https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/03/Web-Elements-Map-thumbnails-28.png

500

750

Shannon Smith

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Shannon Smith2026-06-12 15:27:012026-06-12 15:41:18PA DEP Approves Unusual “Mineral Brine” Well in Erie County, Raising Concerns About New Regulatory Loophole

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/03/Web-Elements-Map-thumbnails-28.png

500

750

Shannon Smith

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Shannon Smith2026-06-12 15:27:012026-06-12 15:41:18PA DEP Approves Unusual “Mineral Brine” Well in Erie County, Raising Concerns About New Regulatory LoopholeAssessment of Oil and Gas Well Ownership Transfers in California

Overview

The California Council on Science and Technology has outlined the economic risk to California resulting from asset retirement obligations related to the plugging, properly abandoning, and remediation of oil and gas well sites. Their report, published in 2018, estimates that the net cost for and plugging oil and gas operations in California amount to at least $9B, although this estimate does not include site reclamation and the maintenance costs associated with re-plugging wells in the future, as plugged and abandoned wells age. A recent Carbon Tracker report puts the current estimate as high as $21B when inflation is considered and site reclamation included.

Plugging just the currently orphan wells in the state is estimated to cost at least $550M. While drilling a new well in California requires a surety bond, reports show that the bonding amounts are substantially deficient to fulfill clean-up costs. The CCST report concluded that, at the time of publication (2020), the average cost to plug and abandon a well was $68,000, but the average bond funding available per well is only about $1. In total, the bonded value does not even cover what is currently needed to plug known orphan wells, and the counts of orphan wells is expected to vastly increase as CalGEM completes its audit of idle wells. Bonded funds are deficient for a number of reasons, including updated bonding requirements were not adopted by California until 2018 and the ability of operators to purchase one ‘blanket’ bond to cover many wells at discounted rates. Operators that already carry blanket bond indemnity will not typically have to increase their bonding coverage when they acquire additional wells.

This report assesses the risk that the problem of orphan wells in California will continue to grow as a result of transfers of wells to operators who are ultimately unable to properly plug and remediate them. A major risk factor for wells becoming orphaned is the tendency of the larger operators who originally drilled wells and operated them when they were at full production volumes to divest themselves of those wells when production declines or the well becomes idle. Low production and idle wells are regularly and repeatedly sold to progressively less solvent operators. This process increases the risk that these less solvent operators will become insolvent and unable to comply with their plugging and abandonment obligations.

This report therefore explores the regulatory data to determine whether transfers of oil and gas well ownership are occurring as a result of financially healthy oil companies pursuing new investment opportunities in reservoir development, or rather a mechanism for oil and gas companies to shed well plugging and reclamation obligations. In order to assess the financial nature of well ownership transfers, CalGEM data was compiled to identify when well ownership transfers had occurred and identify both the divesting and acquiring companies. Both the divesting and acquiring companies were categorized based on several categories. These categories included whether the companies had declared bankruptcy, had divested from California exploration and production operations, had been created out of parent company divestment, and their historical production volumes reported to CalGEM. The proportions of well transfers that fall into each category are reported and discussed.

