste

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/04/IMG_5940-1.jpg

1125

1500

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2022-04-11 16:48:092022-04-20 13:23:14Dimock residents working to protect water from a new threat: fracking waste https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/03/KFerrar-feature-CAsetbacks2022.jpg

878

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-04-06 12:01:332023-08-24 19:08:53Implications of a 3,200-foot Setback in California

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/03/KFerrar-feature-CAsetbacks2022.jpg

878

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-04-06 12:01:332023-08-24 19:08:53Implications of a 3,200-foot Setback in California https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/03/BLenker_infrastructure-oilrig-southLA-CA_Oct20173.jpg

795

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-03-15 16:32:032022-03-15 18:00:00New Trends in Drilling Permit Approvals Take Shape in CA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/03/BLenker_infrastructure-oilrig-southLA-CA_Oct20173.jpg

795

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-03-15 16:32:032022-03-15 18:00:00New Trends in Drilling Permit Approvals Take Shape in CA https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/03/KFerrar-CAlegislative-analysis_March2022.jpg

720

1280

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-03-14 15:18:402022-03-14 15:18:40Oil and Gas Drilling in California Legislative Districts

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/03/KFerrar-CAlegislative-analysis_March2022.jpg

720

1280

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-03-14 15:18:402022-03-14 15:18:40Oil and Gas Drilling in California Legislative Districts https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/01/PFAS-wells-in-Colorado-Feature.jpg

667

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2022-01-31 16:36:332022-01-31 16:36:33New Report: Fracking with “Forever Chemicals” in Colorado

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/01/PFAS-wells-in-Colorado-Feature.jpg

667

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2022-01-31 16:36:332022-01-31 16:36:33New Report: Fracking with “Forever Chemicals” in Colorado https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/01/FeatImage_MK.jpg

935

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2022-01-20 15:32:142022-01-20 15:32:14Introducing: FracTracker’s comprehensive new Pennsylvania map!

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/01/FeatImage_MK.jpg

935

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2022-01-20 15:32:142022-01-20 15:32:14Introducing: FracTracker’s comprehensive new Pennsylvania map! https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/12/173695136_1422048161521006_7197500259062906334_n.jpg

667

1500

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2021-12-01 15:27:402021-12-01 15:27:40New Letter from Federal Regulators Regarding how the Falcon has Been Investigated

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/12/173695136_1422048161521006_7197500259062906334_n.jpg

667

1500

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2021-12-01 15:27:402021-12-01 15:27:40New Letter from Federal Regulators Regarding how the Falcon has Been Investigated https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/11/TAuch_Infrastructure-naturalgas-powerplant-construction-Caithness-GuernseyCounty-OH_April2021.jpg

667

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2021-12-01 15:20:152022-01-04 17:53:55US Army Corps Muskingum Watershed Plan ignores local concerns of oil and gas effects

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/11/TAuch_Infrastructure-naturalgas-powerplant-construction-Caithness-GuernseyCounty-OH_April2021.jpg

667

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2021-12-01 15:20:152022-01-04 17:53:55US Army Corps Muskingum Watershed Plan ignores local concerns of oil and gas effects https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/11/TAuch_Plastics_Refinery_TankFarm_Terminal-Trafigura_CorpusChristiPolymers_Valero_Citgo_FlintHillsResources-CorpusChristi_TX_LightHawk_Nov2019-feature.jpg

667

1500

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2021-11-05 09:43:472021-11-05 09:47:30Southeastern Texas Petrochemical Industry Needs 318 Billion Gallons of Water, but the US EPA Says Not So Fast

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/11/TAuch_Plastics_Refinery_TankFarm_Terminal-Trafigura_CorpusChristiPolymers_Valero_Citgo_FlintHillsResources-CorpusChristi_TX_LightHawk_Nov2019-feature.jpg

667

1500

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2021-11-05 09:43:472021-11-05 09:47:30Southeastern Texas Petrochemical Industry Needs 318 Billion Gallons of Water, but the US EPA Says Not So Fast https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/10/Chickahominy-feature.jpg

667

1500

Karen Edelstein

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Karen Edelstein2021-11-01 13:29:122021-12-17 11:53:41Chickahominy Pipeline project tries to exploit an apparent regulatory loophole