CalGEM Operator Transfers

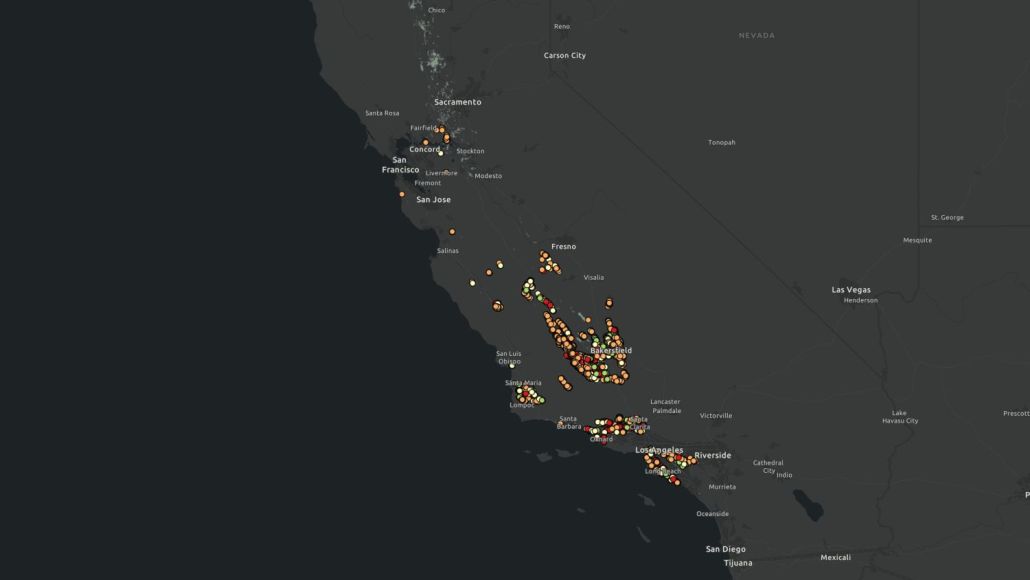

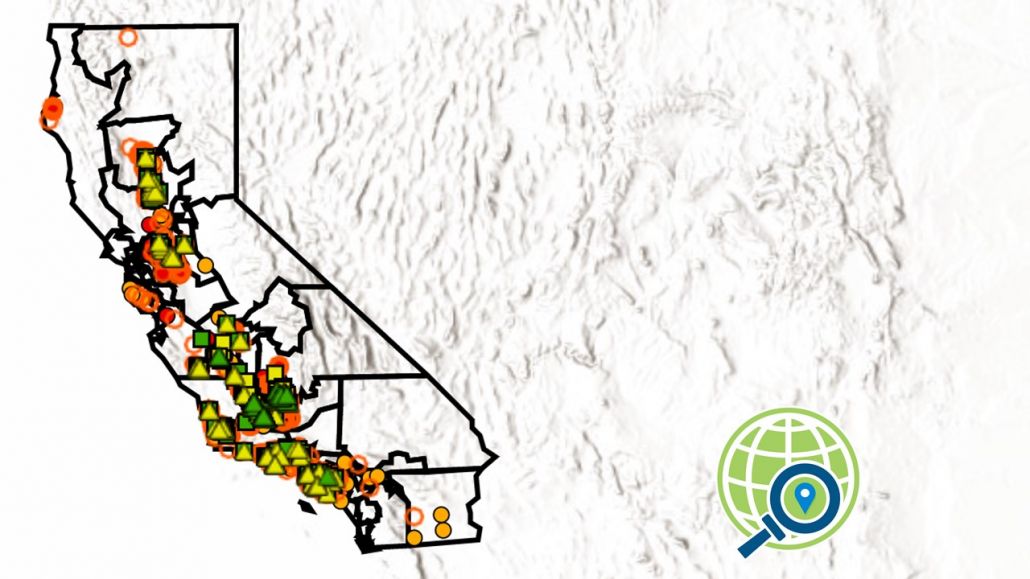

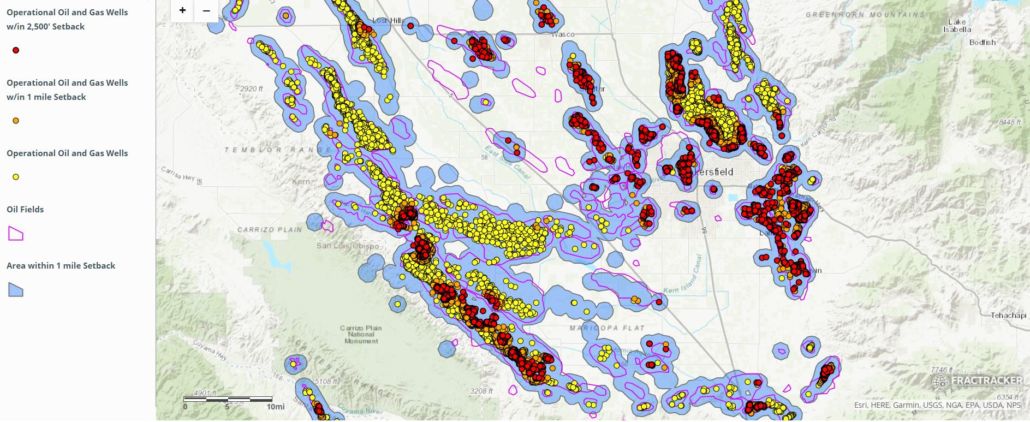

This interactive map looks at CalGEM oil and gas wells that have changed ownership 1977-2022. The dataset of well transfers compiled for this report was used to map the locations of wells that were transferred between operators.

View the map “Details” tab below in the top right corner to learn more and access the data, or click on the map to explore the dynamic version of this data. Data sources are also listed at the end of this article.

In order to turn layers on and off in the map, use the Layers dropdown menu. This tool is only available in Full Screen view.

Items will activate in this map dependent on the level of zoom in or out.

View Full Size Map | Updated 5/18/2023 | Map Tutorial

Methods

Data Preparation

Datasets utilized included the annual CalgEM production and injection datasets (1977-2021), as well as the AllWells.csv dataset, downloaded (5/2/23), to represent 2022/current ownership, and CalGEM weekly summary of permit notices. The “OilandGasWells” tables from the production and injection datasets were exported from the Microsoft Access databases and merged together (along with the AllWells.csv file) using Python v3.9.12. Duplicate American Petroleum Institute identification numbers (APIs) were removed and the ‘Operator Code’ column data was cleaned and revised to prevent duplicate operators.

The first year of reported production was identified for each well API, and the operator code listed for each well’s first year of production and each year following was compared with the operator listed in the most current (5/3/23) AllWells.csv dataset. To identify the year of transfer, operator codes reported in each production year dataset were compared to the previous year’s operator code. Changes in operator code between individual years were summed for each year. Additional fields from the annual production data were conserved, including well status for the year of ownership transfer.

Of the total (N= 238,151) unique API’s identified, about 20% (50,173) were only listed in the AllWells.csv and not in annual production reports. This contingent was not able to be screened against previous years. The figures reported in this analysis should therefore be considered a lower bound of the estimate of the count of wells that have changed ownership. While this subset was not screened against previous years, the dataset was screened for a list of operators known to have transferred ownership of all wells via a declared bankruptcy, via an LLC created by a separate operator to dump liabilities, or by an operator that fully divested of California assets. Operators included California Resources Corporation and subsidiaries, Occidental Petroleum, Venoco, Greka, Rincon Island Limited Partnership, Exxon Mobil, Shell and subsidiaries, and Aera. Wells drilled after the Occidental Petroleum divestment in 2014 and continuously operated by California Resources Corp were not included in the counts of transferred wells, as they did not change ownership.

Data analysis

Wells that changed ownership were classified based on the nature of the transfer. Both the status of the divestment and the acquisition were categorized. The economic standing of each operator was considered. Knowledge of bankruptcies for larger operators was collected via SEC 10-K filings and regulatory reports, but comprehensive knowledge of all oil and gas operator bankruptcies was not possible. This report therefore likely under-reports the counts of wells that transferred ownership as a result of bankruptcies. The same goes for the ‘marginal operator’ counts in the acquisition category.

Divestment Categories

-

Bankruptcy – Wells that transferred ownership as a result of a bankruptcy by the parent operator.

-

Divestment – Transferred from an operating company with existing active wells to a different operator.

-

California exit divestment – Transferred from an operator that divested from California exploration and production (active or idle). An example is Aera Energy, but also includes many smaller operators Chevron and Berry could be soon to follow.

-

Likely insolvent divestment – Wells transferred from an operator that no longer profits from active wells in California, but has unplugged idle well liabilities within the state.

Acquisition Categories

-

Marginal Operator – Wells transferred to a new operator that was created by the previous operator via an exchange of debt for credit type of divestment, such as California Resources Corporation and its subsidiaries.

-

Investment Asset – Wells transferred to a larger or similarly sized operator.

-

Investment Liability – Wells transferred to a smaller operator.

These categories were created to understand whether wells were being purchased by smaller operators more likely to orphan wells, or if the well transfers were investments by larger operators with the intention of redeveloping the wells. Operators were ranked by production to assess whether wells were transferred to larger or smaller operator. Total lifetime oil production for each operator (1977-2021) was summed using CalGEM annual production datasets. Transfers that went from a larger operator to a smaller operator were tagged as ‘investment liabilities’, and wells that were transferred from smaller operators to larger operators were tagged as ‘investment assets’. To be conservative, exchanges among the top 10 state producers or between similarly sized operators (within 10 rank points) were categorized as investment assets regardless of rank differential. Wells transferred to the State Lands Commission and those to marginal operators that were created out of parent company divestitures such as California Resources Corp. and subsidiaries were counted as investment liabilities due to these operators’ inherent risk of insolvency.

The dataset for the analysis and the python code can be found here.

Results

As a threshold matter, to assess the frequency of this type of divestiture, California Department of Geological Energy Management’s (CalGEMs) well production and injection annual summary reports were screened for changes in ownership of individual oil and gas wells. Results show that of the nearly (N=238,151) unique oil and gas well IDs listed in the production and injection reports, a total of at least 121,726 (51.1%) wells have changed ownership between 1977 and 2022. A significant proportion (at least 13%) of these wells have changed ownership more than one time – since 1977 there have been a total of at least 137,063 transfers of ownership for wells, as reported by CalGEM. The vast majority of these transfers have occurred since 2010 (99.7%). The plot in Figure 2 below shows the cumulative count of wells that have changed ownership between 1977 and 2020. The map in Figure 1 (above) shows the locations of the wells that have changed ownership.

Figure 2. Cumulative Count of Unique Wells Transferred by Year, 1978-2022. The plot shows the counts of wells that changed ownership each year, according to CalGEM data. There were an additional 15,983 wells that changed ownership during this time frame, but the specific year ownership was transferred was not able to be determined. Major transfer events viewable in the plot include divestments by Berry Petroleum Co in 2010, the transfer of wells from Occidental to California Resources Corporation in 2014/2015, the bankruptcy of Venoco Inc. and Linn Energy LLC in 2016/2017, major divestments by Chevron in 2018, and the divestment of Aera Energy LLC from California in 2021.

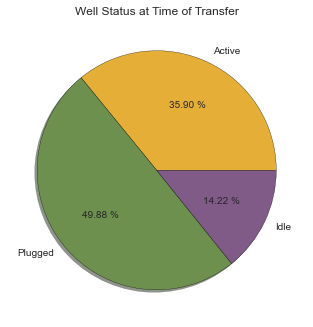

The results of the divestment and acquisition categorization are split into two components due to the high counts of plugged wells that were transferred between operators. Data for operational wells, with statuses of active or idle at the time of transfer, is presented separately from counts of plugged well transfers. The proportions of transferred well statuses is shown below in the pie chart in Figure 3. Nearly half of all the wells transferred between operators were plugged wells, while just over 35% of the well transfers were for active wells.

Figure 3. Pie chart of well statuses. Well statuses were identified for the year of ownership transfers, based on CalGEM annual production and injection reports. Nearly half of well transfers were for plugged wells, while active wells only accounted for about 36%.

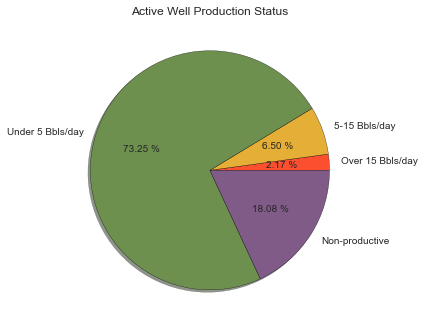

Over a third of the well transfers were for active wells. The category “active” refers to wells that consistently produce monthly volumes of oil or gas, or inject fluids underground. However, it is important to note that the majority of active wells produce stripper or marginal volumes in California (for definitions of stripper or marginal volumes see the glossary). CalGEM production data shows that the majority of transferred active wells were stripper wells that produced less than 15 bbls/day of oil or less than 90 MCF/day of gas (97.8%), and over 91% of wells transferred produced less than 5 bbls/day. Of the total population of wells transferred since 1977, only 2.2% produced more than 15 bbls/day, meaning that just 2.2% of wells transferred produced above the stripper well threshold. In Figure 4 below, the data is limited to ‘active’ wells, to show the counts of actively producing wells that produced volumes of oil above stripper volumes and within additional production brackets.

Figure 4. Pie chart of production status of active wells. Annual production volume totals were quantified for active wells the same year as the reported operator transfers. About 2% of active well transfers were for non-stripper wells (wells producing more than 15 bbls/day). Over 91% of active well transfers were for wells producing less than 5 bbls/day.

Divestments

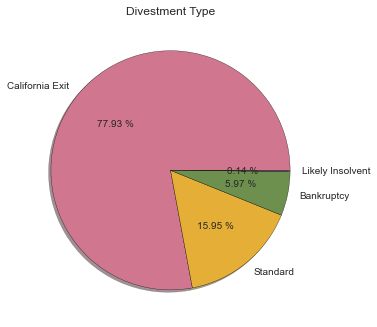

Each data point (well transfer) was summarized in two ways in order to fully understand the flow of assets and liabilities from operator to operator. First the nature of the divestment was analyzed based on the economic status of the divesting operator. The pie chart in Figure 5 shows the results of this categorization. The majority of well transfers were the result of California exit divestment (operators completely divesting from California exploration and production), while about 16% of transfers were between two active operators. Nearly 6% of well transfers were from operators that declared Chapter 7 bankruptcy. Many of those wells are now the responsibility of the state lands commission to plug and remediate. A small percentage of the well transfers (0.14%) were from operators with idle well liabilities without active wells to fund remediation efforts. This included operators such as Union Oil Co. of California, Arthur McAdams, Amrich Energy, and Solimar Energy, among others.

Figure 5. Pie chart of well divestments. Well divestments were categorized by the economic status of the divesting operator. Nearly 80% of divestments were from companies that shut down their operations in California. An additional 0.14% shut down production but still own idle wells in California that require plugging and site remediation.

Acquisitions

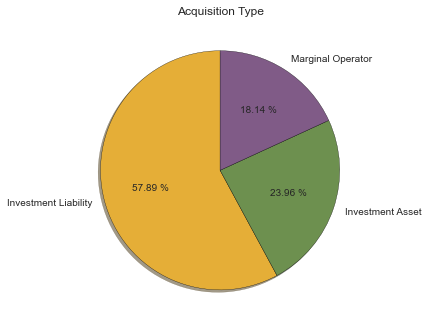

The acquisition of wells was also categorized, but by the economic status of the receiving operator. The pie chart below in Figure 6 shows the breakdown of acquisitions by categorized transfers. The majority, about 58%, of transfers were from larger operators to smaller operators, and are labeled as ‘investment liabilities’. They are liabilities because while wells may still be producing, they are typically near the end of their production decline curve; otherwise they would not have been divested. As such these wells may not produce enough oil or gas to cover their own plugging and remediation costs. An additional 18% of transfers were to a ‘marginal operator’ – that is, oil and gas companies that are created to absorb retirement obligations, such as the spin-off of California Resources Corporation and its subsidiaries that funded the expansion of Occidental Petroleum into new oil and gas basins in Texas, Colorado, and internationally. Only about 24% of the well transfers were acquisitions by larger or similarly sized operators.

Figure 6. Pie chart of well acquisitions. Well acquisitions were categorized by the economic status of the acquiring operator.

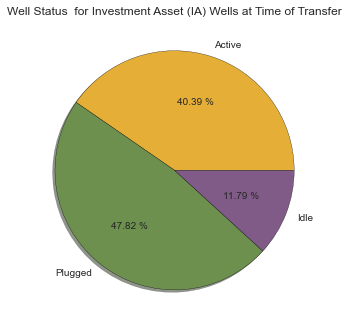

While ‘investment asset’ (IA) acquisitions constitute nearly a quarter of well transfers, the majority of wells acquired by larger companies were ‘idle’ or ‘plugged’ (about 60%). Figure 7 below shows the breakdown of the ‘investment asset’ category by well status at the time of ownership transfer. About 40% of the IA acquisitions by larger companies were active wells, but similar to the full population sample, the vast majority of the active wells were stripper wells (98.4%), and only 6.6% of the active IA wells produced more than 5 bbls/day.

Figure 7. Well statuses of ‘Investment Asset’ (IA) transfers. The dataset of transfers was limited to just the subset of transfers that went from a smaller operator to a larger or similar sized operator.

Discussion

The analyses in this report confirm observation of the trend of larger operators divesting wells at the end of their productive lifespan to smaller operators. This report established that ownership transfers in the oil and gas industry tend to occur near the end of the productive life of an oil or gas well, with the transfers occurring once the majority of profit is extracted from a well. Over 96% of the transfers were either to smaller holding companies/operators, the result of a bankruptcy, or executed to facilitate the exit of a company from the California exploration and production market. These scenarios increase the risk that these wells will become orphaned, putting the financial burden of plugging and remediation costs on the taxpayers of California. The analyses further confirm the trend is growing. A total 51% of the state’s oil and gas wells have been transferred from one operator to another, and the rate of transfers have grown dramatically since 2010.

The transfers of wells to California Resources Corporation (CRC) highlight the fiscal risk to the state from this trend. CRC and its subsidiaries, created to absorb bad assets and provide fresh sources of funding, make up the largest operator in the state of California. In the operator’s creation by Occidental Petroleum in 2014, CRC inherited $4.4B in debt. In 2020 CRC, California’s largest oil and gas operator, filed for Chapter 11 bankruptcy. While the operator was able to restructure and continue to operate, in the event of a future Chapter 7 bankruptcy the state would be left with little recourse. Bankruptcies of Venoco Inc., Greka Oil Co., Rincon Island Limited Partnership, and Linn Energy have already opened California up to major financial obligations as the State Lands Commission takes over plugging and remediation costs.