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/10/Chickahominy-feature.jpg

667

1500

Karen Edelstein

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Karen Edelstein2021-11-01 13:29:122021-12-17 11:53:41Chickahominy Pipeline project tries to exploit an apparent regulatory loophole https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/10/Mariner-East-2-feature.jpg

667

1500

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2021-10-29 13:02:432021-11-01 12:17:20Map Update on Criminal Charges Facing Mariner East 2 Pipeline

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/10/Mariner-East-2-feature.jpg

667

1500

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2021-10-29 13:02:432021-11-01 12:17:20Map Update on Criminal Charges Facing Mariner East 2 Pipeline https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/09/NRDC-Urban-Drilling-feature.jpg

667

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2021-09-14 14:26:442026-04-28 14:29:26It’s Time to Stop Urban Oil Drilling in Los Angeles

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/09/NRDC-Urban-Drilling-feature.jpg

667

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2021-09-14 14:26:442026-04-28 14:29:26It’s Time to Stop Urban Oil Drilling in Los Angeles https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/08/Texas-Infrastructure-Feature-.jpg

667

1500

Intern FracTracker

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Intern FracTracker2021-09-14 08:00:002022-01-24 17:49:20Infrastructure Networks in Texas

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/08/Texas-Infrastructure-Feature-.jpg

667

1500

Intern FracTracker

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Intern FracTracker2021-09-14 08:00:002022-01-24 17:49:20Infrastructure Networks in Texas https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/09/National-Prison-Strike-poster-feature.jpg

667

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2021-09-09 08:00:082021-09-08 17:30:46California Prisons are Within 2,500’ of Oil and Gas Extraction

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/09/National-Prison-Strike-poster-feature.jpg

667

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2021-09-09 08:00:082021-09-08 17:30:46California Prisons are Within 2,500’ of Oil and Gas Extraction https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/08/kemap.jpg

400

900

Karen Edelstein

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Karen Edelstein2021-08-26 11:19:442021-08-26 15:08:04New power plant proposal called senseless and wasteful by climate groups

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/08/kemap.jpg

400

900

Karen Edelstein

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Karen Edelstein2021-08-26 11:19:442021-08-26 15:08:04New power plant proposal called senseless and wasteful by climate groups https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/03/Falcon-Ohio-River-Crossing-Feature-A.LauschkeLightHawk-scaled.jpg

667

1500

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2021-08-24 07:15:232021-08-23 17:30:12Ongoing Safety Concerns over Shell’s Falcon Pipeline

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/03/Falcon-Ohio-River-Crossing-Feature-A.LauschkeLightHawk-scaled.jpg

667

1500

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2021-08-24 07:15:232021-08-23 17:30:12Ongoing Safety Concerns over Shell’s Falcon Pipeline https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/08/BLenker_infrastructure-oilrig-southLA-CA_Oct2017-feature.jpg

667

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2021-08-05 16:38:392021-08-05 16:38:39New Neighborhood Drilling Permits Issued While California Fails to Act on Public Health Rules

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/08/BLenker_infrastructure-oilrig-southLA-CA_Oct2017-feature.jpg

667

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2021-08-05 16:38:392021-08-05 16:38:39New Neighborhood Drilling Permits Issued While California Fails to Act on Public Health Rules https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/08/Bitcoin-feature.jpg

667

1500

Karen Edelstein

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Karen Edelstein2021-08-02 17:05:372022-01-04 10:48:28The world is watching as bitcoin battle brews in the US

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/08/Bitcoin-feature.jpg

667

1500

Karen Edelstein

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Karen Edelstein2021-08-02 17:05:372022-01-04 10:48:28The world is watching as bitcoin battle brews in the US https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/07/Lycoming-feature.jpg

667

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2021-07-27 09:58:142021-07-28 11:23:19Lycoming Watershed Digital Atlas

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/07/Lycoming-feature.jpg

667

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2021-07-27 09:58:142021-07-28 11:23:19Lycoming Watershed Digital Atlas https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/07/California-oil-drilling-feature.jpg

400

900

Kyle Ferrar, MPH