The data also shows that numerous operators are engaged in ‘insolvent divestment’ – that is, the practice of operators selling off their productive wells to temporarily stave off bankruptcy, but in the process stripping themselves of the earnings stream that would enable them to fund the plugging and abandonment of idle wells. As a result, the idle wells become orphaned when avoiding bankruptcy is no longer possible, with the operators having already taken the benefit from the sales of their remaining productive wells. These likely insolvent operators include Amrich Energy Inc., Arthur McAdams, Tetra Oil Company, and Innex California Inc. to name just a few. These operators have sold all of their producing oil wells to other companies, but still own numerous idle wells. Without the oil sale profits from producing wells, these companies may not be able to afford the maintenance costs for their remaining idle wells, much less afford to plug and reclaim the idle wellsites.

An issue that has not been discussed in the literature or the media is the issue of plugged well liabilities – i.e., the inevitable cost of monitoring and sometimes repairing wells that have been plugged. While the initial cost of plugging an operational well has been discussed, the fact that operators will be liable for replugging costs in perpetuity, has not been considered. While properly plugged wells are considered environmentally innocuous, the efficacy of a well plug is not permanent. Well plugs can and do fail, and there are many such events that have been covered by the media. While current plugging techniques are much better than the past, most of the wells plugged in California were completed decades ago and are questionable at best. The data shows that tens of thousands of potentially improperly plugged wells have transferred ownership, and California has issued at least 261 ‘re-abandonment’ permits just since the beginning of 2020 to deal with the issue of failed well pluggings.

In addition to divesting from low producing and idle wells to shed well plugging and remediation costs, divesting from the ownership of plugged wells also sheds future liabilities that would otherwise make operators responsible for the future costs of re-plugging. All well pluggings have a discrete lifespan, regardless of whether the plugging operation was completed properly, or using improper methods (such as shoving a telephone pole down the borehole – a method reportedly common in the Los Angeles Basin). In Aera’s exit divestment from California, Exxon-Mobil and Shell transferred the ownership and liabilities of over 35,700 plugged wells to the German energy investment firm IKAV.

Conclusions

Based on the results of this report that show that over half of the oil and gas wells in California have changed hands, and the vast majority at the end of their productive lifespan to smaller operators; FracTracker Alliance recommends the adoption of pre-emptive regulations to financially protect state taxpayers against the insolvency of marginal operators. Both the plugging and remediation of operational (active and idle) wellsites as well as the continued maintenance of plugged wells needs to be considered when wells are transferred from one operator to another. Existing bonding requirements for new wells need to be increased to cover the full lifespan of maintenance for wells, from plugging and remediation through lifetime maintenance of the plugged well. Additionally, existing wells need to be re-bonded at the time of transfer to address the deficits resulting from blanket bond policies and the increasing costs of well plugging and reclamation services.

References & Where to Learn More

Topics in This Article:

Join the Conversation

Stay Informed

Support Our Work

FracTracker Alliance helps communicate the risks of oil and gas and petrochemical development to advance just energy alternatives that protect public health, natural resources, and the climate.

By contributing to FracTracker, you are helping to make tangible changes, such as decreasing the number of oil and gas wells in the US, protecting the public from toxic and radioactive chemicals, and stopping petrochemical expansion into vulnerable communities.

Your donations help fund the sourcing and analysis of new data so that we can keep you informed and continually update our resources.

Please donate to FracTracker today as a way to advocate for clean water, clean air, and healthy communities.

What You Should Read Next

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/03/Web-Elements-Map-thumbnails-28.png

500

750

Shannon Smith

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Shannon Smith2026-06-12 15:27:012026-06-12 15:41:18PA DEP Approves Unusual “Mineral Brine” Well in Erie County, Raising Concerns About New Regulatory Loophole https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/05/Untitled-design.jpg

844

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2026-04-30 17:32:352026-05-28 13:40:18From Coal Plant to AI Campus: FracTracker Documents Construction at Homer City

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/05/Untitled-design.jpg

844

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2026-04-30 17:32:352026-05-28 13:40:18From Coal Plant to AI Campus: FracTracker Documents Construction at Homer City https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/05/3.jpg

628

1200

Gwen Klenke

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Gwen Klenke2026-04-29 16:16:562026-05-08 11:24:12An update on Southwest Detroit Industrial Impacts: The Zug Island Ruling

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/05/3.jpg

628

1200

Gwen Klenke

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Gwen Klenke2026-04-29 16:16:562026-05-08 11:24:12An update on Southwest Detroit Industrial Impacts: The Zug Island Ruling https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/03/Shell-Polymers-Data-Tool-Graphics.png

628

1200

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2026-03-26 15:42:172026-04-03 10:35:54FracTracker’s New Data Tool Visualizes Shell’s Pollution, Violations, and Malfunctions Ahead of Permit Public Hearing

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/03/Shell-Polymers-Data-Tool-Graphics.png

628

1200

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2026-03-26 15:42:172026-04-03 10:35:54FracTracker’s New Data Tool Visualizes Shell’s Pollution, Violations, and Malfunctions Ahead of Permit Public Hearing https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/01/Howell-Township-Win-Article-Graphics.jpg

628

1200

Gwen Klenke

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Gwen Klenke2026-01-14 18:33:052026-05-06 18:11:32Howell Township Data Center Win: $1B Project Withdrawn After Community Meeting on Energy and Infrastructure Impacts

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2026/01/Howell-Township-Win-Article-Graphics.jpg

628

1200

Gwen Klenke

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Gwen Klenke2026-01-14 18:33:052026-05-06 18:11:32Howell Township Data Center Win: $1B Project Withdrawn After Community Meeting on Energy and Infrastructure Impacts https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/06/SShamer_Infrastructure-pipeline-rightofway-ColumbiaLineMB-BaltimoreCounty-MD-May2016.jpg

266

400

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-09-03 16:14:462025-09-30 10:26:57Comment Opposing the Southeast Supply Enhancement Project (SSEP) – Clean Water Act Section 404 Permit Application (SAW-2024-01961)

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/06/SShamer_Infrastructure-pipeline-rightofway-ColumbiaLineMB-BaltimoreCounty-MD-May2016.jpg

266

400

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-09-03 16:14:462025-09-30 10:26:57Comment Opposing the Southeast Supply Enhancement Project (SSEP) – Clean Water Act Section 404 Permit Application (SAW-2024-01961) https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/07/California-oil-fields-feature.jpg

667

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2025-08-26 17:36:222025-08-27 21:56:28California’s New Oil Wells Average 13.5 Barrels/Day — Far Below State Projections

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/07/California-oil-fields-feature.jpg

667

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2025-08-26 17:36:222025-08-27 21:56:28California’s New Oil Wells Average 13.5 Barrels/Day — Far Below State Projections Photo by David Becker

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/08/david-becker-crs2vlkSe98-unsplash.jpg

996

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-08-22 11:22:272025-08-26 15:47:09FracTracker Launches Oil, Gas, and Petrochemical Data Portals

Photo by David Becker

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/08/david-becker-crs2vlkSe98-unsplash.jpg

996

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-08-22 11:22:272025-08-26 15:47:09FracTracker Launches Oil, Gas, and Petrochemical Data Portals https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2013/12/Colorado.jpg

642

1144

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-07-22 10:42:552025-07-23 11:06:23Colorado Operators Increase Chemical Disclosures After Public Pressure, but Major Gaps Remain

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2013/12/Colorado.jpg

642

1144

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-07-22 10:42:552025-07-23 11:06:23Colorado Operators Increase Chemical Disclosures After Public Pressure, but Major Gaps Remain https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/07/Missouri-Oil-and-Gas-Wells-2025.jpg

921

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2025-07-21 19:15:592025-07-22 10:08:23Evaluation of Federal Requirements for Plugging Orphaned Oil and Gas Wells: A Missouri Case Study

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/07/Missouri-Oil-and-Gas-Wells-2025.jpg

921

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2025-07-21 19:15:592025-07-22 10:08:23Evaluation of Federal Requirements for Plugging Orphaned Oil and Gas Wells: A Missouri Case Study https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2019/03/IdleWellsHathaway_resize.jpg

400

900

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-07-03 13:40:552025-07-03 15:42:15Methane Matters, but Make Polluters Pay: FracTracker’s Response to Carl Pope

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2019/03/IdleWellsHathaway_resize.jpg

400

900

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-07-03 13:40:552025-07-03 15:42:15Methane Matters, but Make Polluters Pay: FracTracker’s Response to Carl Pope https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/11/Fhn3YgeXkAI0QiX.jpg

675

1200

Katie Jones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Katie Jones2025-07-03 13:22:502026-01-14 17:55:32Shell Polymers Monaca: 17.9 Billion Pounds of Emissions and Repeated Violations in Pennsylvania

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/11/Fhn3YgeXkAI0QiX.jpg

675

1200

Katie Jones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Katie Jones2025-07-03 13:22:502026-01-14 17:55:32Shell Polymers Monaca: 17.9 Billion Pounds of Emissions and Repeated Violations in Pennsylvania https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2016/07/DSC_0266_LowRes.jpg

3000

4496

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-06-30 14:48:532025-07-03 13:47:59Plum Borough Rejects Fracking Waste Injection Well After Public Pushback

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2016/07/DSC_0266_LowRes.jpg

3000

4496

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-06-30 14:48:532025-07-03 13:47:59Plum Borough Rejects Fracking Waste Injection Well After Public Pushback https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/05/51382261216_f8af819a45_o.jpg

1125

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2025-05-31 12:00:592026-03-13 12:05:07Power Plant Locations and Unemployment Rates

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/05/51382261216_f8af819a45_o.jpg

1125

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2025-05-31 12:00:592026-03-13 12:05:07Power Plant Locations and Unemployment Rates https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/04/49770601811_6cc7e18996_k.jpg

716

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2025-04-07 15:42:272025-04-07 15:42:27Pipeline Incidents Are a Daily Occurrence

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/04/49770601811_6cc7e18996_k.jpg

716

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2025-04-07 15:42:272025-04-07 15:42:27Pipeline Incidents Are a Daily Occurrence https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/02/Los-Angeles-skyline-feature-scaled.jpg

667

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2025-03-27 15:37:102025-04-01 12:55:42Environmental Justice Analysis of Oil Extraction in Los Angeles Communities

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/02/Los-Angeles-skyline-feature-scaled.jpg

667

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2025-03-27 15:37:102025-04-01 12:55:42Environmental Justice Analysis of Oil Extraction in Los Angeles Communities https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/03/3_TAuch_Infrastructure-FrackPad-SouthwestPA_April2019.jpg

830

1500

Katie Jones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Katie Jones2025-03-26 14:05:222025-04-01 12:29:01How Increased Protective Buffer Zones Could Help Protect 3.6 million Pennsylvanians

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/03/3_TAuch_Infrastructure-FrackPad-SouthwestPA_April2019.jpg

830

1500

Katie Jones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Katie Jones2025-03-26 14:05:222025-04-01 12:29:01How Increased Protective Buffer Zones Could Help Protect 3.6 million Pennsylvanians https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/02/49727923413_5d7b7335a0_k.jpg

621

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2025-01-31 14:52:292025-02-03 15:59:13Regulatory Gaps and Resistance: The Battle Over Fracking in Southern Illinois

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/02/49727923413_5d7b7335a0_k.jpg

621

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2025-01-31 14:52:292025-02-03 15:59:13Regulatory Gaps and Resistance: The Battle Over Fracking in Southern Illinois https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/02/1400669_062416-kabc-cuffe-erskine1-imgcrtr.jpg

720

1280

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-01-31 12:07:132025-02-06 14:11:38Can California Energy Policy Move Past its Contradictions?

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/02/1400669_062416-kabc-cuffe-erskine1-imgcrtr.jpg

720

1280

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2025-01-31 12:07:132025-02-06 14:11:38Can California Energy Policy Move Past its Contradictions? FracTracker Alliance, 2024

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/03/ODNR-Oil-and-Gas-Incidents-2018-2023.jpg

844

1500

Gwen Klenke

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Gwen Klenke2025-01-06 11:47:452025-01-06 14:49:36Data Gaps: A Critical Examination of Oil and Gas Well Incidents in Ohio

FracTracker Alliance, 2024

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/03/ODNR-Oil-and-Gas-Incidents-2018-2023.jpg

844

1500

Gwen Klenke

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Gwen Klenke2025-01-06 11:47:452025-01-06 14:49:36Data Gaps: A Critical Examination of Oil and Gas Well Incidents in Ohio Great Plains Action Society

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/10/No-CO2-Ppelines-Sioux-City.jpg

672

1012

Gwen Klenke

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Gwen Klenke2024-10-22 11:55:082024-10-25 12:10:00Indigenous Communities’ Fight Against CO2 Pipelines in the Great Plains

Great Plains Action Society

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/10/No-CO2-Ppelines-Sioux-City.jpg

672

1012

Gwen Klenke

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Gwen Klenke2024-10-22 11:55:082024-10-25 12:10:00Indigenous Communities’ Fight Against CO2 Pipelines in the Great Plains https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/08/Midas6M_RecvFacil_042024_Header.jpg

891

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2024-08-01 20:41:312024-08-02 17:55:17Pennsylvania Oil and Gas Industry Trends: Drilled Wells, Violations, Production, and Waste

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/08/Midas6M_RecvFacil_042024_Header.jpg

891

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2024-08-01 20:41:312024-08-02 17:55:17Pennsylvania Oil and Gas Industry Trends: Drilled Wells, Violations, Production, and Waste https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/06/Hydrogen-molecule-feature.jpg

844

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2024-06-05 17:41:582024-06-06 09:18:40A Closer Look at Risks of the Appalachian Hydrogen Hub

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/06/Hydrogen-molecule-feature.jpg

844

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2024-06-05 17:41:582024-06-06 09:18:40A Closer Look at Risks of the Appalachian Hydrogen Hub FracTracker Alliance, 2024

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/06/Falcon-Pipeline-Violations-2024.jpg

844

1500

Katie Jones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Katie Jones2024-06-05 10:35:022024-06-05 11:36:30Falcon Pipeline Criminal Charges Explained

FracTracker Alliance, 2024

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/06/Falcon-Pipeline-Violations-2024.jpg

844

1500

Katie Jones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Katie Jones2024-06-05 10:35:022024-06-05 11:36:30Falcon Pipeline Criminal Charges Explained https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2016/10/Nix-Pix-050.jpg

3088

4629

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2024-06-04 16:34:592025-05-02 14:53:36The Importance of Surveying Rural Landowners in North Dakota on Fracking

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2016/10/Nix-Pix-050.jpg

3088

4629

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2024-06-04 16:34:592025-05-02 14:53:36The Importance of Surveying Rural Landowners in North Dakota on Fracking https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2016/04/Mount-Carbon-WV-Large.jpg

1429

1888

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2024-06-04 14:18:082024-06-04 16:39:12Exploring the Fallout of Precision Scheduled Rail: A Rail Worker’s Perspective on Precision Scheduled Rail

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2016/04/Mount-Carbon-WV-Large.jpg

1429

1888

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2024-06-04 14:18:082024-06-04 16:39:12Exploring the Fallout of Precision Scheduled Rail: A Rail Worker’s Perspective on Precision Scheduled Rail https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2019/12/Drilling-rig-in-Washington-County-Pennsylvania.jpg

573

2000

Katie Jones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Katie Jones2024-05-02 15:54:282025-05-21 12:33:41Not-So-Radical Transparency: An Ineffective and Unnecessary Partnership Between Pennsylvania Governor Shapiro and the Gas Company CNX

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2019/03/IdleWellsHathaway_resize.jpg

400

900

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2024-05-02 10:32:552024-05-02 12:43:28California Must Improve Management of Idle Wells

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2019/12/Drilling-rig-in-Washington-County-Pennsylvania.jpg

573

2000

Katie Jones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Katie Jones2024-05-02 15:54:282025-05-21 12:33:41Not-So-Radical Transparency: An Ineffective and Unnecessary Partnership Between Pennsylvania Governor Shapiro and the Gas Company CNX

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2019/03/IdleWellsHathaway_resize.jpg

400

900

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2024-05-02 10:32:552024-05-02 12:43:28California Must Improve Management of Idle Wells https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/10/gilooly-farmer-pa-2013.jpg

823

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2024-04-26 11:34:082024-04-29 09:39:15Holes in FracFocus

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/10/gilooly-farmer-pa-2013.jpg

823

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2024-04-26 11:34:082024-04-29 09:39:15Holes in FracFocus FracTracker Alliance, 2024

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/03/WV-PFAS-Map.jpeg

763

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2024-03-29 15:06:512024-03-29 15:42:29Mapping PFAS Chemicals Used in Fracking Operations in West Virginia

FracTracker Alliance, 2024

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/03/WV-PFAS-Map.jpeg

763

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2024-03-29 15:06:512024-03-29 15:42:29Mapping PFAS Chemicals Used in Fracking Operations in West Virginia https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2020/04/California-well-pad.jpg

666

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2024-03-07 17:01:582024-03-12 09:55:39Chevron’s $2.3 Billion Asset Adjustment Raises Questions Amidst Regulatory Changes in California

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2020/04/California-well-pad.jpg

666

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2024-03-07 17:01:582024-03-12 09:55:39Chevron’s $2.3 Billion Asset Adjustment Raises Questions Amidst Regulatory Changes in California Ross incinerator in Eaton Township. Photo by Ted Auch, FracTracker Alliance, 2023

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/02/52748252528_19364d2943_k.jpg

918

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2024-02-07 21:56:582024-02-09 13:47:09Stop Toxic Threat: A Heavy Industrial Zoning Battle

Ross incinerator in Eaton Township. Photo by Ted Auch, FracTracker Alliance, 2023

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/02/52748252528_19364d2943_k.jpg

918

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2024-02-07 21:56:582024-02-09 13:47:09Stop Toxic Threat: A Heavy Industrial Zoning Battle Ross Environmental Hazardous Waste Incinerator in Eaton Township, Ohio. Ted Auch, FracTracker Alliance, 2023

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/02/52747231757_2834f8bd30_k.jpg

1124

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2024-02-01 22:00:352024-02-09 13:45:10East Palestine Warning: The Growing Threat From Hazardous Waste Storage

Ross Environmental Hazardous Waste Incinerator in Eaton Township, Ohio. Ted Auch, FracTracker Alliance, 2023

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/02/52747231757_2834f8bd30_k.jpg

1124

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2024-02-01 22:00:352024-02-09 13:45:10East Palestine Warning: The Growing Threat From Hazardous Waste Storage FracTracker Alliance, 2024

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/01/California-Daily-Oil-Production-2024.jpg

844

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2024-01-30 05:00:012024-02-05 13:46:42Index of Oil and Gas Operator Health in California Shows Risks to State Economy and Taxpayers

FracTracker Alliance, 2024

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/01/California-Daily-Oil-Production-2024.jpg

844

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2024-01-30 05:00:012024-02-05 13:46:42Index of Oil and Gas Operator Health in California Shows Risks to State Economy and Taxpayers The cottage along Slope Creek, months after being vacated due to health concerns caused by nearby oil and gas operations. Photo courtesy of Chloe Mankin

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/01/slopecreek2018.jpg

845

1500

Chloe Mankin

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Chloe Mankin2024-01-12 12:51:302024-01-12 16:32:21Calling for Change: Life on the Fracking Frontlines

The cottage along Slope Creek, months after being vacated due to health concerns caused by nearby oil and gas operations. Photo courtesy of Chloe Mankin

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2024/01/slopecreek2018.jpg

845

1500

Chloe Mankin

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Chloe Mankin2024-01-12 12:51:302024-01-12 16:32:21Calling for Change: Life on the Fracking Frontlines https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/12/Figure-6-Rail-Population.jpg

801

1498

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2023-12-14 16:26:372023-12-15 11:47:53On the Wrong Track: Risks to Residents of the Upper Ohio River Valley From Railroad Incidents

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/12/Figure-6-Rail-Population.jpg

801

1498

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2023-12-14 16:26:372023-12-15 11:47:53On the Wrong Track: Risks to Residents of the Upper Ohio River Valley From Railroad Incidents Matt Kelso, FracTracker Alliance, 2023

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/11/DSCN1328.jpg

1125

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2023-11-16 13:25:082025-03-06 15:39:23Digital Atlas: Exploring Nature and Industry in the Raccoon Creek Watershed

Matt Kelso, FracTracker Alliance, 2023

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/11/DSCN1328.jpg

1125

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2023-11-16 13:25:082025-03-06 15:39:23Digital Atlas: Exploring Nature and Industry in the Raccoon Creek Watershed https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/10/RusticRidge_102023.jpg

1119

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2023-11-09 19:01:252025-08-12 13:45:14Why Do Houses Keep Exploding in One Pennsylvania Suburb?

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/10/RusticRidge_102023.jpg

1119

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2023-11-09 19:01:252025-08-12 13:45:14Why Do Houses Keep Exploding in One Pennsylvania Suburb? https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/10/Wells-Within-3200-Feet-of-Schools-Childcare-CA.jpg

595

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-10-04 16:38:472023-10-04 21:19:54Oil and Gas Activity Within California Public Health Protection Zones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/10/Wells-Within-3200-Feet-of-Schools-Childcare-CA.jpg

595

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-10-04 16:38:472023-10-04 21:19:54Oil and Gas Activity Within California Public Health Protection Zones https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/05/Colorado-Water-Use-5.2.23.jpg

589

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-05-02 12:33:532026-04-23 15:43:28Evaluation of the Capacity for Water Recycling for Colorado Oil and Gas Extraction Operations

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/05/Colorado-Water-Use-5.2.23.jpg

589

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-05-02 12:33:532026-04-23 15:43:28Evaluation of the Capacity for Water Recycling for Colorado Oil and Gas Extraction Operations Sarah Carballo, FracTracker Alliance, 2022

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/04/DSC_0855.jpg

1001

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2023-04-27 13:46:002023-04-27 14:18:17Evidence Shows Oil and Gas Companies Use PFAS in New Mexico Wells

Sarah Carballo, FracTracker Alliance, 2022

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/04/DSC_0855.jpg

1001

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2023-04-27 13:46:002023-04-27 14:18:17Evidence Shows Oil and Gas Companies Use PFAS in New Mexico Wells https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/04/Rework-Permits-Feature-Image.png

506

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-04-14 11:36:392023-04-28 16:05:23CalGEM Permit Review Q1 2023: Well Rework Permits Increase by 76% in California

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/04/Rework-Permits-Feature-Image.png

506

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-04-14 11:36:392023-04-28 16:05:23CalGEM Permit Review Q1 2023: Well Rework Permits Increase by 76% in California Ted Auch, FracTracker Alliance, 2022

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/02/DSC_1026_LowRes.jpg

1000

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2023-02-01 15:36:182023-02-01 17:01:372022 Pipeline Incidents Update: Is Pipeline Safety Achievable?

Ted Auch, FracTracker Alliance, 2022

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/02/DSC_1026_LowRes.jpg

1000

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2023-02-01 15:36:182023-02-01 17:01:372022 Pipeline Incidents Update: Is Pipeline Safety Achievable? https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2020/09/Methane_Air_WaterQualityConcerns-1.jpg

534

800

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2023-01-31 15:01:342023-02-27 16:43:15Testimony On EPA’s Proposed Methane Pollution Standards for the Oil and Gas Industry

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2020/09/Methane_Air_WaterQualityConcerns-1.jpg

534

800

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2023-01-31 15:01:342023-02-27 16:43:15Testimony On EPA’s Proposed Methane Pollution Standards for the Oil and Gas Industry https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/01/California-Rework-Permits-2023.jpg

541

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-01-24 09:01:352023-01-24 13:21:55Assessment of Rework Permits on Oil Production from Operational Wells Within the 3,200-Foot Public Health Protection Zone

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/01/California-Rework-Permits-2023.jpg

541

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-01-24 09:01:352023-01-24 13:21:55Assessment of Rework Permits on Oil Production from Operational Wells Within the 3,200-Foot Public Health Protection Zone https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/01/CalGEM-Q4-2022-Permit-Review.jpg

570

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-01-18 18:01:532023-01-18 18:03:23CalGEM Permit Review Q4 2022: Oil Permit Approvals Show Steep Rise Within Protective Buffer Zones

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2023/01/CalGEM-Q4-2022-Permit-Review.jpg

570

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2023-01-18 18:01:532023-01-18 18:03:23CalGEM Permit Review Q4 2022: Oil Permit Approvals Show Steep Rise Within Protective Buffer Zones https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/03/TAuch_Transportation-RoverPipeline_Construction-EnergyTransferPartners-Woodsfield_OH_May2017.jpg

576

1500

Karen Edelstein

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Karen Edelstein2022-11-30 17:50:122024-01-22 16:03:23A Contentious Landscape of Pipeline Build-outs in the Eastern US

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/03/TAuch_Transportation-RoverPipeline_Construction-EnergyTransferPartners-Woodsfield_OH_May2017.jpg

576

1500

Karen Edelstein

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Karen Edelstein2022-11-30 17:50:122024-01-22 16:03:23A Contentious Landscape of Pipeline Build-outs in the Eastern US https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/11/Rager-Mountain-Feature.jpg

636

1500

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2022-11-30 14:12:222023-02-03 13:50:48Major Gas Leak Reveals Risks of Aging Gas Storage Wells in Pennsylvania

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/11/Rager-Mountain-Feature.jpg

636

1500

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2022-11-30 14:12:222023-02-03 13:50:48Major Gas Leak Reveals Risks of Aging Gas Storage Wells in Pennsylvania https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/11/DSC_1359_HighRes.jpg

1000

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2022-11-23 15:15:112025-03-06 15:40:10Coursing Through Gasland: A Digital Atlas Exploring Natural Gas Development in the Towanda Creek Watershed

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/11/Fhn3YgeXkAI0QiX.jpg

675

1200

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2022-11-17 16:43:392022-11-18 13:41:39Falcon Pipeline Online, Begins Operations Following Violations of Clean Streams Law

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/11/DSC_1359_HighRes.jpg

1000

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2022-11-23 15:15:112025-03-06 15:40:10Coursing Through Gasland: A Digital Atlas Exploring Natural Gas Development in the Towanda Creek Watershed

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/11/Fhn3YgeXkAI0QiX.jpg

675

1200

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2022-11-17 16:43:392022-11-18 13:41:39Falcon Pipeline Online, Begins Operations Following Violations of Clean Streams Law https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/10/Columbus-Source-Water.jpg

605

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-10-31 21:39:022022-11-29 14:24:38Synopsis: Risks to the Greater Columbus Water Supply from Oil and Gas Production

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/10/Columbus-Source-Water.jpg

605

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-10-31 21:39:022022-11-29 14:24:38Synopsis: Risks to the Greater Columbus Water Supply from Oil and Gas Production https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/09/DSC_1021_LowRes__1607617394306__w1920-e1663613850641.jpg

667

1500

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2022-09-19 15:08:172022-11-03 11:56:26Desalination: The Chemical Industry’s Demand for Water in Texas

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/09/DSC_1021_LowRes__1607617394306__w1920-e1663613850641.jpg

667

1500

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2022-09-19 15:08:172022-11-03 11:56:26Desalination: The Chemical Industry’s Demand for Water in Texas https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/06/LKrop_infrastructure-offshoredrilling-drillrigs-SantaBarbara-CA_EnvrDefenseCtr_Aug20131-e1663254826557.jpg

178

400

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2022-09-06 13:32:202022-09-15 11:14:03Take Action in Support of No New Leases

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/06/LKrop_infrastructure-offshoredrilling-drillrigs-SantaBarbara-CA_EnvrDefenseCtr_Aug20131-e1663254826557.jpg

178

400

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2022-09-06 13:32:202022-09-15 11:14:03Take Action in Support of No New Leases https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/08/51119572588_132e0366c1_k_1-e1663254774314.jpg

607

1364

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-08-31 14:33:482022-09-15 16:29:45Carbon Capture and Storage: Developments in the Law of Pore Space in North Dakota

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/08/51119572588_132e0366c1_k_1-e1663254774314.jpg

607

1364

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-08-31 14:33:482022-09-15 16:29:45Carbon Capture and Storage: Developments in the Law of Pore Space in North Dakota https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2017/03/DSC_0341_to_0345_LowRes2-e1663254589691.jpg

667

1500

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2022-08-31 12:54:012023-12-07 14:33:18Carbon Capture and Storage: Industry Connections and Community Impacts

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2017/03/DSC_0341_to_0345_LowRes2-e1663254589691.jpg

667

1500

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2022-08-31 12:54:012023-12-07 14:33:18Carbon Capture and Storage: Industry Connections and Community Impacts https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/08/ExxonMobil-LaBarge-CCUS-e1663254477876.jpg

465

1047

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2022-08-31 11:19:122022-09-15 11:08:15Carbon Capture and Storage: Fact or Fiction?

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/08/ExxonMobil-LaBarge-CCUS-e1663254477876.jpg

465

1047

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2022-08-31 11:19:122022-09-15 11:08:15Carbon Capture and Storage: Fact or Fiction? https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/08/MOV_8837_Moment-e1663254387862.jpg

284

640

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-08-22 09:52:582026-04-28 14:45:28FracTracker Finds Widespread Hydrocarbon Emissions from Active & Idle Oil and Gas Wells and Infrastructure in California

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/08/MOV_8837_Moment-e1663254387862.jpg

284

640

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-08-22 09:52:582026-04-28 14:45:28FracTracker Finds Widespread Hydrocarbon Emissions from Active & Idle Oil and Gas Wells and Infrastructure in California https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/07/kyle-ferrar-e1663254307641.jpg

636

1430

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-07-29 19:04:322022-09-15 11:05:17California Regulators Approve More Oil Well Permits Amid a Crisis of Leaking Oil Wells that Should be Plugged

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/07/kyle-ferrar-e1663254307641.jpg

636

1430

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-07-29 19:04:322022-09-15 11:05:17California Regulators Approve More Oil Well Permits Amid a Crisis of Leaking Oil Wells that Should be Plugged https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/06/CCSHFeatureImage.jpg

667

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-06-23 15:29:312022-06-30 12:30:43An Insider Take on the Appalachian Hydrogen & CCUS Conference

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/06/CCSHFeatureImage.jpg

667

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-06-23 15:29:312022-06-30 12:30:43An Insider Take on the Appalachian Hydrogen & CCUS Conference https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/06/TAuch_Infrastructure-OilRefinery_DowntownToledo-ToledoOil-LucasCounty-OH_Lighthawk_Sept2021.jpg

667

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2022-06-21 15:46:522024-06-18 10:53:27Does Hydrogen Have a Role in our Energy Future?

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/06/TAuch_Infrastructure-OilRefinery_DowntownToledo-ToledoOil-LucasCounty-OH_Lighthawk_Sept2021.jpg

667

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2022-06-21 15:46:522024-06-18 10:53:27Does Hydrogen Have a Role in our Energy Future? https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/05/Brine-spreading-map-feature-1.jpg

667

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-05-13 16:19:112022-08-10 15:43:05Oil and Gas Brine in Ohio

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/05/Brine-spreading-map-feature-1.jpg

667

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-05-13 16:19:112022-08-10 15:43:05Oil and Gas Brine in Ohio https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/05/DustingHighVolDirtyFilter-feature.jpg

667

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-05-03 09:37:492022-05-03 09:37:49PA Environment Digest Blog: Conventional Oil & Gas Drillers Dispose Of Drill Cuttings By ‘Dusting’

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/05/DustingHighVolDirtyFilter-feature.jpg

667

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Guest Author2022-05-03 09:37:492022-05-03 09:37:49PA Environment Digest Blog: Conventional Oil & Gas Drillers Dispose Of Drill Cuttings By ‘Dusting’ https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/04/TAuch_Cultural-Harvey_FamilyFarm_NEXUS_Pipeline-DTEEnergy_Enbridge-ChippewaLake_MedinaCounty_OH_May20183-feature.jpg

667

1500

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2022-04-28 14:12:552022-04-28 14:12:55Real Talk on Pipelines

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/04/TAuch_Cultural-Harvey_FamilyFarm_NEXUS_Pipeline-DTEEnergy_Enbridge-ChippewaLake_MedinaCounty_OH_May20183-feature.jpg

667

1500

Ted Auch, PhD

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Ted Auch, PhD2022-04-28 14:12:552022-04-28 14:12:55Real Talk on Pipelines https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/04/TAuch_Infrastructure-Compressor_Cryogenic_Complex-MarkWest_EnergyTransfer-WashingtonCounty-PA_Sept2021-feature.jpg

667

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2022-04-28 13:37:312023-03-09 14:03:402021 Production from Pennsylvania’s Oil and Gas Wells

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/04/TAuch_Infrastructure-Compressor_Cryogenic_Complex-MarkWest_EnergyTransfer-WashingtonCounty-PA_Sept2021-feature.jpg

667

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2022-04-28 13:37:312023-03-09 14:03:402021 Production from Pennsylvania’s Oil and Gas Wells https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/04/Russia-Ukraine-Energy-feature.jpg

667

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2022-04-20 13:25:452022-04-20 17:23:17Mapping Energy Systems Impacted by the Russia-Ukraine War

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/04/Russia-Ukraine-Energy-feature.jpg

667

1500

FracTracker Alliance

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

FracTracker Alliance2022-04-20 13:25:452022-04-20 17:23:17Mapping Energy Systems Impacted by the Russia-Ukraine War https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/04/IMG_5940-1.jpg

1125

1500

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2022-04-11 16:48:092022-04-20 13:23:14Dimock residents working to protect water from a new threat: fracking waste

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/04/IMG_5940-1.jpg

1125

1500

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2022-04-11 16:48:092022-04-20 13:23:14Dimock residents working to protect water from a new threat: fracking waste https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/03/KFerrar-feature-CAsetbacks2022.jpg

878

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-04-06 12:01:332023-08-24 19:08:53Implications of a 3,200-foot Setback in California

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/03/KFerrar-feature-CAsetbacks2022.jpg

878

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-04-06 12:01:332023-08-24 19:08:53Implications of a 3,200-foot Setback in California https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/03/BLenker_infrastructure-oilrig-southLA-CA_Oct20173.jpg

795

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-03-15 16:32:032022-03-15 18:00:00New Trends in Drilling Permit Approvals Take Shape in CA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/03/BLenker_infrastructure-oilrig-southLA-CA_Oct20173.jpg

795

1500

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-03-15 16:32:032022-03-15 18:00:00New Trends in Drilling Permit Approvals Take Shape in CA https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/03/KFerrar-CAlegislative-analysis_March2022.jpg

720

1280

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-03-14 15:18:402022-03-14 15:18:40Oil and Gas Drilling in California Legislative Districts

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/03/KFerrar-CAlegislative-analysis_March2022.jpg

720

1280

Kyle Ferrar, MPH

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Kyle Ferrar, MPH2022-03-14 15:18:402022-03-14 15:18:40Oil and Gas Drilling in California Legislative Districts https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/01/PFAS-wells-in-Colorado-Feature.jpg

667

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2022-01-31 16:36:332022-01-31 16:36:33New Report: Fracking with “Forever Chemicals” in Colorado

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/01/PFAS-wells-in-Colorado-Feature.jpg

667

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2022-01-31 16:36:332022-01-31 16:36:33New Report: Fracking with “Forever Chemicals” in Colorado https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/01/FeatImage_MK.jpg

935

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2022-01-20 15:32:142022-01-20 15:32:14Introducing: FracTracker’s comprehensive new Pennsylvania map!

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2022/01/FeatImage_MK.jpg

935

1500

Matt Kelso, BA

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Matt Kelso, BA2022-01-20 15:32:142022-01-20 15:32:14Introducing: FracTracker’s comprehensive new Pennsylvania map! https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/12/173695136_1422048161521006_7197500259062906334_n.jpg

667

1500

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2021-12-01 15:27:402021-12-01 15:27:40New Letter from Federal Regulators Regarding how the Falcon has Been Investigated

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/12/173695136_1422048161521006_7197500259062906334_n.jpg

667

1500

Erica Jackson

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png

Erica Jackson2021-12-01 15:27:402021-12-01 15:27:40New Letter from Federal Regulators Regarding how the Falcon has Been Investigated https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2021/11/TAuch_Infrastructure-naturalgas-powerplant-construction-Caithness-GuernseyCounty-OH_April2021.jpg

667

1500

Guest Author

https://www.fractracker.org/a5ej20sjfwe/wp-content/uploads/2025/09/2025-Wordmark-Logo.png